5 Things to Know About Sustainable Funds

More funds, greater flows, and strong relative performance in 2018.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Stock and bond markets may have struggled in 2018, but sustainable funds in the United States had a good year. They grew in number and size. They attracted record net flows. They turned in strong relative performance. Sustainable exchange-traded funds, in particular, experienced significant growth. But investors shouldn't be too quick to paint them all with the same brush because, as the group has expanded, some clear distinctions can be made between several types of sustainable funds. Those are among my conclusions in this year's report on sustainable funds in the U.S.

Here are five takeaways from the report:

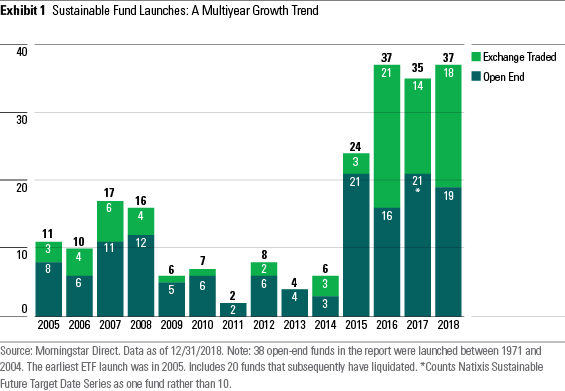

1) The universe of sustainable funds in the U.S. continues to grow. The number of sustainable funds offered to U.S. investors at the end of 2018 and included in this year's report was 351, up from 235 in last year's report. The number of new funds launched tied with 2016 as the most ever, and 62 existing funds added sustainability/environmental, social, and governance criteria to their prospectuses.

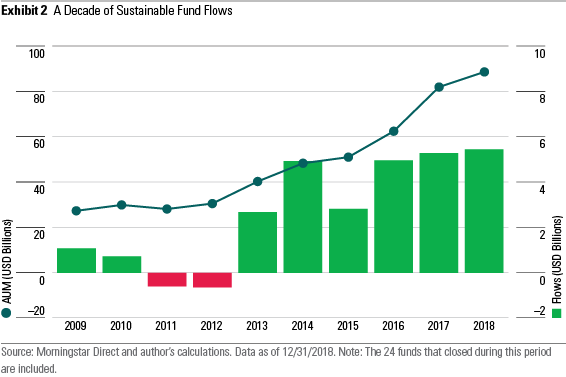

2) Sustainable funds in the U.S. attracted record net flows in 2018. U.S.-domiciled sustainable funds attracted nearly $5.5 billion in net flows last year. That marks the third-straight year of record annual net flows to sustainable funds and stands in stark contrast with the overall U.S. fund universe, which netted its lowest calendar-year flows since 2008. Speaking of the past decade, in the four years following the financial crisis, 2009-12, annual net flows averaged only $136 million. In the six years since, 2013-18, annual net flows averaged $4.4 billion.

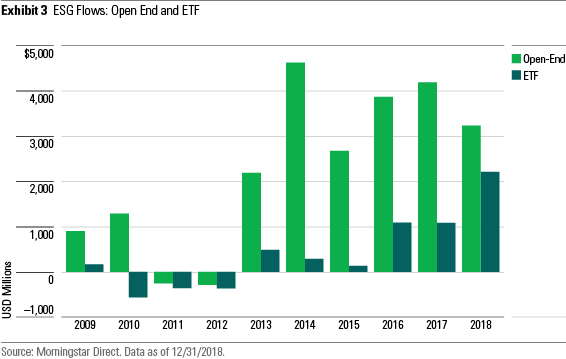

3) Sustainable ETFs are gaining ground. Over the past three years, the number of sustainable ETF launches nearly matched those of open-end funds. It is now possible to find sustainable ETFs that investors can substitute for market-cap-weighted indexes in the U.S. large-cap, small/mid-cap, growth and value, global-equity, non-U.S. developed equity, emerging-markets, and intermediate-bond segments. Sustainable ETF net flows grew to 40% of overall sustainable-fund flows in 2018 from 20% in each of the two previous years.

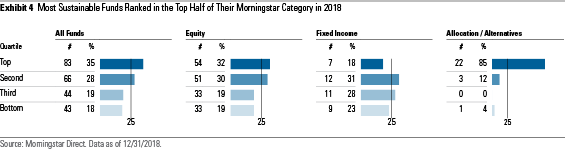

4) Sustainable funds outperformed in 2018. The returns of 35% of sustainable funds placed in the top quartile of their respective Morningstar Categories, and 63% placed in the top half. By contrast, only 18% finished in the bottom quartile. Strong relative performance by equity funds fueled those overall numbers. My colleague Hortense Bioy reported virtually identical results for European-domiciled sustainable funds in 2018.

Relative to their conventional peers, sustainable funds have held their own in up markets and outperformed in down markets over the past four years. During that period, the group's best relative performance was in 2015, when equity markets finished just above water. In the intervening two years when markets were more strongly positive, sustainable funds turned in average overall relative performance. It all adds up to impressive three- and five-year annualized returns relative to peers. For the trailing three years through the end of 2018, 57% of sustainable funds had annualized returns that ranked in the top half of their categories. For the trailing five years, 58% ranked in the top half.

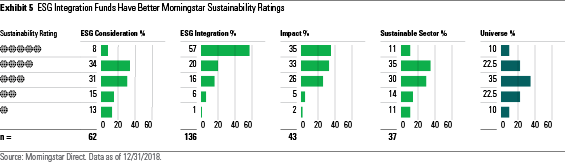

5) Four types of sustainable funds. The sustainable funds group breaks down into four types: ESG consideration funds are those that refer to ESG criteria in their prospectuses as one set of factors that are considered in their investment process. Most of the existing funds that have recently added ESG to their prospectuses fall into this subgroup. ESG integration funds, by contrast, are those that make sustainability factors a major component of their processes for both security selection and portfolio construction. These funds also tend to be active owners, engaging with companies and supporting (and sometimes sponsoring) ESG-related shareholder resolutions. A third group, impact funds, focuses on broad sustainability themes and on delivering social or environmental impact alongside financial returns. The fourth group consists of sustainable sector funds focusing on investment opportunities that contribute to, and aim to benefit from, the transition to a green economy.

Sustainable funds of all types have plenty of room to grow. Their assets under management and flows, though both higher than ever before, remain tiny compared with the overall U.S. fund universe. While many financial intermediaries have yet to fully embrace sustainable investing, more asset managers are realizing the need to take account of sustainability factors in their investment processes, both for fiduciary reasons and in response to growing investor demand. Much of the new demand is coming from younger investors and women. They form an increasingly powerful investor segment with a higher level of confidence in the long-term investment value of strong ESG practices and want their investments to have a positive impact on the world. As their investable assets grow, more assets are likely to move into sustainable funds.

Interested in ESG? Check out a curated collection of our latest content on ESG investing.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)