The 30-Year Outlook for U.S. Stocks

How much of the past will repeat?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Looking Ahead Tuesday’s column discussed the primary investment lesson over the past 30 years: Own equities. Own as much as possible for as long as possible. To a first approximation, it was never wrong to buy stocks, and never right to sell them.

Today's installment addresses the more difficult task of looking forward. It's one thing to appreciate how successful equities have been. It's quite another to determine whether their marvelous results will continue.

We have been here before. In 1989, as I can personally attest, the prevailing message to stock-market debutantes was that past performance had been terrific, but it was unsustainable. Over the previous three decades, the S&P 500 had gained an annualized average of 5.5%, after inflation. (All total returns in this column are expressed in real terms.) Naturally, that figure would shrink going forward. The secret about equities was out: They had become too dear.

It was not so. Indeed, whereas U.S. stocks did post marginally lower nominal returns during the next 30 years, their real gains were higher. As inflation during the second period was only half the first period's, their annualized real returns improved to 6.5%. The correct counsel to 1989's equity novices was not to beware. Instead, it would have been, "The good news will only get better."

My point being that rapid judgments are unhelpful. Neither assuming that history will repeat nor instinctive contrarianism are the correct approaches.

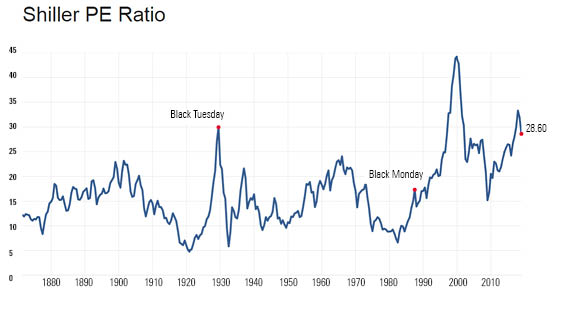

High CAPE Ratio The best starting point is price. How much do stocks cost? And the best measure of price, by my judgment, is the Shiller CAPE Ratio, developed by Nobel laureate Robert Shiller. The CAPE Ratio evaluates the average cost that equity investors pay to hold corporate earnings (as averaged over a company's previous 10 years). A ratio of 20 means that placing $10,000 in a stock-market index will, in effect, purchase $500 worth of earnings.

Kind-hearted people have calculated and published the S&P 500's CAPE Ratio over time. This permits us to place current stock quotes into some perspective. When compared with the two earlier starting points, 1959 and 1989, are today's stock valuations high, medium, or low?

- Source: mltpl.com

Without question, they are high. In 1959, the CAPE Ratio was about 20, in 1989 it was 16, and now it exceeds 28. By perhaps the broadest, most-comprehensive stock-price scoreboard that has been devised, the S&P 500 is pricey. This can partially be explained away by changes in accounting standards that have improved companies' earnings quality, and partially by greater overall financial stability. Modern economic cycles are longer than in the past. Along with quiescent inflation, that justifies a steeper stock-market valuation.

But the current appraisal would seem to overshoot the mark. A CAPE Ratio of 28 implies an "earnings yield" on the S&P 500 of 3.5%. While above that of a 10-year Treasury yield, which rests at 2.7%, that amount is not comforting. Not only are stocks riskier than government bonds, and their payouts mostly theoretical rather than actual (aside from dividend payments), but the earnings used to calculate today's CAPE Ratio occurred almost entirely during an economic expansion. They are likely to decline in the near term.

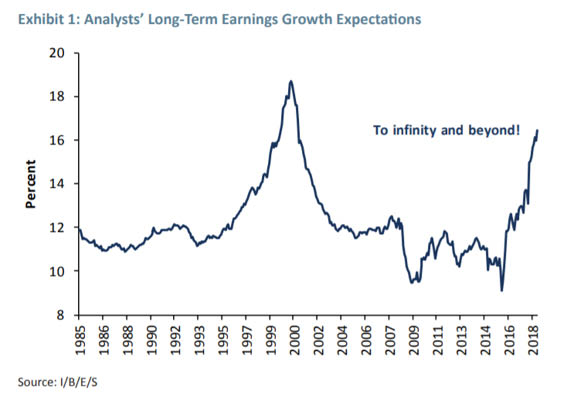

High Expectations James Montier, of the money-management firm GMO, demonstrates why stocks are so bullishly priced. It is because Wall Street researchers have become so giddy. In a December 2018 letter, Montier depicts the average expected five-year earnings-growth rate for publicly traded U.S. companies, as computed by I/B/E/S, has changed over time. The chart is grimly amusing.

- Source: Grantham, Mayo, & van Otterloo

An ill wind blows. From 1985 through 1997, Wall Street stock analysts held a steady opinion of five-year earnings growth. Then, in the late 1990s, as actual growth exceeded the 12% they had projected, the analysts' estimate became increasingly optimistic, peaking at 18% at the start of the new millennium. Recorded earnings then declined, leading them to cut their long-term estimates, which bottomed at 9% in year-end 2009 and then again seven years later.

Regrettably, Wall Street analysts have been a reliable indicator, in both directions. They have lagged, by raising their future estimates as their current economies strengthened, and they have led, by shouting "Left!" before the market turns right. Their long-term forecast was at its rosiest in 2000. Conversely, their earnings outlook was consistently muted during this decade's great bull market--until recently.

Deflating the Optimism I therefore concur with the experts assembled by Morningstar's Christine Benz that U.S. equity returns will probably lag their long-term averages over the next several years. Predictions for annualized large-company stock performance from Christine's seven sources range from 4% (BlackRock) to, ouch, negative 4% (GMO), with the median at 1%. Six of the seven sources expect similar or higher results from investment-grade bonds.

(Technically, BlackRock forecasts 7% nominal returns, to which I applied a 3% inflation haircut.)

Those forecasts, which are for periods ranging from seven to 15 years, implicitly assume that stock-market conditions will return to "normal" when the time horizon concludes. How equities will behave from those points forward is, of course, speculative. That depends greatly on global macroeconomic conditions. But it seems reasonable to me that once normalcy resumes, stocks will revert to something near their 60-year average.

Thus, my stylized outlook is to accept the experts' view of 1% in average inflation-adjusted annualized gains over the next 10 years, then 6% annualized for the succeeding 20 years. If so, that would make the annualized average for the full, 30-year period 4.3%. Per this prediction, U.S. equities from 2019 to 2048 will have annual real returns that are about 1 percentage point less than my parents' generation, and about 2 percentage points behind what I have enjoyed.

It's good to be me. That said, while the initial few years may be rough, this column's back-of-the-envelope analysis suggests that stocks should remain the purchase of choice for the patient, long-term investor, particularly if that investor suffers losses calmly. Some might be forthcoming.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)