3 Asset Classes That Still Hold Opportunities for Long-Term Investors

Morningstar Wealth experts say you haven’t missed out entirely on the market rally.

/s3.amazonaws.com/arc-authors/morningstar/efab5c51-f608-4afc-84c2-ddbd25cd7cde.jpg)

The first six months of 2023 in equity markets were nearly the polar opposite of last year’s experience. Stocks have entered a new bull market while pushing aside fears of recession and lower earnings.

A few major equity indexes are within a few percentage points of making new all-time highs. Considering the sentiment last October, all-time highs were unthinkable.

Naturally, many investors will ask themselves: Did I miss it?

A feature of investing is that there are always opportunities if you’re willing to do the homework and can stomach the volatility that often comes with where those opportunities are found.

The future is always uncertain, but there are select investing opportunities that still feel attractive for long-term investors.

At Morningstar Wealth, our process seeks to understand what’s been priced into markets and where opportunities might exist. Thus far in 2023, our work suggests that equity markets—particularly select growth companies in the United States—have already thrown a “Goodbye Inflation” party. So, even if the softest of landings is playing out in real time, we believe it’s wise to rotate into areas that weren’t invited to the party.

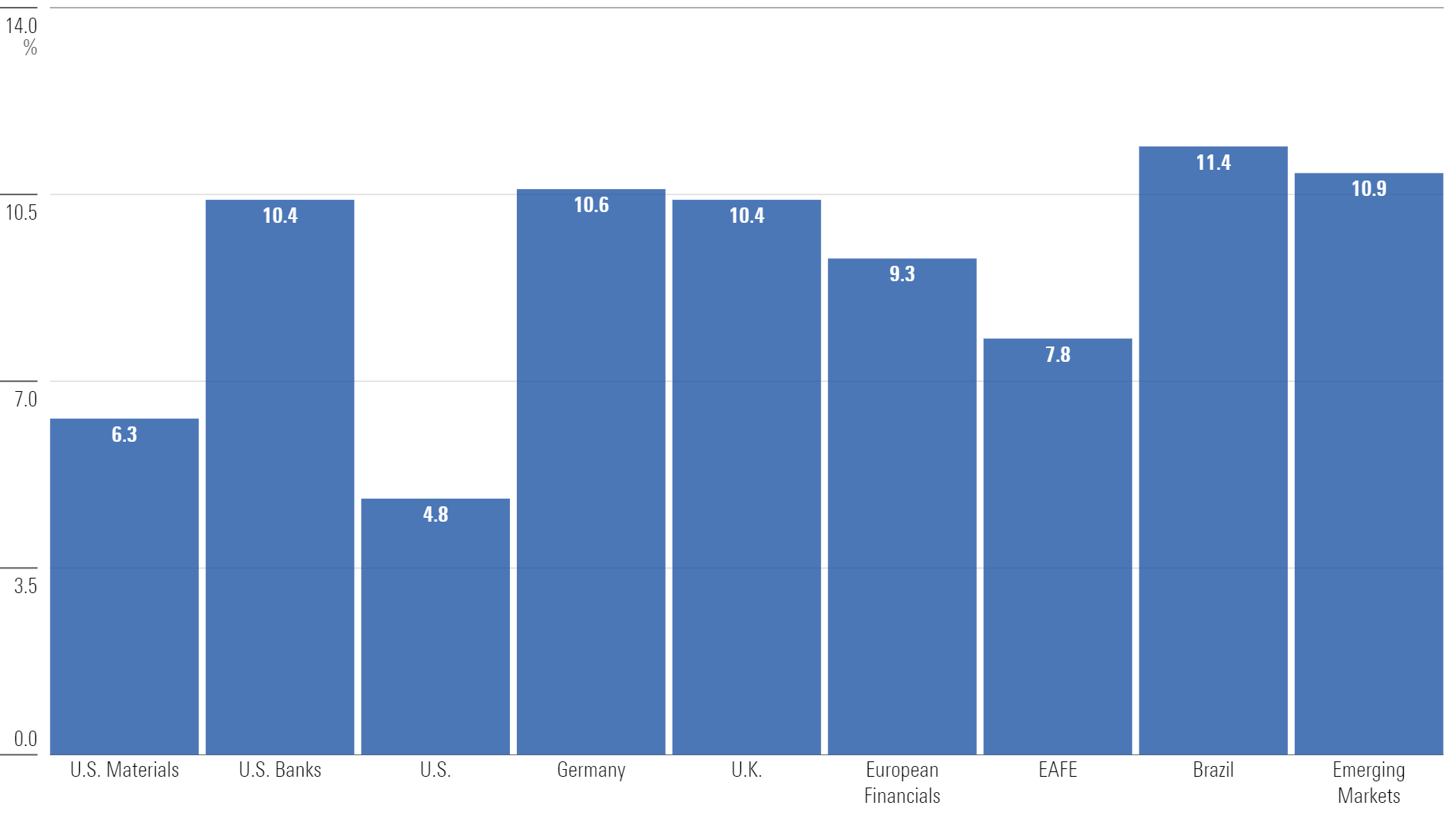

This leads us to some of the most interesting opportunities our research currently finds, which can be seen below in our forward-looking 10-year annualized return expectations for select equity markets.

Forward-Looking Return Expectations

Here are three asset-class observations that we believe are worth highlighting:

1) Emerging Markets

Extrapolating the recent past—specifically investment performance—is a common investor trait. U.S. stocks have trounced emerging markets for more than a decade.

Many investors might perceive U.S. stock outperformance as a fact of life.

But the long tail of history tells us markets are cyclical; every investment has its days in the sun and days in the shade. And history would indicate the next decade could be very different.

Look at the total return breakdown of four different periods between emerging markets and U.S. stocks over the past 25 years:

Total Return by Asset Class

Periods of extreme outperformance are common. But the pendulum swings in both directions, and as investors, we should do our best to prepare.

The structural story around emerging markets remains largely intact. Emerging markets represent 80% of the world’s population and nearly 70% of the world’s gross domestic product growth but only 11% of the total global equity market cap. There’s a compelling long-term investment story.

And many of the best emerging-markets opportunities happen at the individual country level. As we highlight in our global convictions document:

“We also need to remember that emerging markets are heterogeneous. Investors tend to bucket emerging markets as one, but often, the real opportunities present themselves at a country, sector, or regional level. For example, despite the many challenges confronting Chinese equities, both the absolute and relative valuation remains attractive.”

That doesn’t mean we’ll sell U.S. stocks and rotate blindly into emerging markets; rather, we think there’s an opportunity to increase exposure to emerging markets.

2) Europe: Sectors and Countries

Europe has faced a similar fate as emerging markets, which is to say, it hasn’t competed well from a return standpoint versus U.S. stocks. But the same historical patterns of performance observed in emerging markets are also true in Europe.

Going forward, we see reasons why Europe could be relatively resilient versus other major developed markets. High inflation and a harder economic fallout from the Russia-Ukraine war have been reflected in stock prices, creating compelling valuation opportunities.

While valuation comparisons between countries aren’t a perfect science, certain European countries and industry groups have some of the most reasonable valuations in the developed world.

Highlighting two examples from our global convictions document:

European financials: European indexes have a far greater weighting in financials, which have benefited from higher interest rates leading to earnings upgrades. In recent years, there were periods of time when interest rates in Europe were negative, meaning banks had to pay to keep their excess reserves stored at the central bank, rather than receiving interest income. Now that rates are normalizing, we believe stock prices have some catching up to do.

German stocks: Germany is Europe’s economic powerhouse, accounting for 25% of Europe’s GDP. The fallout from the Russia-Ukraine war—specifically less Russian energy coming to Germany—created fears of a deep recession coming for Germany, which stock prices began to reflect. Given the extensive headwinds and cyclical earnings (especially from the automotive sector), German stocks have been quite resilient, offering solid balance sheets and potential upside to earnings, without extreme valuations.

3) U.S. Banks

Markets are usually efficient—pricing assets correctly—but occasionally, situations arise that enable investors to buy great assets at deep discounts. The banking crisis in March seems to have been one of those situations.

Despite three bank failures, the banking system has been incredibly resilient. It likely should not have been labeled a banking crisis, but rather a crisis of a few banks.

Jamie Dimon—CEO of JPMorgan Chase JPM, the largest U.S. bank—summarized his view in his shareholder letter, simply stating:

“Most of the risks were hiding in plain sight.”

The “risks” he was referencing were twofold:

- A rapid rise in interest rates damaged bank bond portfolios.

- Large numbers of uninsured deposits sat alongside concentrated depositor bases—mostly venture capital-controlled companies—that ran in the same social circles and coordinated pulling deposits.

While most bank fundamentals held steady, their share prices did not. It was a “throw the baby out with the bath water” situation from a market perspective. The regional banking index fell nearly 40% peak to trough through the beginning of May. Since then, the banks have rallied but remain in bear-market territory from the onset of the problems in early March.

For investors, we believe there’s more room to run. While technology stocks capture most of the market’s attention, unloved and oversold banking stocks have the potential to deliver meaningful future returns.

A more detailed summary of Morningstar Wealth’s asset-class views can be found here.

Morningstar Investment Management LLC is a Registered Investment Advisor and subsidiary of Morningstar, Inc. The Morningstar name and logo are registered marks of Morningstar, Inc. Opinions expressed are as of the date indicated; such opinions are subject to change without notice. Morningstar Investment Management and its affiliates shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Before making any investment decision, please consider consulting a financial or tax professional regarding your unique situation.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KWYKRGOPCBCE3PJQ5D4VRUVZNM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TZEZ6FJNTZEZRC3FBWCWXTXVOQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/efab5c51-f608-4afc-84c2-ddbd25cd7cde.jpg)