The Workers’ Guide to Retirement Income

A brief overview of the topic for those who have not yet retired.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

The Situation

Newly minted retirees occupy three economic tiers: 1) those who will rely mainly on Social Security payments; 2) those who have additional monies but who still face the possibility of outliving their assets; and 3) those who inevitably will leave significant estates.

This column addresses the middle group, as the first requires spending advice more than investment counsel, while the third, strictly speaking, needs no help at all. (Nonetheless, that third group is the primary audience for financial professionals.)

Assume a married couple has begun to draw monthly Social Security payments. Each spouse is 65 years of age, and the couple holds $800,000 in investment assets. How should the couple convert that lump sum into income? What are the primary choices?

Choice #1: Buy Treasuries

Traditionally, retirees sought the safety of Treasury securities. Although unsophisticated, this was a reasonably sound strategy. Treasuries paid handsomely--well above what stocks delivered--while being guaranteed by the U.S. government. Retirees who held Treasuries until their bonds and notes matured faced no principal risk and thus possessed few worries.

With that approach, the real value of a retiree's capital eroded. Fortunately, inflation's effect was less damaging than advertised because, for most retirees, the longer their retirement, the less they spent. True, sometimes this decline occurred by necessity, as reduced purchasing power crimped their spending habits, but for the most part it happened naturally due to health concerns.

Regrettably, time has ravaged the Treasury strategy. Had couples through time placed $800,000 into 10-year Treasury notes, those who retired in January 1970, 1980, 1990, and 2000 would have generated hefty monthly incomes of $5,240, $7,333, $5,327, and $4,527, respectively. In contrast, today’s couple would earn a mere $1,113. The price for investment safety has become exorbitantly high.

Choice #2: Boost Income

Unlike in the past, retirees cannot simultaneously: 1) generate substantial income, 2) without touching their capital base, 3) while receiving a government guarantee. However, they may still achieve those first two goals, should they jettison the third. That is, retirees can buy investments that generate sufficient yield so that they need not supplement their income by dipping into their investment capital.

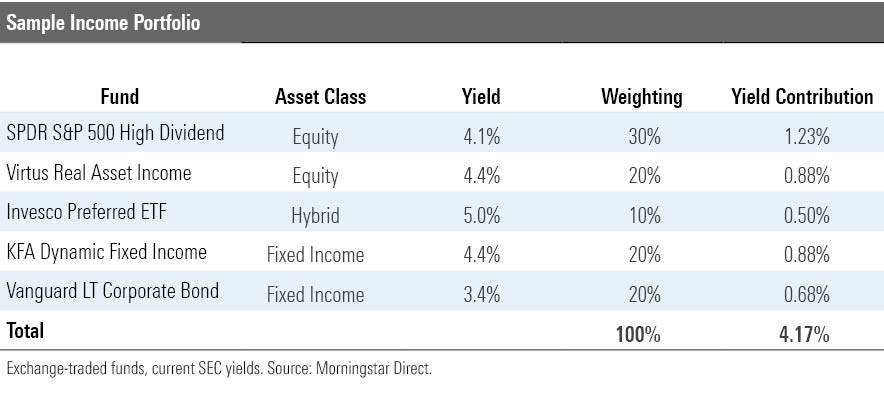

For example, our couple could buy a portfolio consisting of the following exchange-traded funds, which would collectively yield 4.17%. The monthly income on the $800,000 investment would be $2,780--far below what 10-year Treasuries paid during bond investors’ glory days but more than double Treasuries’ current level.

The danger with this approach is that although the portfolio ostensibly is diversified, holding both stocks and bonds, almost all the holdings are economically sensitive. Of course, my investment suggestions could readily be altered, but the conclusion would remain intact. Particularly now, with inflation fears abated, so that long investment-grade bonds no longer pay very much, there’s no real way to achieve high yields without courting recession risk.

For that reason, “spend income and maintain capital” strategies are quietly hazardous. Unless the retiree is willing to slash the portfolio’s income by seeking proper diversification, such approaches tend to get clocked by economic slowdowns. Sometimes the losses are merely temporary, but on other occasions they are permanent, caused by corporate bankruptcies. That’s a tough way to live.

Choice #3: Spend Capital

A more prudent path is to accept lower portfolio income, then supplement those receipts by gradually removing investment capital. Psychologically, this tactic can be difficult. As financial advisor and author Michael Kitces explains, those who spend their working years increasing their assets tend to dislike doing the opposite. Growing one's wealth is enjoyable; shrinking it, not so much.

Investing 50% in a broad U.S. stock market index and 50% in high-grade bonds makes for a 1.5% overall yield, which means that, to match the payout from the income portfolio, our couple would need to spend 2.67% of their capital during their first year of retirement. As U.S. stocks over the past century have posted annual price gains of slightly more than twice that amount, growth from the 50% of portfolio held in stocks would more than compensate for the lost principal. On average, our couple will fare just fine.

In practice, though, the financial markets fluctuate. Consequently, the “spend capital” tactic must be flexibly implemented. Those who adopt this approach will need to reduce their withdrawals after equity prices have fallen significantly, thereby avoiding the vicious cycle of raiding a declining asset base. With luck, lost ground will be recouped later. But unlike with the strategy of owning Treasuries, there are no guarantees.

Choice #4: Annuitize

Another possibility for those willing to part with their capital is to annuitize by buying a contract that promises future payments. While such investments come with a cost--just because they lack official expense ratios doesn’t mean that the insurer provides its services for free--they boast the benefit of pooled resources. A group of people can insure themselves more efficiently than can an individual.

There are several ways to use annuities. One is to buy an immediate lifetime annuity. Currently, a 65-year-old couple can earn about 4.8% annually on a joint lifetime annuity, to be paid until both parties have died. If our couple were to place $650,000 into that joint annuity and the remainder into equities, they would match the income portfolio’s yield, while retaining $150,000 that could be used for portfolio growth.

Conversely, the couple could buy a deferred annuity. The purchase occurs today, but the benefit is paid in the future. For example, the couple could devote $300,000 of the portfolio toward a joint deferred annuity that would pay $3,000 per month, starting at age 80. That would cut their current portfolio to $500,000 from $800,000, but that half million would only need to last for 15 years because, after that date, the deferred annuity would fully meet their needs.

Annuitizing is even harder psychologically than dipping into capital because the retiree forgoes a bigger chunk of money when annuitizing, which will never return. Also, the decision to annuitize can be complex, given how many options exist. For these reasons, the tactic isn’t very popular. However, it is worth considering. There is an advantage to locking down income, thereby freeing the remaining assets so that they can be invested for capital appreciation.

Wrapping Up

By design, this column surveys the topic of retirement income from the stratosphere. It will surprise nobody who works in the field. However, from my experience, workers who haven’t yet thought about how to convert their investment assets into income during retirement often struggle to find articles that lay the groundwork. This one makes that attempt.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6NPXWNF2RNA7ZGPY5VF7JT4YC4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RYIQ2SKRKNCENPDOV5MK5TH5NY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)