Putting the Olympics on Hold Isn't Keeping ETF Investors From Going for Gold

Gold ETFs stood atop the podium in July.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

Stocks ended July within spitting distance of their all-time high. At month-end, the Morningstar Global Markets Index--a broad gauge of global stock markets--had rebounded 40.5% from its recent low and sat just 4.5% below its mid-February peak. The index has declined 2.2% through the first seven months of the year. The bond market has stabilized since the U.S. Federal Reserve’s late-March intervention. After briefly dropping into negative territory earlier in the year, the Morningstar U.S. Core Bond Index was up 7.7% for the year to date by month’s end.

Here, I will take a closer look at how the major asset classes performed last month, where investors were putting their money, and which segments of the market look cheap and dear--all through the lens of exchange-traded funds.

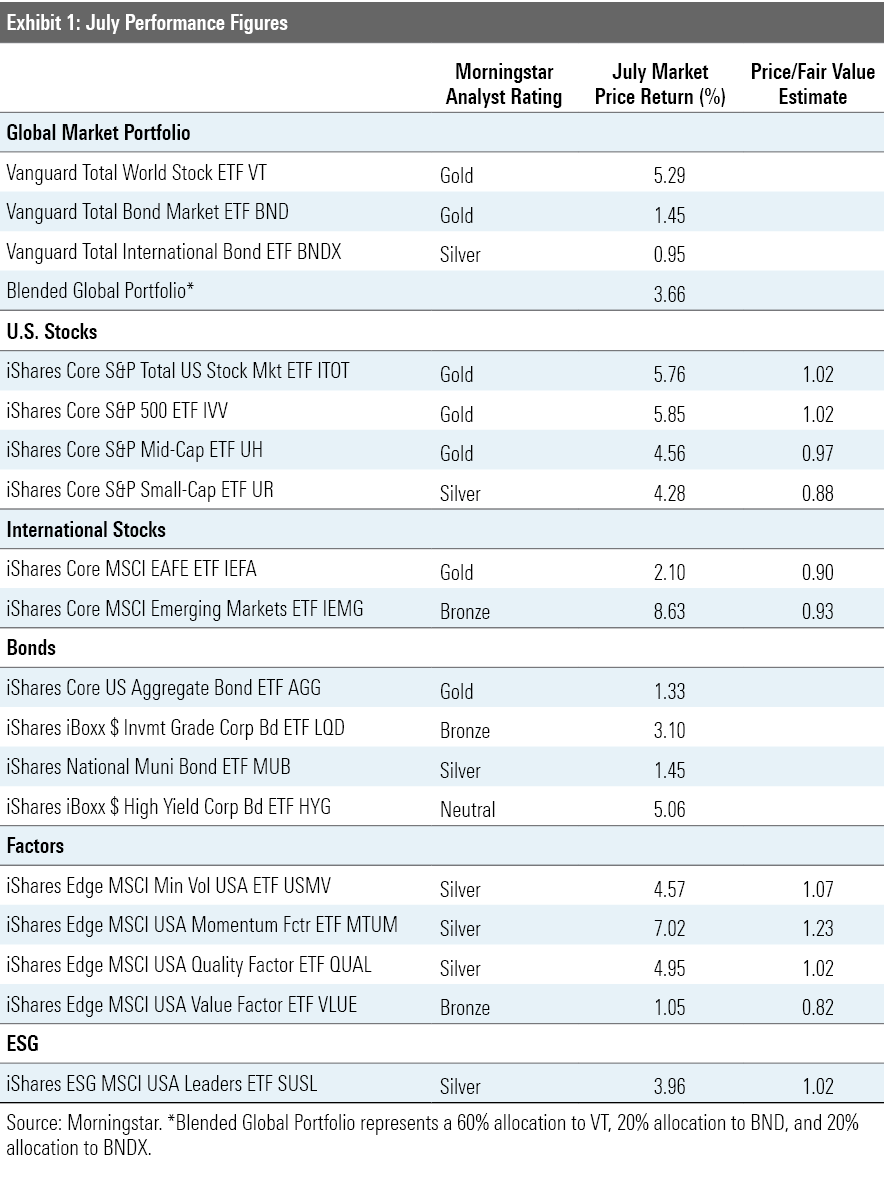

After Another Month of Gains, U.S. Stocks Look Fairly Valued Exhibit 1 features July performance figures for a sampling of Morningstar Medalist ETFs representing most major asset classes. Investors in a blended global market portfolio gained 3.7% during the month. Stock markets were up across the board. U.S. stocks, as proxied by iShares Core S&P U.S. Total Stock Market ETF ITOT inched into overvalued territory, as measured by the fund's Morningstar Price/Fair Value Estimate. Meanwhile, even after making significant gains in recent months, both developed ex U.S. (represented by iShares Core MSCI EAFE ETF IEFA) and emerging-markets stocks (iShares Core MSCI Emerging Markets ETF IEMG) still look somewhat cheap.

Emerging-markets stocks once again outperformed both developed international and U.S. stocks in July. But foreign stocks’ short-term gains haven’t been enough to alleviate investors’ long-term pain. Over the trailing five years through July, ITOT outgained IEFA by 8.4 percentage points annually and IEMG by about 5.4 percentage points per year. International diversification may be a smart idea, but it has smarted for a while now.

U.S. large caps were back on top in July. IShares Core S&P 500 ETF IVV outstripped its mid- and small-cap counterparts and finished the month trading at a 2% premium to Morningstar’s fair value estimate for its constituent stocks. Much of IVV’s monthly gains were driven by three of its four largest holdings. Apple AAPL, Amazon AMZN, and Facebook FB jointly accounted for one third of the fund’s July performance. This is not a new development. The S&P 500’s largest stocks have been carrying most of the water for a while now, and the index has become increasingly concentrated as a result--recently surpassing levels of concentration last seen at the height of the dot-com bubble.

The performance spread across the diagonal of the Morningstar Style Box flared once again in July. IShares S&P 500 Growth ETF IVW, which falls in the large-growth Morningstar Category, outperformed small-value resident iShares S&P Small-Cap 600 Value ETF IJS by 4.6%. For the year to date through July, IVW has outperformed IJS by nearly 38%. IJS has fallen more than 22% in 2020, trying the patience of even the most dedicated value investors.

Most sectors of the bond market have recovered their first-quarter losses. The exceptions are the most credit-risky sectors like high-yield corporates, high-yield munis, and bank loans, all of which posted gains in July but remain underwater for the year.

Credit markets--and bond ETFs--snapped back into order following the Federal Reserve's late-March intervention. In May, the Fed began purchasing corporate-bond ETFs as part of its previously announced plan to backstop the bond market with its Secondary Market Corporate Credit Facility. Between May 12 and June 29, the Fed purchased shares of 16 different corporate-bond ETFs with a total market value of $7.9 billion. The Fed hasn’t been alone in buying bond ETFs; after another big month of inflows in July, they are on pace to see record annual flows.

Strategic-beta ETFs representing a variety of individual factors had a mixed showing versus the broader U.S. stock market. Value stocks suffered again, while momentum picked up steam. Through the first half of the year, iShares Edge MSCI USA Value Factor ETF VLUE has fallen 17.2%, while iShares Edge MSCI USA Momentum Factor ETF MTUM has gained 12.5%, outperforming the broader U.S. market. At the end of July, VLUE was trading at an 18% discount to its Morningstar fair value estimate, while MTUM was priced 23% higher than our analysts' assessment of its intrinsic worth.

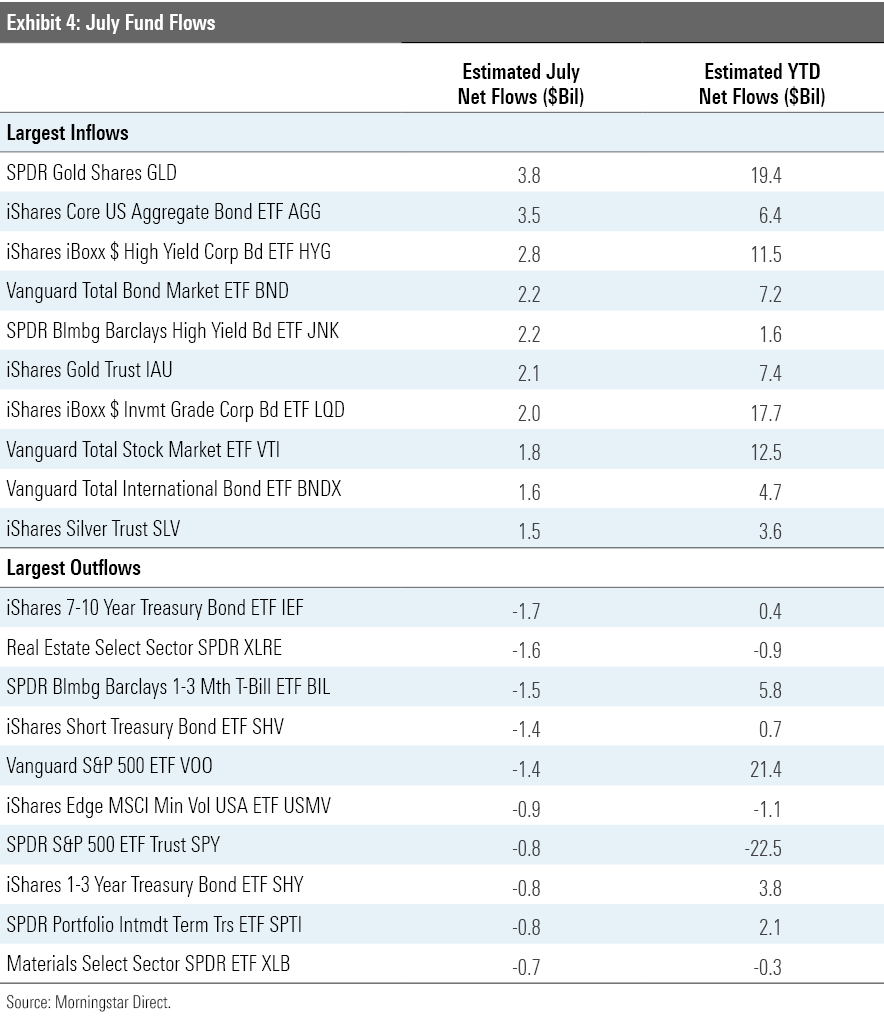

Going for the Gold Physical gold ETFs continued to gain assets from safe-haven seekers, inflation worriers, and performance-chasers alike. SPDR Gold Shares GLD topped the asset flows ranking as it amassed another $3.8 billion in net new inflows in July. This marked the eighth straight month that GLD has seen net inflows. In sum, investors have poured nearly $20 billion in new money into GLD over this stretch. With $78 billion in assets, GLD is as big as it's ever been, recently eclipsing its prior peak in assets reached during the years following the global financial crisis.

GLD wasn’t the only shiny object coveted by investors in July. IShares Gold Trust IAU raked in $2.1 billion in net new money, bringing its year-to-date total to $7.4 billion. Silver also shone. As the metal’s price spiked, so did flows into iShares Silver Trust SLV, which amounted to $1.5 billion for the month.

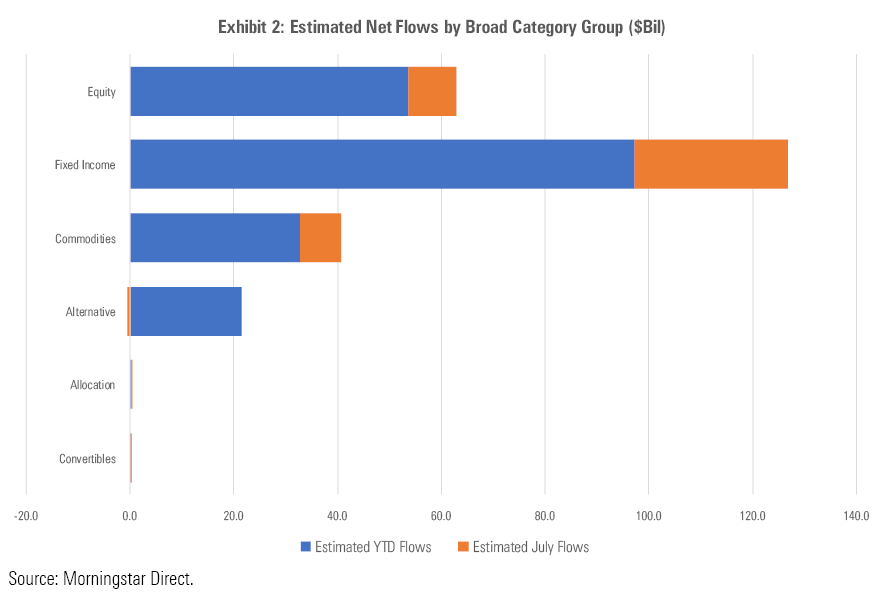

ETF flows have continued to flood bond funds after the Fed put a bid under the market in March. Fixed-income ETFs took in $29.6 billion in net new flows in July, down from June’s $33.5 billion, which marked a monthly record. Over the past four months, estimated net flows into fixed-income ETFs amounted to just over $114.1 billion. This is the largest four-month net flow into bond ETFs on record by a large margin.

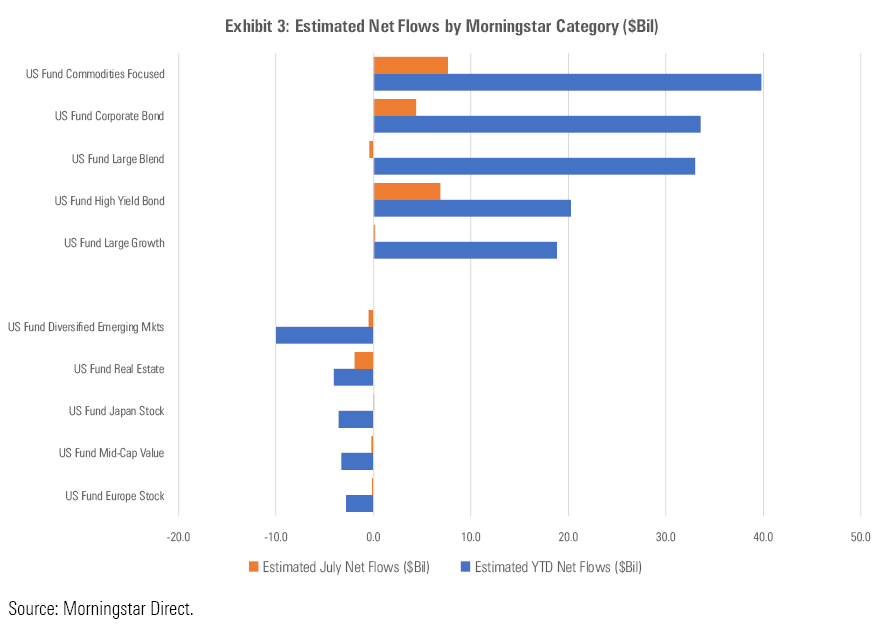

Stock ETFs saw modest inflows in June, totaling $9.2 billion. Flows into more-concentrated stock ETFs have increased amid the recent market volatility. In July, ETFs in the technology, energy, consumer cyclical, and health categories together pulled in nearly $5 billion in assets as more investors are plunking down sector-level bets. After a brief respite in June, outflows resumed among emerging-markets stock ETFs. The diversified emerging markets category has seen the largest outflows of any category this year, with just over $10 billion being yanked from these funds.

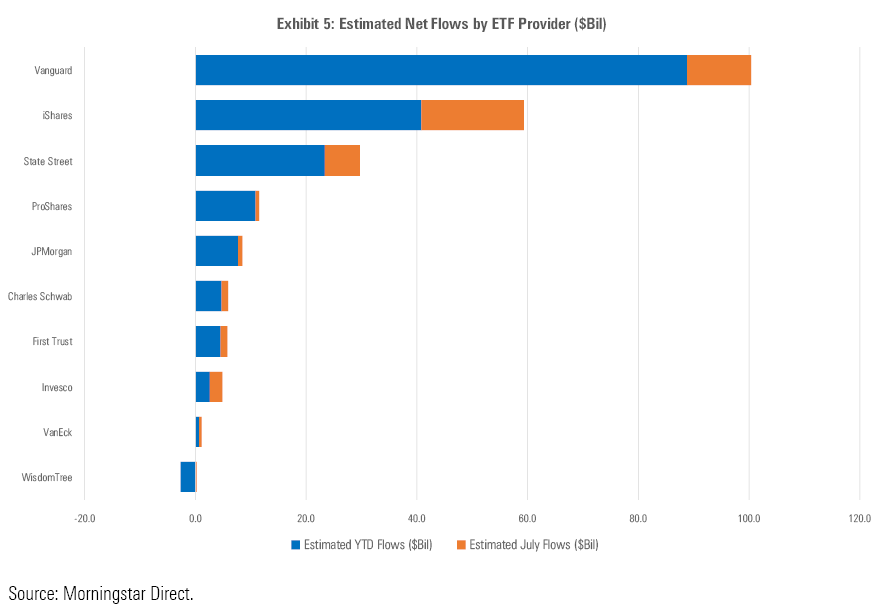

Vanguard’s clients have continued to put money to work. The firm’s year-to-date ETF flows are slightly greater than the sum of its four largest rivals. At least some portion of Vanguard’s ETF flows have resulted from conversions of assets in the firm’s Admiral share class to ETF shares, which, following a wave of repricing that was implemented over the past year, are now cheaper than Admiral shares of the same funds.

Following a three-month streak of outflows, Schwab’s ETF lineup experienced a small inflow in July. That three-month stretch broke the firm’s long record of steady net inflows, which had gone unbroken from their 2009 inception through April of this year. Outflows were likely driven by changes to the firm’s own proprietary ETF model portfolios. For example, as of March 31, Charles Schwab Investment Advisory was the largest owner of the Schwab Intermediate-Term U.S. Treasury ETF SCHR. The fund has seen the largest outflows of any ETF in Schwab’s stable for the year to date through July, with $1.62 billion withdrawn. Based on data from CSIA’s recent 13-F filings, it held 42.7 million shares of SCHR as of the end of March and had sold 5.7 million shares in the first quarter of 2020 (about 12% of its stake as of the end of 2019).

GLD has carried State Street through much of 2020. Flows into the world’s largest gold-backed exchange-traded product have accounted for nearly two thirds of the firm’s year-to-date total. Flows into the firm’s Select Sector SPDR suite have further bolstered its position.

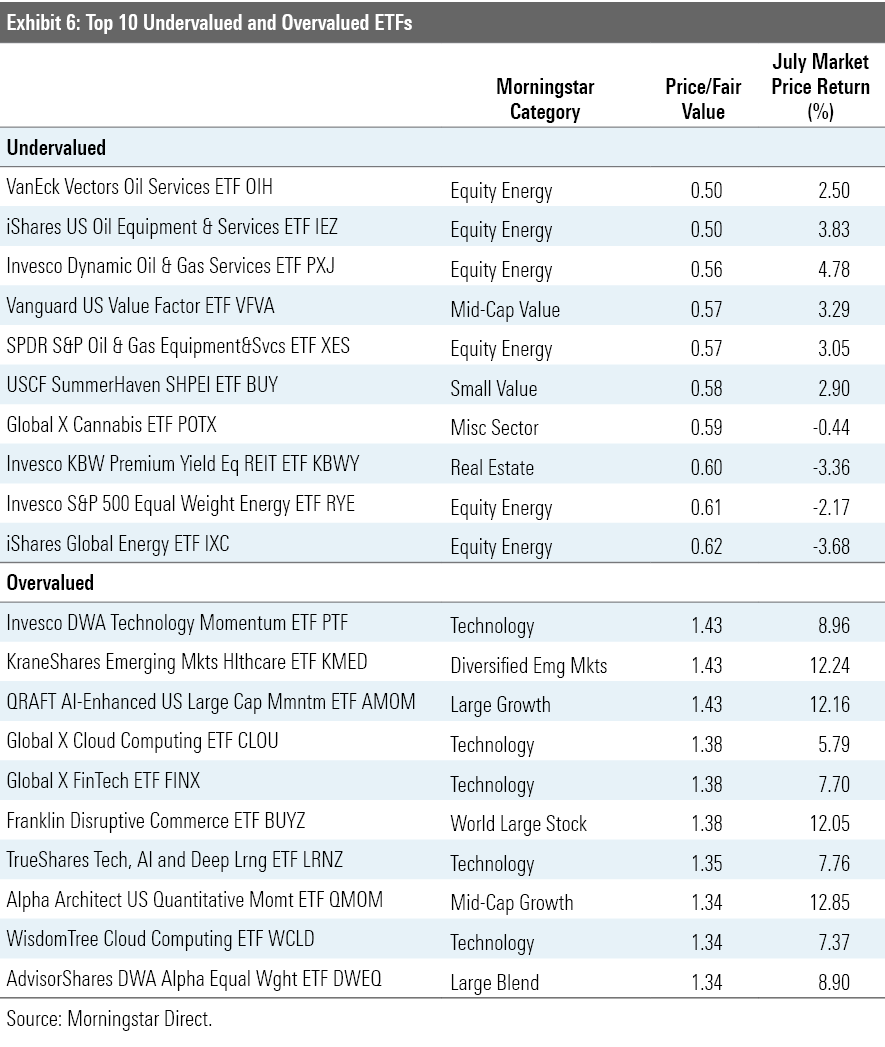

There Appears to Be Value in Value, While Tech Looks Toppy The Morningstar fair value estimate for ETFs rolls up our equity analysts' fair value estimates for individual stocks and our quantitative fair value estimates for those stocks not covered by Morningstar analysts into an aggregate fair value estimate for stock ETF portfolios. Dividing this value by the ETFs' market prices yields a price/fair value ratio. This ratio can point to potential bargains and areas of the market where valuations are stretched.

Exhibit 6 features the 10 ETFs that were trading at the largest discounts and premiums to their fair value estimates as of the end of July. Six of the funds trading at the largest discounts belong to the equity energy category. Pain has been pervasive in the energy sector this year as demand has declined and supply has continued to flood the market. As producers ran out of places to store their output, prices collapsed, as did the share prices of firms operating in the oil- and gas-service industry.

But the market is a discounting mechanism, and just as the oil patch appeared to be on the brink, many investors began wagering that the worst had passed. After a sharp rebound off the bottom, oil prices have normalized and energy stocks’ gains have stalled. In July, Energy Select Sector SPDR ETF XLE, which holds the energy names in the S&P 500, fell 4.8%. While the sector has come back from the edge, many energy names are still trading at steep discounts.

Tech stocks have been on a tear this year, so it is no surprise to see a number of tech-focused funds among the ranks of the most overvalued ETFs. Notable among them are Global X Cloud Computing ETF CLOU, WisdomTree Cloud Computing ETF WCLD, and Franklin Disruptive Commerce ETF BUYZ. All three funds were more than 30% overvalued as of the end of July. Investors’ enthusiasm for the stocks these funds own has grown amid a worldwide lockdown that’s forced many to work, shop, and live online.

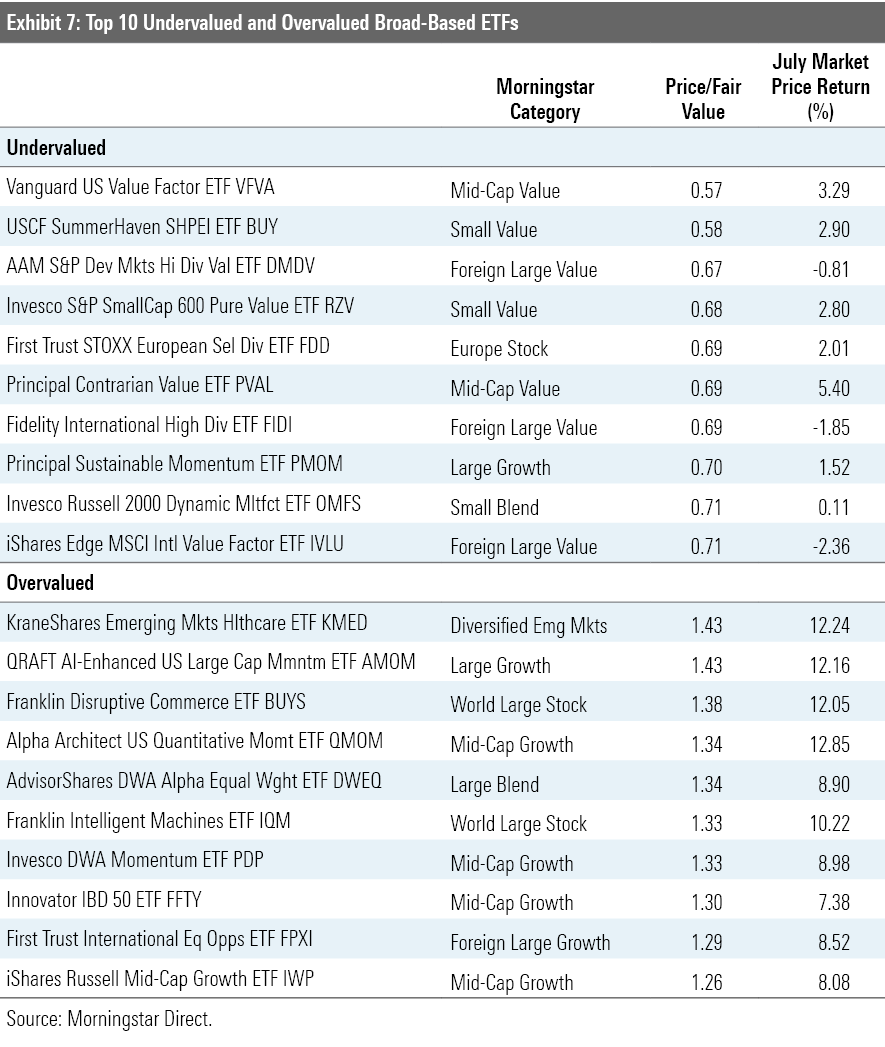

Exhibit 7 features the 10 broad-based (those ETFs belonging to one of the mainline Morningstar Style Box or other broader geographic categories) that were trading at the largest discounts and premiums to their fair value estimates as of month end. The common thread among the most undervalued funds is an orientation toward smaller, cheaper stocks. Some of them deliberately lean into value by virtue of selecting and weighting stocks based on their relative cheapness. This is the case for funds like Vanguard U.S. Value Factor ETF VFVA and Invesco S&P SmallCap 600 Pure Value ETF RZV. There are also four value-oriented funds that invest in international stocks featured on this month’s list. Notable among them is iShares Edge MSCI International Value Factor ETF IVLU, the foreign cousin of VLUE, which has a Morningstar Analyst Rating of Silver. Like its U.S. cousin, IVLU takes a sector-neutral approach, sweeping in the cheapest stocks within each sector and weighting them based on a combination of their market cap and the strength of their value characteristics. The result is a portfolio with a strong and consistent value orientation.

The most overvalued broad-based ETFs include a number of funds with a momentum focus. Alpha Architect U.S. Quantitative Momentum ETF QMOM and QRAFT AI-Enhanced U.S. Large Cap Momentum ETF AMOM both spin highly concentrated, high-octane momentum portfolios by design. Folding in names that are priced at premium multiples is embedded in these funds’ DNA. KraneShares Emerging Markets Healthcare ETF KMED finished the month trading 43% above its Morningstar fair value estimate. The fund has gained 42% for the year to date as investors have plunked down big bets on the pharmaceutical, biotech, and medical devices firms that are working feverishly to cultivate a cure for the pandemic that’s ailing us all.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)