Navigating ETF Discounts and Premiums During Turbulent Times

Recent market volatility has led to extraordinary dislocations in ETF prices.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

Editor's note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

Key Takeaways

- Market volatility has caused many exchange-traded funds to trade at extreme discounts to their net asset values.

- ETF investors should understand ETF premiums and discounts and how to best navigate them.

- If possible, ETF investors should avoid trading during unstable periods in the market. If they must trade, using limit orders is a best practice. And for those investors that don't place any value on ETFs' intraday liquidity, mutual funds offering similar exposure are perfectly suitable options.

Investors Are Flocking to ETFs As markets have been roiled by the spread of the coronavirus and flailing to price the implications for economic growth and corporate earnings, ETF trading has spiked. Shares of SPDR S&P 500 ETF SPY, the oldest and largest U.S. ETF, have changed hands in record volumes. On Feb. 28, 2020, SPY's trading volume hit $114 billion--an all-time high, equivalent to 5.6 times its average daily volume during 2019 and representing 43% of its assets under management. According to Bloomberg data compiled by BlackRock, ETF trading accounted for 38% of all equity volume on U.S. exchanges from Feb. 24 through March 13. This compares with an average of 27% in 2019. What explains this uptick?

ETFs are a dynamic investment wrapper. They can be used by long-term investors as low-cost, tax-efficient portfolio building blocks. They have penetrated actively managed funds as a means of maintaining market exposure and managing liquidity needs. They can be sold short by those with a bearish view. And they've become an additional layer of liquidity in fixed-income markets, stepping in where traditional bond market participants have stepped out in the post-financial-crisis period. Given these funds' diverse use cases and user base, it is no surprise that investors of all stripes have flocked to them in a market that--to put it lightly--has been liquidity-challenged.

Unprecedented Dislocations ETFs trade like stocks. Investors pay or receive the going market price for their shares. These prices tend to hew closely to the value of their underlying assets. ETF market makers make sure of this. They are the linchpin of the ETF ecosystem. They quote bid and ask prices for ETF shares and compete with one another to profit from any discrepancy between the funds' share prices and their own estimates of the value of the funds' assets.

In normal market conditions, market makers face little risk and ample opportunities to collect profits from keeping prices in check and pocketing bid-ask spreads in exchange for connecting ETF buyers and sellers. But these aren't normal conditions. Today, the risk market makers face has flared and the demand for their ability to price them has peaked. As a result, they are having greater difficulty and facing bigger risks pricing ETF portfolios and are quoting wider bid-ask spreads.

In the early days of the current market meltdown, ETFs were weathering the storm well. While bid-ask spreads and premiums and discounts widened, they remained within normal ranges.

During the week of March 9, as the going got tougher, many ETFs saw their prices come unmoored from their NAVs. This owed to a variety of factors, but tumult in the Treasury market played a big role. The impact was immediate and significant. The March 12 closing prices for Vanguard Total Bond Market Index ETF BND, iShares Core U.S. Aggregate Bond ETF AGG, and Schwab U.S. Aggregate Bond ETF SCHZ represented respective discounts to the funds' NAVs of 6.2%, 4.4%, and 6.3%. In all cases, these were well, well outside of normal ranges--none of these funds had ever seen discounts of this magnitude.

To be clear, these funds were not alone--abnormally large premiums and discounts have been pervasive. In one extreme case, VanEck Vectors High-Yield Municipal Index ETF HYD closed at a 19.3% discount to its NAV on March 12. But I chose to highlight these three because they are among the largest funds offering access to the most liquid segments of the fixed-income markets. BND is the ETF share class of the world's largest bond fund. These are not the funds that anyone--myself included--would have expected to behave as they have in stressed markets.

What are investors to make of all of this? How should they respond? Before I dive into the details, I think it is worth revisiting the basics of ETF premiums and discounts.

What Is NAV? Net asset value is the total value of an ETF's assets less the total value of its liabilities. The composition of an ETF's assets will vary but will generally comprise stocks, bonds, and/or cash. If the fund uses physical replication to track its benchmark (that is, it owns securities, not derivatives), the assets are the component securities (or a sampling thereof) of its benchmark index, any accrued income generated through securities lending, and some cash. Liabilities for ETFs and other funds will largely consist of fees owed to the fund company. An ETF's NAV per share can then be calculated by dividing the total NAV of the fund by its number of outstanding shares.

NAV = (Total Value of Assets - Total Value of Liabilities) / Number of Shares

What Is iNAV? Traditional open-end mutual funds calculate their NAV once per business day, after most exchanges have closed and third-party pricing services have disseminated up-to-date price information for various securities. Funds use that value as the price for new purchase or redemption orders placed throughout the day. New investors will purchase fund shares at end-of-day NAV (less any fees), and investors exiting funds will also do so at end-of-day NAV (again, less any fees). This single price for purchases and sales, set using end-of-day prices for all the assets in the portfolio, helps make purchases of traditional funds simple and typically fair.

ETFs offer intraday liquidity. They are priced throughout the trading day and purchased or sold at the prevailing market price. Thus, a regular intraday measure of these funds' NAV can be (somewhat) useful in gauging what (some) portfolios are worth during the trading day. This in turn can help investors see whether they are paying or receiving a fair price.

This intraday portfolio value is called the fund's indicative net asset value, or iNAV. The iNAV is calculated at regular intervals (usually every 15 seconds) throughout the course of the trading day. However, unlike traditional open-end mutual funds, ETF investors trading during market hours will not transact at the most recent iNAV (which is mostly symbolic, a touchstone of sorts). Instead, ETF investors will likely execute their trades at a premium or discount to a fund's true value.

Premiums and Discounts ETFs' market prices will generally not track their NAV nor market makers' own estimate of their value in lock step. If a fund's market price is higher than its NAV, it is said to be trading at a premium, which is good for sellers and bad for buyers. Paying $50.49 for a fund whose component securities are worth $49.99 in aggregate will inherently harm your expected returns. When the market price is lower than the current value of the portfolio, the ETF is trading at a discount, which helps buyers and harms sellers. Paying $49.99 for a share in a fund whose component securities are worth $50.49 could only improve your expected returns.

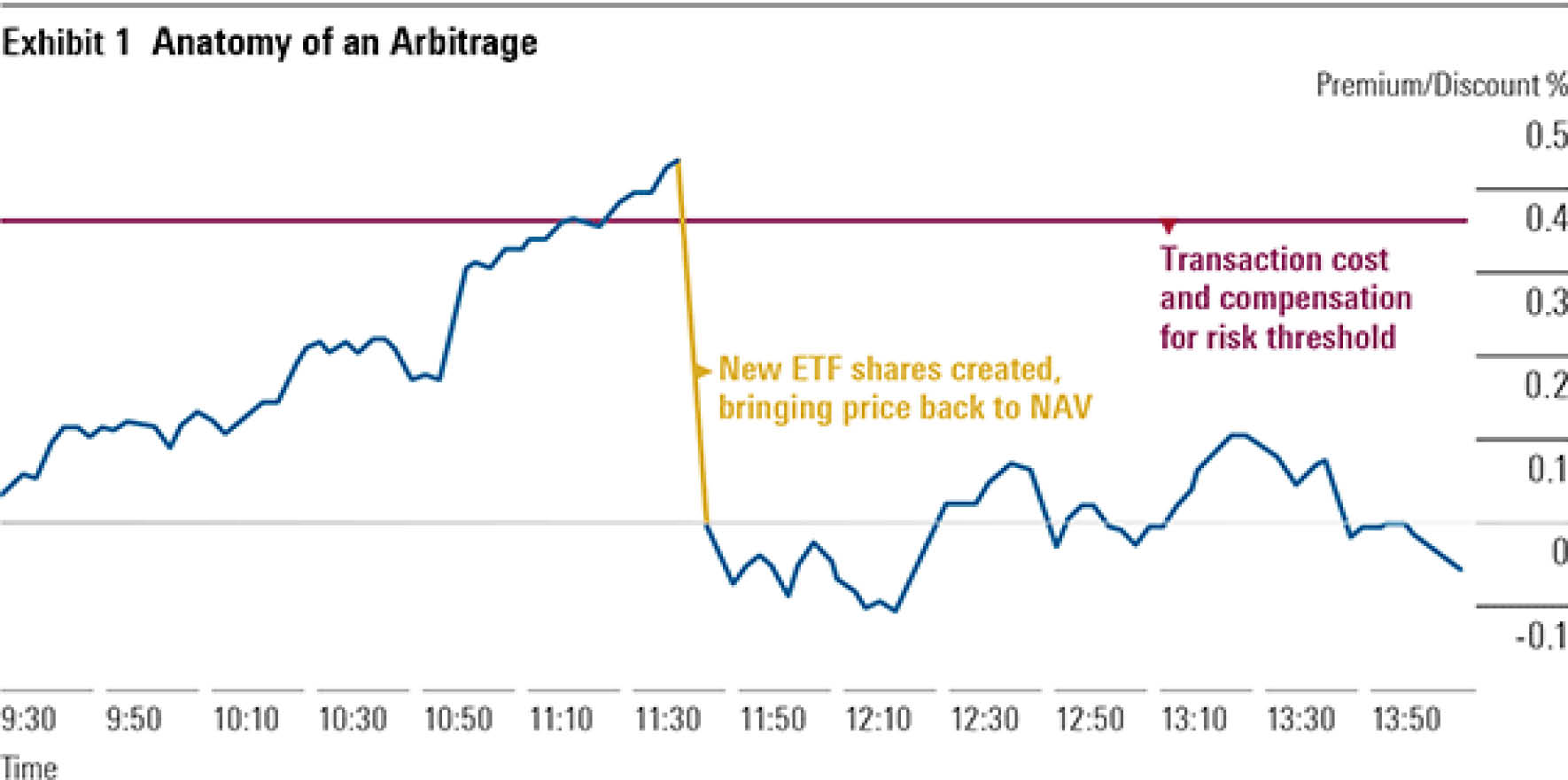

Luckily, ETFs typically trade at prices that are very close to their NAV. Even the examples above, of a 1% premium or discount, would be an exaggeration for nearly all ETFs. This is because any premium or discount that arises presents an arbitrage opportunity for authorized participants, or APs--a special "breed" of market makers with the ability to create and redeem new ETF shares directly with a fund's sponsor. APs are able to create and redeem ETF shares by exchanging a predetermined basket of securities and/or cash for new ETF shares and vice versa. If an ETF's market price strays too far from its NAV, market makers will move to profit from the relative mispricing between the fund's market price and the aggregate price of its underlying securities.

For example, if the component securities of a given fund are worth $49.99 per ETF share and the ETF's shares are changing hands for $50.49 each, a market maker can deliver that basket of securities to the ETF provider in exchange for new ETF shares and subsequently sell the new ETF shares on the open market. The market maker will pocket a small profit for the effort (which will likely be less than $0.50 per ETF share given the costs involved in this process). As market makers compete for these opportunities to make a quick low-risk profit, they serve to minimize the size and persistence of premiums and discounts for the fund's shares.

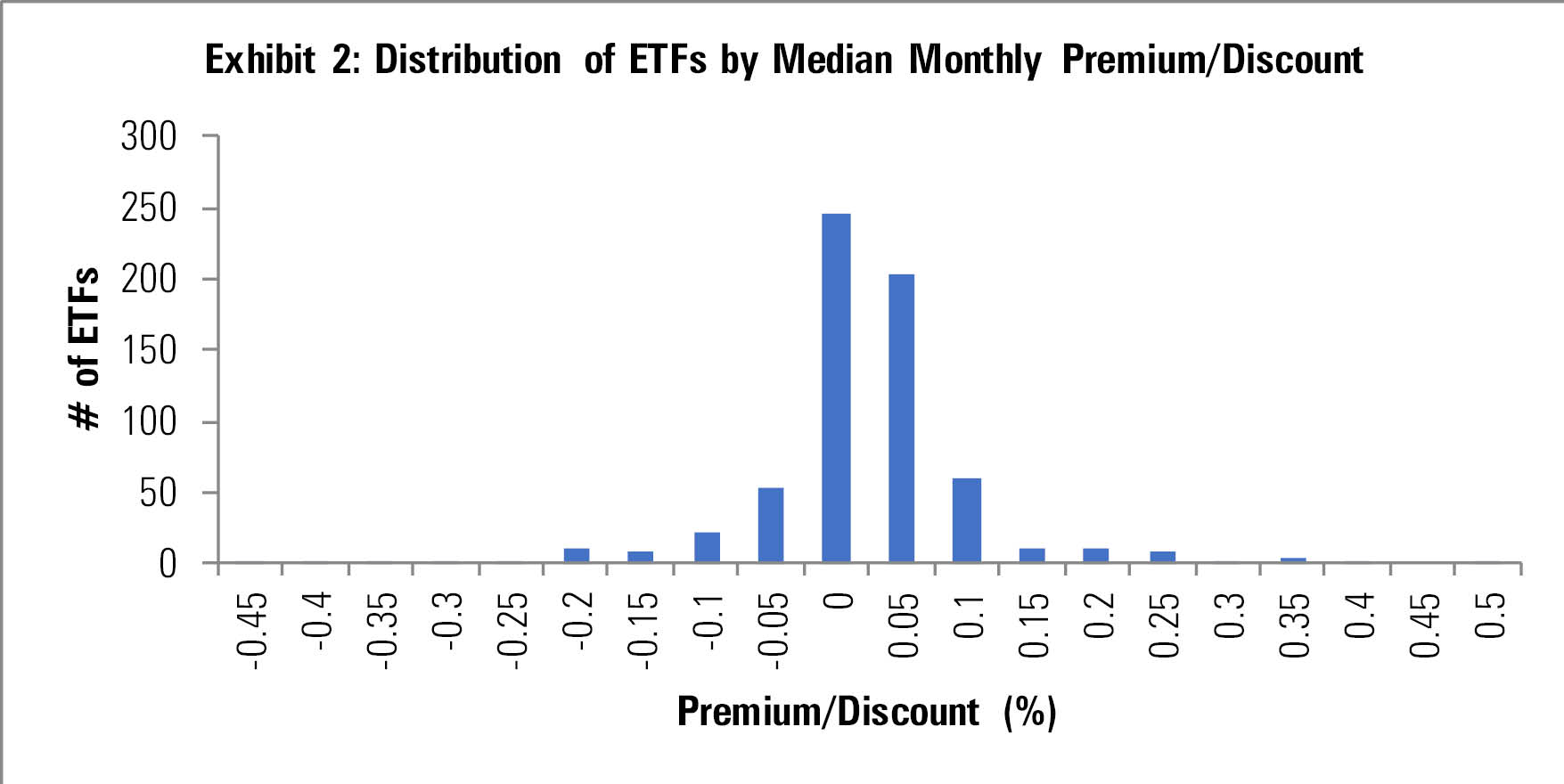

Source: Morningstar.

Exhibit 2 is a testament to APs' hard work. It is a histogram showing the distribution of the median of monthly premiums and discounts for the 645 ETFs for which Morningstar has this data available going back 10 years. You'll notice that sizable and persistent premiums and discounts are the exception rather than the rule. In fact, 500 (78%) of the ETFs in this group have tended to trade at a premium/discount to their NAV that ranged from negative 0.05% and 0.05% during the period in question. But there are exceptions to account for.

Source: Morningstar Direct. Data from March 2010 through February 2020.

Examples of Persistent Premiums and Discounts Of the 645 ETFs included in the sample I've referenced above, those that have exhibited the largest and most persistent premiums and discounts share some common characteristics. Of the 20 funds that had the largest median premium or discount during the past decade, 12 were international- or global-equity funds. Some or all of the stocks in these funds' portfolios trade on exchanges outside the United States, and their home exchanges' trading hours may have little or no overlap with U.S. trading hours. During these nonoverlapping hours, there is no real-time price information flowing from their constituent securities' home markets. In these windows, the funds effectively serve as "price discovery" vehicles, with buyers and sellers agreeing on fair values for a basket of stocks or bonds that may not be currently changing hands in their local markets. Thus, these premiums and discounts are part of the normal course of business in those cases where trading of an ETF's shares and trading of its portfolio holdings are out of sync.

Bond ETFs represented seven of the remaining eight ETFs from the 20 that had the largest median premium or discount in the past decade. Premiums and discounts for bond ETFs are typically driven by 1) differences in the way bonds and the ETFs that hold them are priced and 2) costs. For example, at the end of a trading day, a bond ETF will be priced at the midpoint of the prevailing best bid and offer for its shares. However, its NAV will typically be calculated using the bid price for the fund's bonds. The end result is an apparent premium (that is, the ETF shares will be priced higher than NAV). Costs are also a factor. A fund's premium or discount will have to be sufficiently large to give an AP incentive to step in and exploit the arbitrage opportunity--as represented by the transaction cost and compensation for risk threshold in Exhibit 1. These costs, and hence this threshold, are typically far greater in the bond market, which is inherently less liquid than the market for stocks.

Examples of Episodic Premiums and Discounts The episode we've seen in recent weeks is unique as measured by the magnitude of dislocations we've seen--which are without precedent. But there have been previous instances where ETFs' premiums or discounts have flared. No different than what we've seen more recently, these have typically been driven by dislocations in the market for ETFs' constituent securities.

For example, in the darkest days of the 2008-09 market meltdown, premiums for some fixed-income ETFs showed some staying power. During this period, some fixed-income ETFs became a source of liquidity for holders of these funds' underlying securities, who had almost no way to sell individual bonds on the market. For example, based on daily data collected by Morningstar, iShares iBoxx $ Investment Grade Corporate Bond ETF LQD traded at a persistent premium to NAV for the period spanning from Lehman Brothers' bankruptcy in September 2008 through early 2009. During this span, the average daily premium was 2.3%.

On Aug. 24, 2015, many ETFs briefly traded at substantial discounts to their true value. An early-morning sell-off tripped circuit breakers that temporarily suspended trading in a number of stocks and, as a result, many ETFs that held those same stocks. Some investors fell victim to this downdraft, having placed trailing stop-loss orders in these funds' shares that became market orders at precisely the wrong time. Others were able to capitalize on this situation, placing buy orders for baskets of blue-chip stocks at bargain-basement prices. Episodes like these underscore the importance of assessing market conditions prior to trading ETF shares and practicing safe trading.

How Can Investors Monitor and Manage Premiums and Discounts? There is nothing investors can do to directly manage the inevitable premiums and discounts to NAV that exist in the ETF market. Fortunately, these discrepancies tend to be fairly small and fleeting, thanks to the profit-seeking behavior of fiercely competitive market makers, so this should not be a major concern for most long-term investors.

However, when trading ETF shares, it is worth checking whether your buying or selling price is close to its iNAV. Not all brokerages make this information available. You can find ETFs' iNAVs on their quote pages on Morningstar.com. You can also add iNAVs to ETFs' price charts using the "Add Comparison" tool in the charting feature on Morningstar.com by searching for TICKER/IV. For example, you can find the iNAV for AGG by looking up AGG/IV.

While iNAV is a useful touchstone, the prevailing market price is often the best indicator of a fund's going value. At any given time, market makers and other investors place their bid and ask prices on either side of their estimate of an ETF's fair value. If the bid and ask quotes are only a penny or two apart, the midpoint of the two numbers is probably an even better approximation of the NAV at that time. This is because supercompetitive market makers are leveraging their own proprietary pricing models to assess ETFs' fair values at hyperspeed during the course of the trading day in an effort to maintain their "edge" versus their competitors. Also, iNAV isn't as useful for bond funds or portfolios containing international securities, as their prices are likely stale. The SEC recently acknowledged this in its new ETF rule and no longer requires issuers to hire a third party to calculate and disseminate the value on their behalf.

Ultimately, the best way to protect oneself from these dislocations is to avoid trading during these episodes where ETF prices disconnect from their NAV.

But if you must trade, practice safe trading. In all cases, using limit orders is good practice. Limit orders will ensure favorable execution from a price perspective. A buy limit order will fetch the buyer a price less than or equal to the limit price, while a sell limit order will transact at a price greater than or equal to the limit price. What is the potential cost of using limit orders? Time and incomplete execution. That is, it may take longer for a limit order to be filled than a market order, and when that time comes it might not be completely filled. These costs need to be weighed against the cost of being exploited by an opportunistic market maker looking to pick off market orders.

And for those investors who can't or don't care to get comfortable with all the above, there is an expansive menu of index mutual funds to choose from that will guarantee your orders are executed at NAV.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)