How the World’s Largest ETF Changed Financial Markets

5 charts showing SPY’s web of influence.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

As SPDR S&P 500 ETF Trust SPY celebrated its 30th birthday on Jan. 22, 2023, it’s a good time to reflect on the impact it has had as the very first exchange-traded fund listed in the United States. But—record scratch—it wasn’t the world’s first ETF. That title belongs to the TIPs 35 Fund, which planted the ETF flag in the Great White North in 1990.

SPY’s launch also aligned with the growing popularity of index funds. Indeed, during a speech that took place a year before SPY’s inception, Jack Bogle proclaimed that Vanguard 500 Index VFINXwould surpass Fidelity Magellan FMAGX as the world’s largest mutual fund. That prediction came true in 2000, demonstrating that the wheels were already in motion for index funds.

SPY wasn’t a new strategy, but a new way to invest. ETFs provided traders a way to manage market risk within a single instrument that traded intraday on stock exchanges. It plugged the hole between stocks and equity index futures, according to Steven Bloom, one of SPY’s architects. And its start as a trading tool has embedded it in the fabric of financial markets to this day.

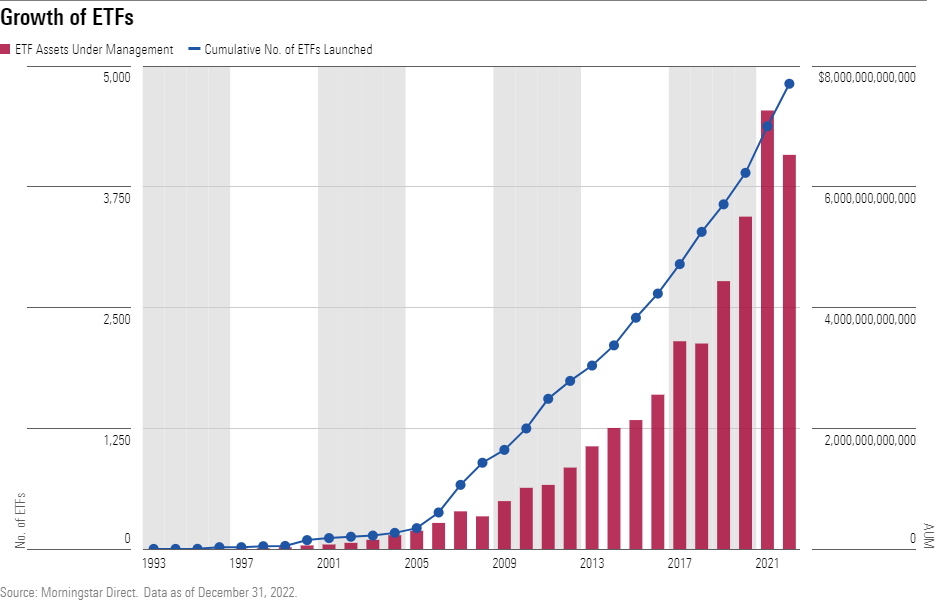

The Spark That Ignited the ETF Market

SPY was the first U.S. ETF, but it certainly wasn’t the last. What started with a single “spider” grew into nearly 5,000 U.S. ETFs and over $6 trillion in assets under management.

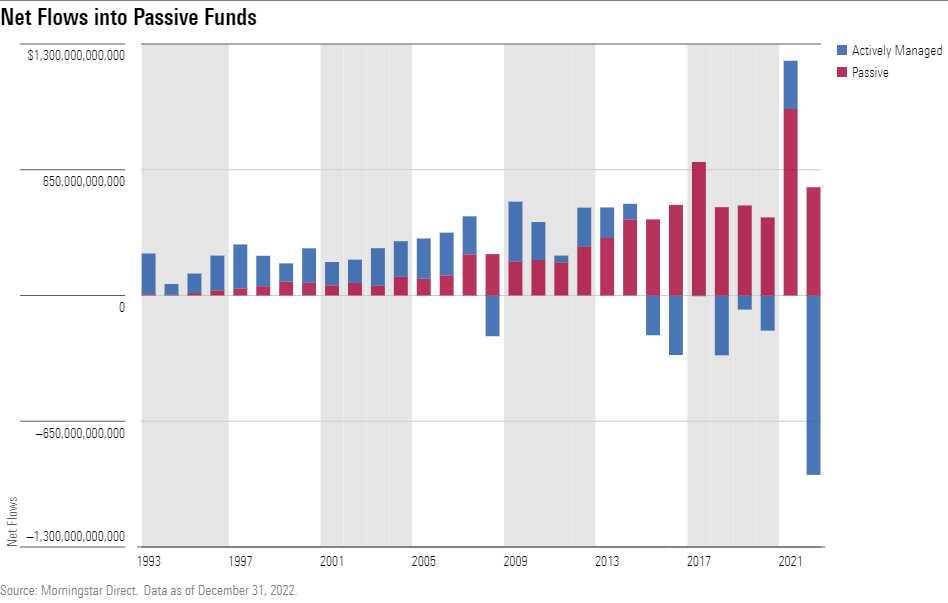

The birth of SPY also precipitated the boom in passive investing. The popularity of index-tracking ETFs hit a fever pitch in 2022, when the spread between passive and active fund net flows hit $1.5 trillion.

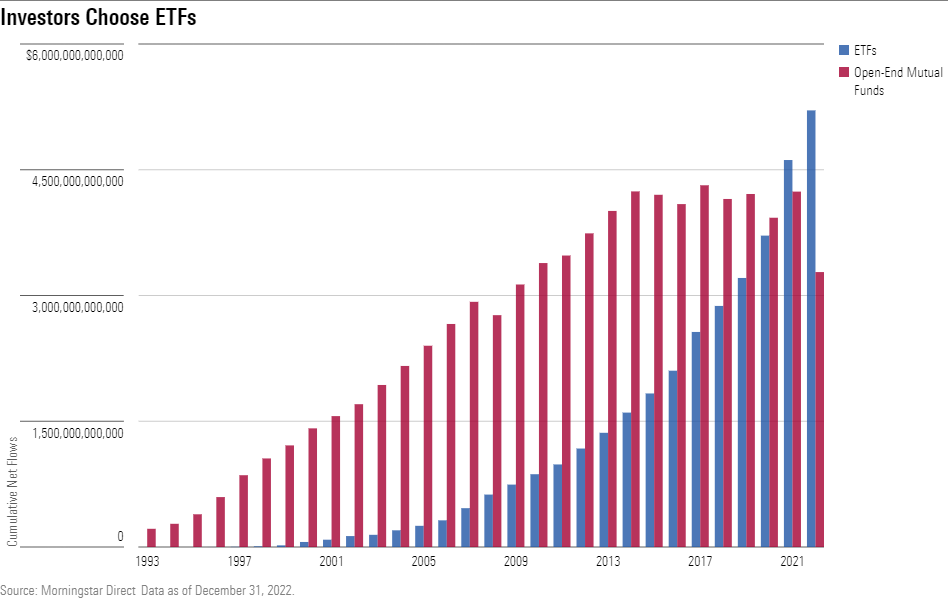

Despite a slow start, cumulative net flows into ETFs since SPY’s launch surpassed mutual funds starting in 2021. That gap widened significantly in favor of ETFs last year.

SPY’s Performance Edge

SPY’s success was critical to investors’ growing acceptance of ETFs. Since its inception, SPY outperformed 71% of U.S. equity funds available in 1993 that had survived, while only 24% of those funds remained open today. SPY jumps up to the top sixth percentile of funds since its inception after accounting for those that died. Its performance went a long way in grabbing investors’ attention and building their trust in ETFs.

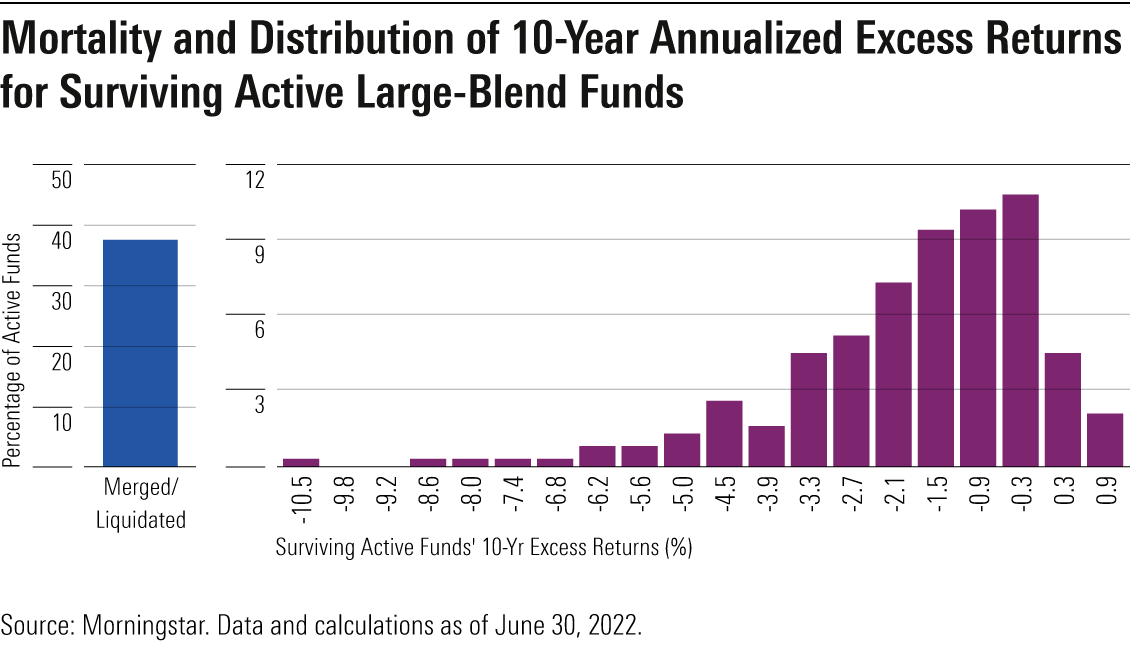

Passive funds like SPY remain a high hurdle for active managers. The 10-year success rates of active funds in the large-blend Morningstar Category over the average passive peer tends to hover around 10%. And some of those active managers failed hard. Over the past 10 years, nearly 40% of active funds alive at the start of the period had to close shop. Of the 60% that survived, many underperformed their average passive counterpart by a significant margin.

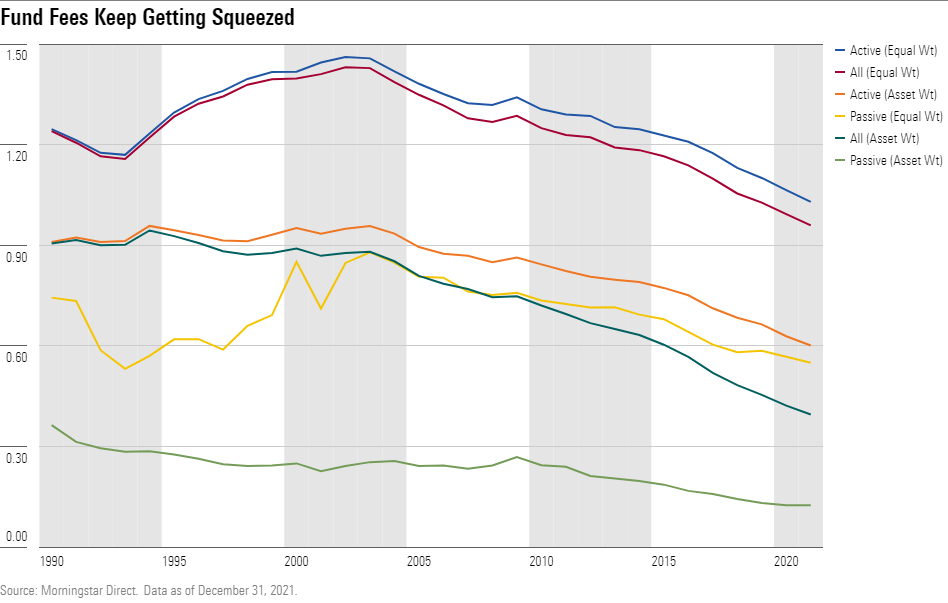

A low fee and low transaction costs played a big part in SPY’s success. The impact of transaction costs is hard to quantify, but market-cap weighting assists the effort. The weight of each stock in SPY’s portfolio fluctuates with price changes, which reduces turnover and the need to trade. Expense ratios more clearly highlight SPY’s advantage. The average U.S. equity fund charged 1.16% annually in 1993, a far cry from SPY’s initial fee of 0.20%. SPY, among other index funds, helped initiate the price wars that continue today.

SPY’s Lasting Legacy

SPY remains the largest ETF, with a staggering $375 billion in net assets, despite cheaper S&P 500 trackers available to investors. SPY alone would register as the fourth-biggest ETF issuer by net assets—a big reason it remains popular with traders. SPY traded over 20 times more shares per day than Vanguard S&P 500 ETF VOO, on average, over the past three months, cementing its prominence in the trader’s tool chest.

SPY also leads ETFs in options volume. And its options aren’t strictly used by traders. Other ETFs use them for option overlays, and they’re even used to price MIAX’s SPIKES Volatility Index, a competitor of the VIX.

SPY’s lead in assets is eroding, as broad market index funds by Vanguard and iShares begin to nip at its heels. But it will remain a major part of financial markets for the foreseeable future.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)