The Advantage for Stocks When Inflation Rises

How stock and bond prices work when inflation is an ongoing possibility.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

This column is inspired by an article published by a reader. (Most seem to have accomplished more than I have.) In “How Inflation Altered the Stock-Bond Relationship,” Lawrence Hamtil writes that, relative to stock prices, bond yields have become higher in recent decades,because of uncertainty about inflation.

The logic is straightforward. Inflation does not affect the payments made by conventional (as opposed to inflation-adjusted) bonds. Whether consumer prices are flat or grow by 10%, a Treasury note with a 4% coupon will pay $40 for every $1,000 of par value. Its distribution never changes. But inflation does influence corporate earnings. Because businesses can raise their prices in response to inflation, at least partially, they offer at least some protection against that danger.

Until the early 1970s, writes Hamtil, this feature went unappreciated because inflation was not a serious concern. Prices briefly surged after World War II, and then again during the Korean War, but investors correctly viewed those spikes as temporary. When supply caught up with demand, inflation subsided. However, after President Nixon cut the nation’s final ties with the gold standard by suspending the Bretton Woods system in 1971, the genie was released. High inflation became an ongoing possibility, thereby reducing bonds’ attractiveness.

Hamtil concludes by noting that equities need not be perfect inflation hedges to outdo bonds. They merely need to do something. True that. Which leads to the next issue: To what extent have companies been able to overcome inflation?

The 67% Rule

The question cannot be precisely answered because the sample size is small and the results vary. For example, when inflation skyrocketed from 1946 through 1948, so did real corporate earnings. But when inflation was equally high in the early 1980s, the opposite occurred. Adding to the difficulty of connecting inflation’s causes and effects is that higher prices sometimes immediately hurt real corporate earnings, while at other times their consequences arrive later.

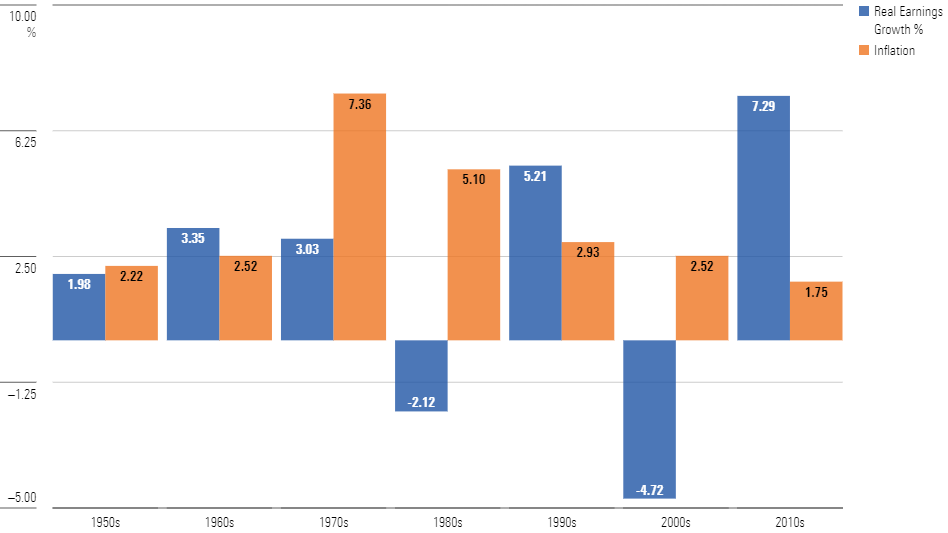

Those caveats being noted, the following chart provides a reasonably accurate picture of the relationship between real corporate earnings and inflation. It shows the average annualized rate of 1) real earnings growth and 2) inflation for companies in the S&P 500, over each decade from the 1950s through the 2010s.

Real Earnings Growth and Inflation, by Decade

The very lowest decade for inflation, the 2010s, also registered the strongest real earnings growth. As that evidence suggests, companies can benefit from predictably low inflation rates. However, inflation was almost as tame during both the 1950s and early 2000s, in the first case with average corporate-earnings growth and in the second with poor results, thanks to the double-whammy of the technology-stock meltdown and the global financial crisis.

Meanwhile, despite its rotten reputation, the “stagflation” decade of the 1970s wasn’t all that bad for corporate earnings. At 3%, annual after-inflation earnings growth placed fourth among the seven decades. That picture is somewhat deceptive, as it omits the earnings decline during the early 1980s, but the lesson remains. Corporations do indeed compensate for the damage of inflation by increasing the prices they charge their clients.

In short, companies can mostly overcome inflation’s tax, but not entirely. As a rough estimate, they can neutralize two thirds of inflation’s cost. The other third represents an opportunity cost, levied by macroeconomic disorder.

For Example

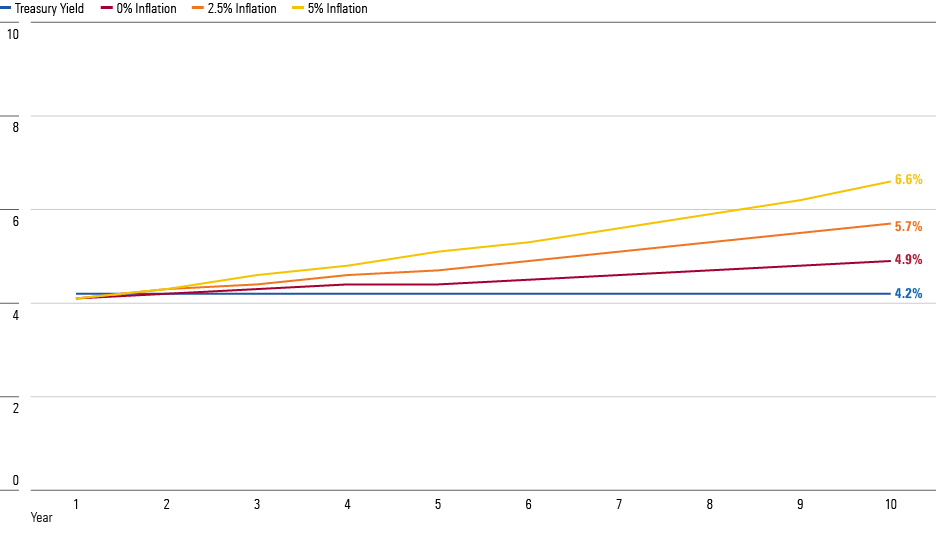

Let’s now consider how the differing levels of inflation insurance for stocks and bonds—partial for the former and none for the latter—affect their future payouts. The next chart measures how 1) the earnings yields (defined as earnings divided by price) for stocks and 2) the yields on bonds can be expected to behave over time, assuming typical economic conditions.

Specifically, the study assumes 2% annual real corporate earnings growth while modeling three levels of inflation: 1) none, 2) 2.5%, and 3) 5%. When inflation is dormant, the annual growth in equity earnings yield equals the real amount of 2%, while bond yields remain unchanged. However, when inflation exists, the nominal equity earnings yield receives a multiplicative bonus of (by this column’s estimate) two thirds of the inflation rate. The net effect is that nominal earnings on stocks increase by 3.7% per year in the second scenario and by 5.4% in the third.

The year 1 figures represent current financial market prices: an earnings yield of 4.1% for the S&P 500 and (as of this past Friday) a 10-year Treasury note yield of 4.2%. The illustration then depicts how those yields would change over the next 10 years, using the above assumptions.

Earnings Yields Versus 10-Year Treasury Payouts

Note how much more attractive equities become, relative to bonds, as inflation rises. When inflation is absent, the equity earnings yield only gradually surpasses the 10-year Treasury yield, reaching 4.9% when the decade ends, as opposed to the bond’s steady 4.2% payout. But when inflation surfaces, the equity earnings yield increases to 5.7% for the medium-inflation case. If inflation is high, the final earnings yield is a generous 6.6%.

True, rising inflation can harm stock prices by reducing the multiple that investors will pay for a given amount of earnings. That occurred during the 1970s and early 1980s, as declining price/earnings ratios lowered stock returns. During that time, however, long bonds performed even worse.

Conclusion

This article’s numbers are merely illustrative. The 67% estimate for equities’ level of inflation protection was derived—roughly—by summarizing several decades’ worth of evidence. In any single period, the percentage of inflation that corporations can absorb without suffering a decline in real earnings will vary. However, the model does demonstrate how the underlying math works. Bond investors must wish fervently against the resumption of inflation. Equity shareholders need also care—but nowhere near so deeply.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)