Most college costs are covered by loans, while only 13.5% are covered by savings, according to research by student loan provider Sallie Mae. So the challenge for many parents is simple: finding a way to borrow less and still pay for college.

A recently released Morningstar report, “ New Lessons About 529s,” addresses this challenge. In our research, we examine the untapped power of 529s by measuring what would happen if real American households placed their college savings exclusively in a 529.

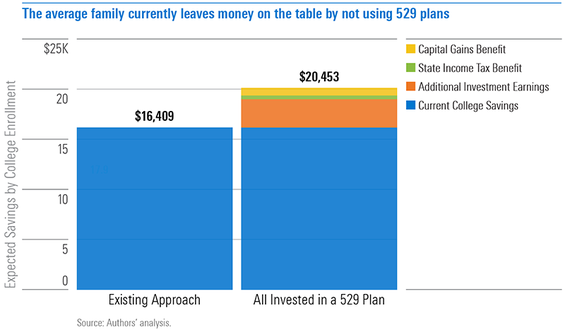

How much are 529 plan benefits worth?

In our analysis, we started with a nationally representative sample of American households with children under age 18 from the Survey of Consumer Finances. We combined it with data from Sallie Mae’s How America Saves for College (2018) report, to estimate how much each household in the survey has saved for college and in what vehicles—i.e. 529 plans, investment accounts, or checking and savings accounts.

Then, for each household, we considered an alternative scenario that examines what their college fund would look like if, at the birth of each child, the family had put all college savings into a 529 plan. This allowed us to calculate the potential impact on each families’ finances.

The answer: billions

We estimated that, by the time their children are ready for college, American households would collectively have saved $237 billion more in assets if they used 529 plans. For the average family saving for college, this means $4,044 more per child without saving an additional penny. To consider this potential boon from another angle, families could save 25% less and still have the same amount available when their child is ready for college if they exclusively used 529s.

What drives this effect? It’s not the tax incentives that 529s are known for. Many families put their college savings in savings and checking accounts—and do not invest it. Since 529s are primarily investment vehicles, they can help families earn a much higher return on their savings over time. The tax advantages of 529s do help, but they have a smaller impact—as the following chart shows.

The benefit of investing is not unique to 529 accounts—any investment vehicle would provide it. The tax incentives, although smaller, do matter and account for about one third of the total benefit, with a particular boost coming from the capital gains incentive.

There is a caveat here—not every family benefits equally. Certain families benefit more than others from 529 plans, and we’ll dive deeper to explain why in our next blog post.

Maximizing 529 plan benefits

Our analysis looked at the aggregate benefits of adopting a 529 plan, but each family is different. The right choice for any particular family depends on their specific circumstances and preferences. Each family needs to decide whether the added risk and volatility (because of increased market exposure), hassle (to set up and fund the account), and constraints (arising from the more limited set of investment options in 529s compared with other investment vehicles) is worth the gains provided by these accounts.

We’ll discuss these family-level dynamics more in upcoming posts and how advisors can help families navigate these choices. But at aggregate level, the potential benefit is clear and significant: an estimated $237 billion in assets. It behooves families, and their advisors, to evaluate the multitude of 529 plans available and determine which 529 option, if any, is right for them.