Keeping What You Earn

The painful math of taxable accounts.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

This article was originally published in February 2014.

The Big Picture The paper's title caught me by surprise. "The 50% Rule: Keep More Profit in Your Wallet," by Stuart Lucas, chairman of the financial advisory firm Wealth Strategist Partners, advocates that investors retain at least half the profits generated in their taxable accounts, thereby giving less than half to government bodies and investment professionals. At first thought, the goal seemed very unambitious. With mutual fund expense ratios less than 1% for most large funds, investors surely need not leak anything like 50% of their profits.

It made sense on second thought. Percentage of investor profits, after all, is quite different from percentage of assets. A 1% annual expense ratio is a tiny fraction of overall assets, but in a year when market returns are 5%, that same expense ratio gobbles up 20% of gross profits. Also, Lucas incorporates tax effects. As he points out, performance is typically reported on a pretax basis. Pretax figures appear on fund advertisements, are shown in Morningstar performance tables, and are incorporated into the Morningstar Rating for funds.

Taxes, of course, are not ignored by those who have the job of collecting them--and they are far from a minor effect in a taxable account, for investors in a high tax bracket. Indeed, for short-term capital gains and income, an investor in a high-tax state can surpass the 50% barrier on taxes alone.

Unsurprisingly, Lucas touches only lightly on financial-advisory fees. They of course must also be added to the equation. As with fund expenses, the seemingly modest 1% of assets that are paid on a typical fee-based advisory account make up a much larger percentage of investor profits.

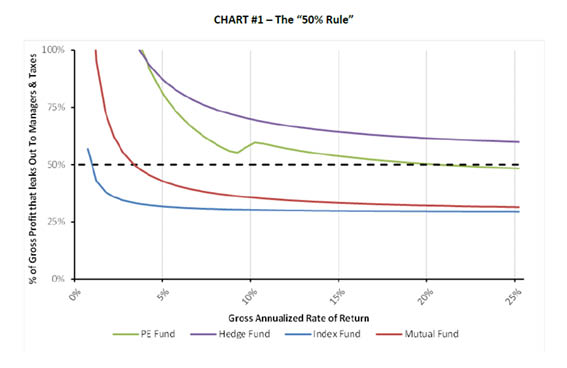

How this all plays out can be seen in the graph below, taken from Lucas' article. I've chopped the lengthy footnotes, which give the various assumptions that go into the numbers. The picture's power lies in its two simple tales. One is that as gross returns decline, leakage as a percentage of profits rises. The other is that while index mutual funds retain more profits than actively managed funds, even actively run funds look good when compared with hedge funds and private equity funds. With those funds, it's very difficult to retain that seemingly low amount of 50%.

Source: Wealth Strategist Partners

Learning Points One lesson, certainly, is to evaluate investments for taxable accounts--prospective and existing--on an aftertax basis. It's all very well for Fund A to have a higher pretax total return, or Sharpe ratio, or Morningstar star rating than Fund B, but if B is the superior fund after taxes are paid then it is the superior fund for the taxable account.

(Lucas suggested in a conversation with me that Morningstar publish aftertax star ratings in addition to the current version. I don't think Morningstar would want two versions of the star rating floating around, but I certainly can see the need for tools that enable investors to make both total-return and risk/return comparisons between funds on an aftertax basis. The ability to incorporate other costs, for example, financial-advisory fees, would be helpful as well.)

Another lesson is the unattractiveness of alternative investments. That alternative strategies carry high expense ratios, often exceeding 2% annually, in the mutual fund format, and even higher costs when packaged as hedge funds and accompanied with a performance fee, is well known. Lucas reminds us, though, of two additional issues. First, many alternative funds trade frequently and generate inefficient short-term capital gains. (Some also use fixed-income strategies that create taxable income.) Second, as alternative funds generally have modest pretax returns, being structured as portfolio diversifiers rather for achieving high total returns, their costs are even higher when measured as a percentage of profits.

Yet the growth in alternatives funds has largely been in the taxable accounts of wealthy investors. There are few alternative funds in 401(k) plans. (Alternative strategies are often incorporated into target-date funds but not made available on their own.) Alternatives are also usually not bought by smaller, direct investors. They are sold by financial advisors to relatively wealthy clients, many of whom have tapped out their tax-sheltered accounts.

Lucas mentions why: The low recent yields of municipal bonds have been hard to tolerate. As a result, he has seen investors replace muni bonds with "hedge funds, 'absolute return funds' and riskier higher yielding fixed income investments." It feels good to move out of low-paying munis, and it may look good on a pretax basis, but, as Lucas writes, it is unlikely to be a good move after all is said and done.

Consider, for example, Vanguard Long-Term Tax-Exempt VWLTX and the Institutional shares of Calamos Market Neutral Income CMNIX. Five years ago, one might have been tempted to swap the former for the latter. That would have been a sound move. The Calamos fund made 7.81% on a gross basis over the next five years (through Jan. 31, 2013), 6.94% pretax after paying its 0.87% expense ratio (the 6.94% figure being the one reported for standard performance charts, including on Morningstar's pages), and 6.17% after accounting for federal taxes at the highest rate. Vanguard's fund, in contrast, made a much lower 5.96% as a gross profit, 5.76% after paying its 0.20% expense ratio, and also 5.76% after taxes.

The Calamos fund outgained the Vanguard fund on every measure. However, the initial Calamos advantage of 180 basis points per year was whittled away to 40 basis points after costs and taxes were considered. Also, the Calamos fund was the single best-performing market-neutral fund over that time period--as well among the very cheapest. Thus, after conducting great research and making a terrific selection, the Calamos investor barely outlegged the easy choice of the Vanguard fund.

It could have been much, much worse--and would have been for investors who lacked the power of perfect foresight. The A shares of DWS Diversified Market Neutral, for example, gained 2.47% per year before expenses, which became 0.70% after paying a 1.77% annual expense ratio. A whopping tax bill shaved another 182 basis points per year from that figure, giving the fund a net aftertax total return of negative 1.12% per year. The fund company got 1.8 percentage points per year, the government got 1.8 percentage points per year, and the investor got ... poorer. This was not an isolated example; the DWS fund had only moderately lower returns than the category average and a typical expense ratio.

Lucas' paper does a nice job of reminding readers to control the simple but powerful items. Get the big things right.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)