How Much of Your ETF's Dividend Income Is Qualified?

Pick dividend ETFs that offer a high percentage of qualified dividend income to maximize aftertax investment performance.

/s3.amazonaws.com/arc-authors/morningstar/64dafa24-41b3-4a5e-aade-5d471358063f.jpg)

A version of this article was published in the March 2018 issue of Morningstar ETFInvestor.

Vanguard founder Jack Bogle has succinctly summarized the effect of fund fees: "In investing, you get what you don't pay for." The less you pay to an investment manager, the more you keep for yourself. The same goes for taxes. The less you fork over to Uncle Sam, the more you pocket. Fortunately, investors have a good amount of control over these two important factors. In this article, I'll zero in on an often overlooked source of tax costs and examine the topic of qualified dividend income, or QDI.

Many investors turn to dividend-paying stock funds for investment income. The Jobs and Growth Tax Relief Reconciliation Act of 2003 made dividend payments more attractive because it introduced a lower tax rate for qualified dividend payments.

Qualified dividends are currently taxed at a rate of 0% to 20%, depending on an investor's tax bracket, rather than at the same rate as ordinary income tax rates. Thus, the higher the percentage of a fund's dividends classified as QDI, the more money taxable investors take home after taxes.

QD 'Aye' Ordinary dividend income is considered "qualified" if it meets certain criteria:

1) A U.S. corporation or qualified foreign corporation makes the dividend payment.

2) The fund (or individual investor) holds the security for at least 61 days out of the 121-day period that began 60 days before the security's ex-dividend date. For example, if a stock's ex-dividend date is March 1, 2018, the investor must hold the shares for more than 60 days between Dec. 31, 2017, and April 30, 2018, for the dividend payment to be eligible for the preferential tax treatment.

3) Special structures such as real estate investment trusts and master limited partnerships do not qualify for favorable dividend income treatment.

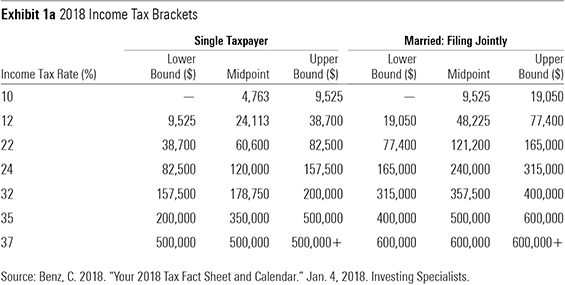

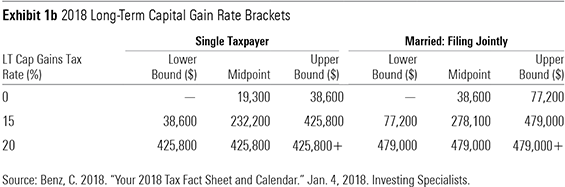

Exhibits 1a and 1b display the new 2018 income tax and long-term capital gains tax brackets.

It's worth pointing out that the income breakpoints between both tables do not line up cleanly as they had prior to the 2018 tax reform. But the implication is straightforward. The bigger the differential between investors' income tax rate and long-term capital gains tax rate, the more they stand to gain by increasing the portion of qualified dividend income.

What's the Impact? Let's assume an investor's annual income is $400,000. This income level translates to a 2018 income tax rate of 35% and a 2018 long-term capital gains tax rate of 15%. Because I can't predict the future of tax policy, I'll hold these tax rates constant. Let's say the investor parked $100,000 in a dividend-paying fund that paid a constant dividend yield of 4% each year. We'll ignore capital appreciation and reinvest the aftertax dividend payment back into the fund at the end of each year to isolate the effect of QDI.

If none of the 4% dividend payment is qualified, then the dividend payment is taxed at the investor’s income tax rate of 35%. At the end of year one, our hypothetical investor only keeps $2,600 of the $4,000 pretax dividend payment. But if the entire dividend payment is deemed qualified dividend income, then it is taxed at the investor's long-term capital gains tax rate of 15%. The investor keeps $3,400 of the $4,000 pretax dividend payment. The power of compounding illustrates the impact of the favorable tax treatment of QDI on an investor's wealth across 10 years. At the end of year 10, the investor will have $129,263 if none of the dividends is qualified, or $138,267 if 100% of the dividends are qualified. That's about a 7% difference in ending wealth.

What's My QDI? Investors in the same fund may have different percentages of qualified dividend income depending on when they purchased or sold it. Investors can use their 1099-DIV tax form to determine their individual portion of QDI. In the 1099-DIV tax form, Box 1a lists total ordinary dividends, and Box 1b shows the amount of the dividends in 1a that count as qualified.

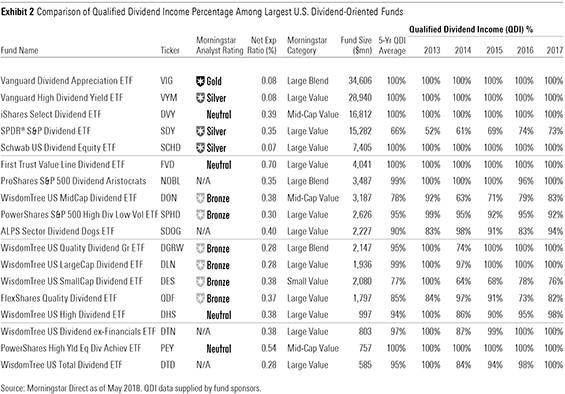

Nearly all major fund sponsors post funds' tax information on their websites. These pages usually include the most recent year's QDI percentages for each of their funds and other tax information such as estimated and actual capital gains distributions. Note that these QDI figures may not match individuals' actual QDI because they assume the maximum QDI treatment and aren't based on individual investors' holding periods. Exhibit 2 shows the five-year qualified dividend income percentages from 2013 through 2017 and the QDI percentage for each of these years for the largest U.S. equity dividend-oriented funds. All QDI figures are expressed as a percentage of total dividends paid for each calendar year.

During the five years through 2017, most of the largest dividend-oriented funds kept their average QDI figure high. Four of the funds in Exhibit 2 have lower average QDI figures. There are a handful of reasons driving this:

1) High allocations to REITs. REIT dividends are not eligible for QDI treatment, but it's not so straightforward: Portions of many REITs' dividends are classified as nontaxable returns of capital that reduce the cost basis of the security.

2) Securities lending. Some funds lend out their holdings to third-party borrowers to generate income. The dividends that the fund receives from the borrower are not eligible to be treated as qualified dividends.

3) High turnover. Funds that reconstitute frequently may not meet the minimum holding period requirement for a stock's dividend payment to be QDI-eligible.

What to Do? Maximizing aftertax returns helps investors compound their wealth. But investing in funds that track soundly constructed indexes and charge low fees will have more of an impact on investors' overall wealth than searching out funds that maximize QDI percentages--which will do far less to move the needle. For most long-term investors, the capital gains hit from swapping similar funds will more than wipe out any future fee or tax savings. That said, considering this particular aspect of funds' tax efficiency when selecting new funds will help maximize the power of compounding over the long haul.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click

for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets,

or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/64dafa24-41b3-4a5e-aade-5d471358063f.jpg)