Buy the Best, Perform the Worst

And vice versa.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Right Idea, Wrong Time Earlier this week, for an upcoming feature on investor returns in Morningstar Magazine, I participated in a discussion with Morningstar's Russ Kinnel and Rayliant Global Advisors' Jason Hsu. The latter presented a counter-intuitive argument: When buying value funds, investors should seek funds with bad recent performance.

Hsu is correct, but the idea takes some unpacking.

To start, let's review investor returns. That calculation differs from the customary measure of mutual fund performance, total returns, in that it also considers the size of the fund's assets. If a fund is tiny when it gains 10% in net asset value, and large when it loses 5%, then it will have a positive total return but a negative investor return. The portfolio manager might have done well, but the shareholders of the fund did not, because they mistimed their investments.

Unfortunately, that example pretty accurately describes how mutual funds are used. As Russ has repeatedly shown in his "Mind the Gap" series, across the large majority of fund categories, over almost all time periods, the average investor return lags the average total return. This return gap, as it is termed, comes from badly timed purchases and sales. A positive return gap suggests that investors were collectively savvy, getting into funds before the good times and getting out before the bad. A negative return gap … not so much.

Value fund shareholders have been no exception. Hsu finds that, after paying their expenses, value-style mutual funds outgained the S&P 500 by an average of 39 basis points (0.39%) per year from January 1991 through June 2013. However, value fund buyers botch their purchase and sale decisions, leading to a return gap of 131 basis points. The math then becomes 32 for the funds and negative 131 for investor decisions, leading to a net loss of 92 basis points. The investor returns (or dollar-weighted returns, if you like) for value funds trails the S&P 500 by almost 1 percentage point per year.

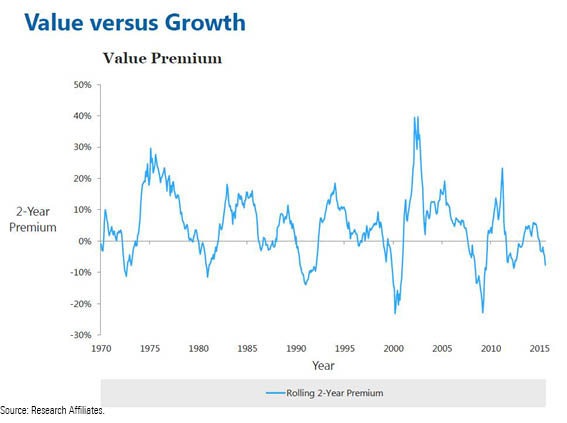

The Style Wave Hsu points out that while value stocks beat the overall stock market over long time periods, they often trail over the intermediate term. And there's something of a rhythm to that behavior. Typically, value climbs for two or three years and then declines for about that amount of time. The decline is generally not as large as the rise, which is why value wins the overall war.

The chart below shows the value-stock premium (that is, the difference in returns between value and growth stocks) calculated over rolling 24-month periods. Up, down, up, down. The pattern isn't so regular as to be predictable, but it doesn't seem to be entirely random, either.

Hsu postulates that the sequence is indeed not fully random, thanks to decisions made by the market's participants. When value stocks rise, the funds that own them lead the performance charts. Investors notice, and they begin to buy these apparently well-managed funds. When those new assets are put to work, they further inflate the prices of value stocks. The funds increase their gains. More assets follow.

The virtuous cycle continues until, at some point, value stocks become so obviously overpriced that portfolio managers who have the flexibility to hold different types of stocks shun value. They put their value stocks up for sale, thereby blunting the buying pressure that has favored the value style and ultimately reversing the trend. Value begins to trail growth, and does so until it becomes so attractively priced--such a value!--that the flexible managers return.

(The economic cycle also has an effect on the value/growth premium. Because value stocks tend to be from economically sensitive companies, value typically struggles when the economy weakens. In some sense, Hsu believes, those problems are what create the value premium in the first place … but that notion is for another column.)

Winning With Losers Do you see where Hsu has taken this?

- Most money comes into value funds after value has performed well.

- At such a time, the value funds with the strongest recent returns will be the purest of the value funds--those that follow a so-called "deep value" strategy. When value reverses course, these funds will trail their peers.

- Therefore, investors should buy the laggards, not the leaders. The funds that have fallen behind will hold up better during the sell-off.

To which you might respond, "Well yes, but I'm no dummy. I won't buy value funds after the value style has rallied. I will buy value funds after value has declined, when it's near a bottom."

(If so, you are a distinct exception. Many people call themselves contrarian, but few actually are. Across investor segments, from pension funds to hedge fund owners to mutual fund shareholders, there is a clear and incontrovertible pattern of buying high and selling low. For example, each of those groups decided to increase their allocation to alternative investments after the 2008 stock crash--and then found itself lighter in equities when stocks staged one of the greatest rallies of the century.)

Fine--but the advice remains intact. When value stocks bottom, the value funds that have dropped the furthest will be the purest and deepest of the value fund. They will shine during the rally. Once again, the sensible plan is to shun the best, and buy the worst.

Hsu gives such counsel specifically for value investing, because that was the focus of his research. But his precept applies to any mutual fund category that shows a similar relative-performance pattern. It obviously would hold for growth-style funds, which are, after all, the mirror image of value funds. As for other fund types, that would depend on the numbers. Do the category's relative returns oscillate in a somewhat reliable fashion over the intermediate term? If so, then the best fund choices will lie with the worst.

Such advice requires a common-sense caveat: Recent bad performance might be a positive sign for a mutual fund, but a poor showing over a full market cycle is anything but. The ideal buy candidate, per this doctrine, is a fund that boasted excellent 10-year numbers a couple of years ago but has since trailed its peers during a weak stretch for its investment style. Naturally, that fund should also have a relatively low expense ratio--why pay full price when so many good discount options are available?

From worst to first. Or, more commonly, for investors who get it wrong and who thereby create the return gap, from first to worst.

Addendum: One hour and 25 minutes after I finished writing this column, I received an email from Bill Bernstein in which he regrets that Morningstar star ratings have a three-year time horizon (which they do, in part) because asset classes revert over such a period. Therefore, writes Bill, the star rating (or any other three-year performance measure, as the argument is general and is not specific to the star-rating calculation) will favor the purest versions of the funds in the "hottest asset classes" before those asset classes reverse.

That's right--his email is the content of this column, in shortened form. A clever fellow, that Bernstein. Knows a bit about investments, and reads minds from 2,000 miles.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}