Are U.S. Stocks Overripe?

The evidence from three indicators.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

A Cautionary Note Market-timers are circus clowns minus the funny suits. Even when they dodge the bear market, they inevitably miss the ensuing bull. Their track record is terrible, and that of their cousins, tactical asset allocators, is not much better. There is a reason 99.9% of mutual fund assets are invested in funds that don't attempt to time the market.

The same, naturally, applies to market-timing writers. As I would prefer not to don a red nose, this column is therefore offered as an exercise, rather than as advice. Do stocks appear to be cheap, expensive, or somewhere in between? The answer is unlikely to change our investment portfolios (it certainly won't change mine), but perhaps the process of thinking through the issue will prove useful. Bad news strikes less hard when it has been anticipated.

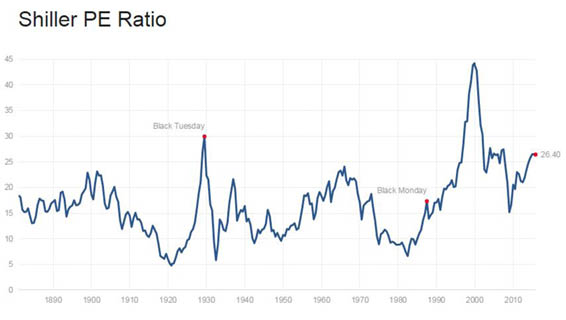

Shiller P/E Ratio Familiar to veteran readers of this column, the market's Shiller P/E ratio, derived from the average inflation-adjusted earnings that companies generated over the past decade (as opposed to typically cited stock-market P/E ratios, which are calculated either on last year's earnings or on next year's forecast), appears to be shrieking, "Sell!"

- Source: multipl.com

Today's Shiller P/E ratio is significantly above the ratio when the market opened on Oct. 19, 1987 (Black Monday). True, the Shiller ratio is below the levels it registered on Oct. 29, 1929 (Black Tuesday), and of the start of this century, but as the former was followed by the longest bear market in U.S. history and the latter by three consecutive years of stock declines, such news offers scant comfort. By any measure, the number looks to be perilously high.

But looks can be deceiving. There are two problems with drawing the apparently obvious lesson from the Shiller P/E ratio chart.

One, historically, the ratio has been a wobbly indicator. I realize that statement sounds ridiculous, given both the picture and my comments above about market peaks coinciding with high Shiller P/E ratios. But those items enjoy the benefit of full hindsight. At the time that the signal was flashing, only the data to the left of that date were available. And that information would have suggested danger in the mid-1950s, no great concern before Black Monday, a red light in the early 1990s, and a lukewarm buy signal (at best) at the market's trough in 2009.

The other problem with drawing the obvious lesson is that today's P/E ratios are not your father's P/E ratios. Accounting standards change. Whether the Shiller P/E chart is fatally compromised by mutations of generally accepted accounting principles or merely challenged is outside the scope of this column, but without question the changes to accounting methods hamper the chart's usefulness. (I discussed this issue in greater detail two years ago.)

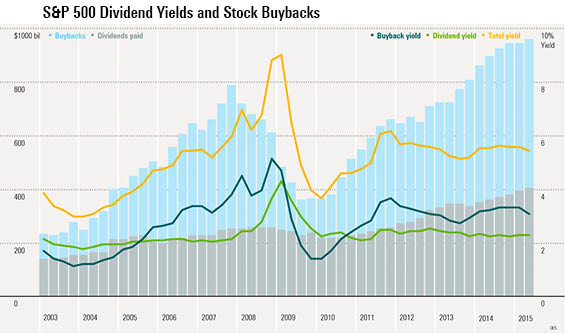

Dividend Yields (and Buybacks) The remaining two charts present few problems for comparability, albeit at the considerable cost of historic context, as they begin in 2003. Unlike with the Shiller P/E ratio, which is calculated by outside parties, these data come from Morningstar, courtesy of the quarterly Markets Observer publication.

One chart is an enhanced version of a dividend yield chart. The yield on the stock market is a fine starting point for making back-of-the-envelope market projections, with lower dividend yields suggesting lower future market returns. But it has a drawback in that it neglects stock buybacks. After all, as with dividend payouts, stock buybacks are monies that are spent to benefit existing shareholders. Assuming that the stock buybacks are funded from existing monies rather than by borrowing, they come from the same pool of excess cash.

The Current Picture

- Source: Morningstar Markets Observer

The bars represent the total dollars spent by S&P 500 companies on payouts and buybacks over trailing 12-month periods--just under $1 trillion at last count. The lines are the more relevant figure for our purposes, as they divide the dollar amount by the (unshown) S&P 500 market capitalization, to arrive at a dividend-plus-buyback percentage that the Markets Observer team calls Total Yield.

That figure is now slightly below 6%. Broadly speaking, it's been roughly at that level for a decade, with the exception of a runup before the 2008 crash, as companies increased their stock buybacks, and then a quick postcrash slide as companies reversed course and cut their buybacks.

In other words, chief financial officers--not retail mutual fund investors--have been the suckers at the table. Which leads to a problem in interpreting the Total Yield indicator. If CFOs were decent investors, then a high total-yield percentage would suggest that companies have a great deal of excess cash relative to their market valuations and thus that stock prices are fairly low. But if CFOs are chumps who have terrible market-timing, then the opposite is true--a high Total Yield percentage is a bad omen, not a good one.

Either way, today's signal looks benign. Of course, this signal has no formal predictive value; effectively, with only one major market crash occurring during the chart's 12-year history, its sample size is exactly 1!

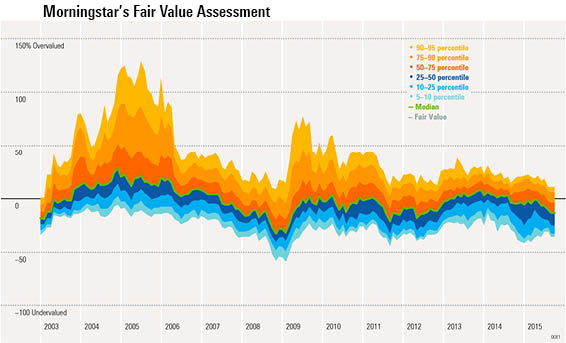

Morningstar's Fair Value Measure The third indicator differs from the first two by incorporating human judgment and by considering many more data points. It is the verdict rendered by Morningstar's equity analysts, who price the stock of each company they cover by conducting discounted cash flow analyses. This is much more ambitious than the simple backward look of the Shiller P/E ratio or the trailing 12-month numbers used in Total Yield.

The analysts' assessment of the stocks' fair values can then be compared with the market prices, with the aggregated totals indicating the degree to which Morningstar's equity analysts, through their bottom-up research, agree with the current stock market prices.

- Source: Morningstar Markets Observer

The bright colors represent the stocks regarded by Morningstar's analysts as being overvalued, the blue shades as being undervalued, and the green line as the median. As with the Total Yield indicator, the median fair value signal has hovered in the same general range for several years. That would again indicate some level of comfort--or at least diminish the possibility that a major crash is just around the corner.

On the other hand, it's worth noting that Morningstar's equity analysts did not, in aggregate, call the 2008 market crash. As stock prices began to slide in late 2007, the analysts did not adjust their earnings forecasts downward, which led to the market becoming cheaper (and thus more attractive) by the fair value measure as autumn 2008 approached. Objectively, given the huge gains posted by stocks since 2009, their fair values might well have been right--but they sure didn't feel right at the time.

To its credit, the fair value indicator registered its all-time low (all-time, that is, for its limited history) at the very best time to purchase stocks: late 2008 through early 2009. That lends a bit of reliability to the indicator's predictive value, which, to cite the broken record, cannot be demonstrated statistically.

A final note on the fair value chart: As shown by the narrowness of the current percentile lines, Morningstar's analysts find today's stock market to be as consistently priced as any that they have encountered. In their collective view, there are few obvious bargains, and equally few stocks that are overpriced. That represents a challenge for active fund managers who believe that they will demonstrate their worth in the next bear market. Per Morningstar's analysts, the current market offers neither good hiding places nor obvious spots to avoid.

Conclusion To the extent that any tentative conclusion can be drawn from this discussion, I believe it is this:

- Each indicator is, roughly speaking, in a holding pattern.

- Absolutely, stocks can crater when valuation indicators are static.

- But such crashes are generally kicked off by dire economic news, as in 2008.

There are times when stock prices are so high that even modest concerns can shake them, such as the 1987 and 2000-02 sell-offs. I don't believe that today is one of those times.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)