Sizing Up a Distinctive Approach to Tilting Toward Smaller-Cap Stocks

This exchange-traded fund tilts toward smaller and more-defensive names in the large-cap universe.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

In a crowded field, iShares MSCI USA Size Factor ETF SIZE offers a distinctive way to tilt toward smaller-cap stocks. It has almost no exposure to small-cap stocks. Instead, it tracks the MSCI USA Risk Weighted Index, which includes the same large- and mid-cap stocks as the broad MSCI USA Index. The risk-weighted benchmark reweights these stocks according to the inverse of their volatilities over the past three years, with a cap to improve diversification. This gives the least volatile stocks the largest weightings and skews the portfolio toward the smaller names in the MSCI USA Index.

The average market capitalization of the fund's holdings is only a third of the corresponding figure for the MSCI USA Index's, so its name is not a complete misnomer. That said, the fund's risk-weighting approach is a more important distinguishing characteristic than its market-cap orientation. It offers moderately defensive exposure to stocks at the smaller end of the large-cap spectrum for a reasonable 0.15% annual fee.

There are more-defensive alternatives, such as

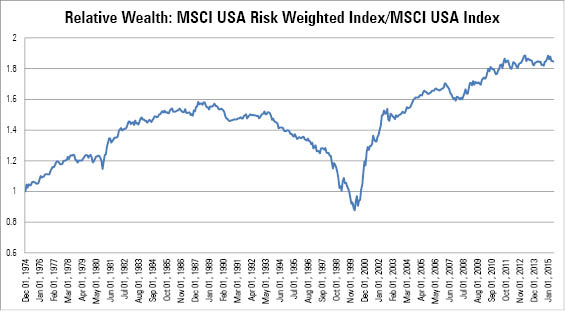

From its back-tested inception at the end of December 1974 through June 2015, the MSCI USA Risk Weighted Index was a little less sensitive to market fluctuations than the MSCI USA Index and was slightly less volatile. This is because the risk-weighted index overweights stocks that have exhibited low volatility relative to the market in the recent past, and this characteristic tends to persist in the short term. During the sample period, the risk-weighted index also outpaced the MSCI USA Index by 1.7 percentage points annually. This outperformance is largely attributable to the index's historical tilt toward stocks with low valuations and high profitability.

The relative wealth chart below illustrates the timing and magnitude of the risk-weighted index's outperformance. It plots the growth of a dollar invested in the MSCI USA Risk Weighted Index, divided by the growth of a dollar in the MSCI USA Index. When the line is upward sloping, the risk-weighted index is outperforming. The opposite is true when it is downward sloping. As the chart shows, the fund's index had a good run from its inception in 1974 through September 1988. It subsequently underperformed through most of the 1990s and surged ahead in bear market during the early 2000s, like most value strategies. It also held up a little better during the bear market from October 2007 through March 2009 and continued to outperform since.

Source: Morningstar.

The fund does not currently have a significant value tilt, which could reduce its potential long-term return advantage. At the end of June, it was trading at a similar multiple of forward earnings (19.0) to the MSCI USA Index (18.6), though it looked slightly cheaper on book value. At first glance, the portfolio does not appear to have a profitability tilt, either. On average, its holdings generated slightly lower returns on invested capital (ROIC) over the trailing 12 months through June 2015 than the constituents of the MSCI USA Index. This isn't surprising because there is a strong positive relationship between profitability and market capitalization. However, the fund's holdings look a little more profitable, based on ROIC, relative to the MSCI USA Equal Weighted Index, which has a similar average market capitalization. This size-relative profitability tilt may continue to give the fund an edge during market downturns.

The portfolio's largest holdings include defensive names, such as

Alternatives

More-cautious investors might consider Bronze-rated

Those who prefer to stick with U.S. stocks might also look at iShares MSCI USA Minimum Volatility USMV (0.15% expense ratio). It follows a similar optimization approach to Vanguard Global Minimum Volatility to reduce volatility, but unlike the Vanguard fund, USMV tracks an index.

Investors can also tilt toward more-defensive stocks at the smaller end of the large-cap spectrum through iShares Enhanced U.S. Large-Cap IELG (0.18% expense ratio). It targets large-cap stocks trading with attractive value, quality, and smaller-cap characteristics and attempts to slightly reduce the portfolio's volatility through the way it weights its holdings.

Disclosure: Morningstar, Inc.'s Investment Management division licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)