Why Product Safety Risk Matters for Stocks

Plane crashes and unsafe medicine are among key ESG governance risks for your investments.

/s3.amazonaws.com/arc-authors/morningstar/220f0649-85f9-4004-a281-b91d9bc53139.jpg)

/s3.amazonaws.com/arc-authors/morningstar/64f4b163-f518-4e34-84eb-bda92c5b0e33.jpg)

On Oct. 29, 2018, a Lion Air Boeing 737 MAX airplane crashed with no survivors. Just four months later, an Ethiopian Airlines 737 MAX had an eerily similar fatal nosedive. The entire MAX fleet was quickly grounded in March 2019, as it was revealed that a deficient flight control system caused the combined 346 deaths.

Unfortunately, this was a reminder what can happen when product governance—the oversight of product safety and trust—breaks down. Additional investigation uncovered a series of training blunders and lax oversight by Boeing, compounded by failures at the Federal Aviation Administration and its too-cozy relationship with the aircraft manufacturer. Boeing BA paid $2.5 billion in fines and compensation, and resumed service of the 737 MAX in December 2020 after rigorous recertification. Over this period, Boeing shares fell 45% while Airbus was down 14% and the Morningstar Global Markets Index was up 40%.

ESG Governance Risks Include Product Safety

Environmental, social, and governance risks have become more widely discussed and considered in investment decisions. Investors have focused on climate change and data privacy, for example. But it’s also critical that companies deliver products safely and as expected. What’s less clear is how investors should think about this product governance risk in a structured and repeatable fashion.

So, what exactly is product governance? It’s a company’s management of the entire lifecycle of its products and services, to prevent adverse and unexpected consequences for its customers and end-users. The key here is the difference in a customer’s expectations and the actual outcome. For example, choices around marketing can influence consumer expectations, inadequate safety and reliability can affect actual outcomes, and how a company responds to failures can shape how customers ultimately perceive the mismatched expectations and outcomes.

Bear in mind that there is a subtle difference between product governance risks and environmental and social product risks. The latter include risks that users are already largely aware of, with tobacco being one example. However, an adverse outcome beyond what is expected—say, a malfunctioning vape caused by poor oversight of the manufacturing process—would be considered a product governance issue.

What Drives Usefulness and Satisfaction?

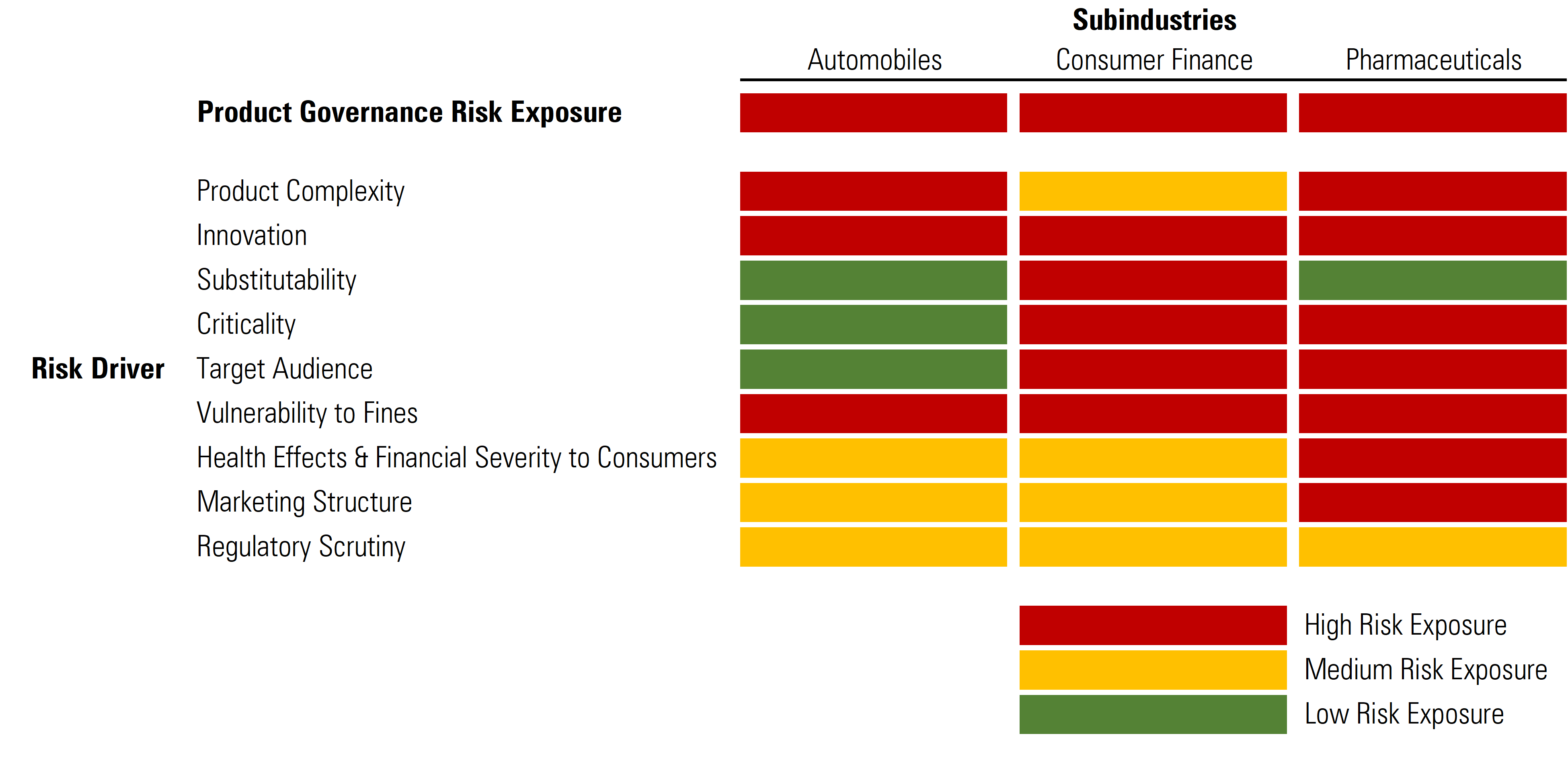

To estimate product governance risk, investors should focus on these drivers that affect user utility and satisfaction:

- Product complexity: Products that are more complex have greater probability of malfunctioning. This can come in the form of mechanical, scientific, or engineering intricacies that can fail. We would also include products that require substantial maintenance, as this adds more opportunity for failure. For example, a jet engine is incredibly complicated. That complexity makes it possible to power a plane through the air, but also introduces the potential for failure.

- Innovation: New and innovative products potentially have higher likelihood of failure or unknown consequences than products that have existed for a long time. Additionally, firms face risk through potential miscommunication with customers. The lack of market experience and information about a new, unique product means the product has a higher risk of a mismatch with customer expectations. For example, although Tesla’s TSLA autopilot technology is meant to take responsibility away from drivers, drivers are still supposed to pay attention. However, in practice there have been a few cases of drivers sleeping, sitting in the back seat, and other forms of dangerous behavior.

- Substitutability: An investor should consider whether a company’s products have alternatives, and whether there are switching costs for using a different product. If a product has no or few viable alternatives, or if it’s difficult to switch products, customers have a higher tolerance for any product failures or unintended outcomes. Here, looking at companies with economic moats based on switching costs can help identify firms that are somewhat protected from this risk. Investors can also look at industry concentration to estimate the availability of alternatives.

- Criticality: Essential items, such as utilities, pharmaceuticals, and healthcare services, are critical for daily life, and disruption would cause wide-scale harm. By comparison, nonessential items often have negative outcomes that are less dramatic and less detrimental.

- Target audience: Products sold to individual consumers are more likely to be scrutinized by regulators than products sold to businesses. Furthermore, products sold to vulnerable populations like children or senior citizens face higher risks still. These groups might not only be disproportionally affected by faults, but incidents affecting them are often magnified in the public eye.

- Vulnerability to fines: Product governance failures are often punished with fines or legal settlements. A firm’s ability to weather a large financial penalty is a crucial consideration. Bigger, more profitable companies with healthier balance sheets can better absorb a financial penalty, all else equal.

- Health effects and financial severity to consumers: When a product fails, the potential consequences to the company are often magnified if it affects the health of the consumer. For example, the consequence to a food company will be far greater if it accidentally poisons consumers than if it made a flavoring mistake. Similarly, the consequence is far greater if there’s a material financial effect on consumers’ financial well-being. For example, offering margin trading accounts for speculative stock investing without proper diligence could result in large irrecoverable losses, increasing product governance risk.

- Marketing structure: The common selling structure in an industry can affect risk. For example, off-label marketing in the pharmaceutical industry creates extreme risk of misuse. Predatory or unethical marketing practices can also lead to adverse outcomes for customers.

- Business hurdles: Lastly, the presence of a regulatory agency for a company’s products adds additional product governance risk. If a failure occurs, the agency has established authority and mechanisms to enforce financial penalties, recalls, or other punishments.

A Closer Look at Automakers, Drug Companies, and Consumer Finance Companies

Based on these factors, a few industries with high product governance risk exposure are worth highlighting: automobiles, consumer finance, and pharmaceuticals.

All these industries are consumer-facing and could have a severe financial and/or health impact on the consumer. Automakers and pharmaceutical companies offer highly complex products and are reliant on innovation. Consumer finance and pharma companies deliver especially critical products and services, and both industries have a history of unethical marketing or advertising practices. Additionally, all three industries face the jurisdiction of regulators.

We See Opportunity in Stocks with High Product Governance Risk Exposure

We’ve identified companies in all three industries with meaningful product governance risk exposure but with attractive risk-adjusted exposure.

- For autos, Morningstar Sustainalytics assigns BMW BMWYY a high ESG risk score because automakers typically face a number of lawsuits over product defects and safety issues related to driverless vehicle technology. Nevertheless, equity research analyst Rich Hilgert sees the stock as undervalued, as ESG risks are more than priced in and brand strength has enabled premium pricing across all BMW products, supporting a narrow economic moat.

- In consumer finance, SoFi Technologies SOFI is exposed to potential governance risk surrounding the quality of its financial products and lending practices as well as its marketing practices. This is magnified by its business focus on individual consumers whose financial health can be affected. Still, the stock currently trades in 5-star territory according to equity analyst Michael Miller, offering meaningful risk-adjusted upside to SoFi’s unique strategy of selling a full financial services suite to young, high-income individuals underserved by traditional full-service banks.

- According to Morningstar Sustainalytics, drug manufacturer AstraZeneca AZN has high product governance risk exposure, especially from pricing risk. However, equity research analyst Damien Conover, CFA, estimates lower ESG pricing risk given lower relative exposure to the U.S., moderate price discrepancies of its products between the U.S. and international markets, and fewer drugs with unjustified prices. Also, we see medium risk from business ethics and product governance issues with a relatively low percentage of drugs targeted for litigation. AstraZeneca is currently undervalued, offering a wide Morningstar Economic moat and attractive exposure to an industry-leading portfolio of patent-protected drugs and promising pipeline, featuring cancer drugs that have potential pricing power.

For investors, we think it’s important to remember there’s more to ESG than environmental and social factors. But it’s critical to also keep governance risks in context. Even stocks with material product governance risk exposure can look attractive for long-term minded investors looking to integrate ESG risk considerations into their analytical process. As with most risks, the market can overestimate the probability and importance of product governance risk. When that happens, it can create profitable opportunities for smart investors.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/220f0649-85f9-4004-a281-b91d9bc53139.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/64f4b163-f518-4e34-84eb-bda92c5b0e33.jpg)