The Wall Street Checklist

The good, the bad, and the ugly.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Rephrasing My column "No, Wall Street Is Not Rigged" created something of a failure to communicate. The article claimed that retail stock market investors face no meaningful barriers. They may directly buy and sell the same companies as can institutions, at the same prices. Or, if they wish, they can hold the entire marketplace through an index fund. The cost for that service is virtually nothing. (Fidelity Zero FZROX funds do not require the modifier, having expense ratios of 0.00%.)

To my surprise, many readers objected. They read that article as implying that Wall Street consistently treats its customers well. That was certainly not my intent. As with all industries, Wall Street's quality varies. Some investments I recommended to my own mother, while others I deemed fit only for my stepmother. (Just kidding about that second part, step-mama is fine.)

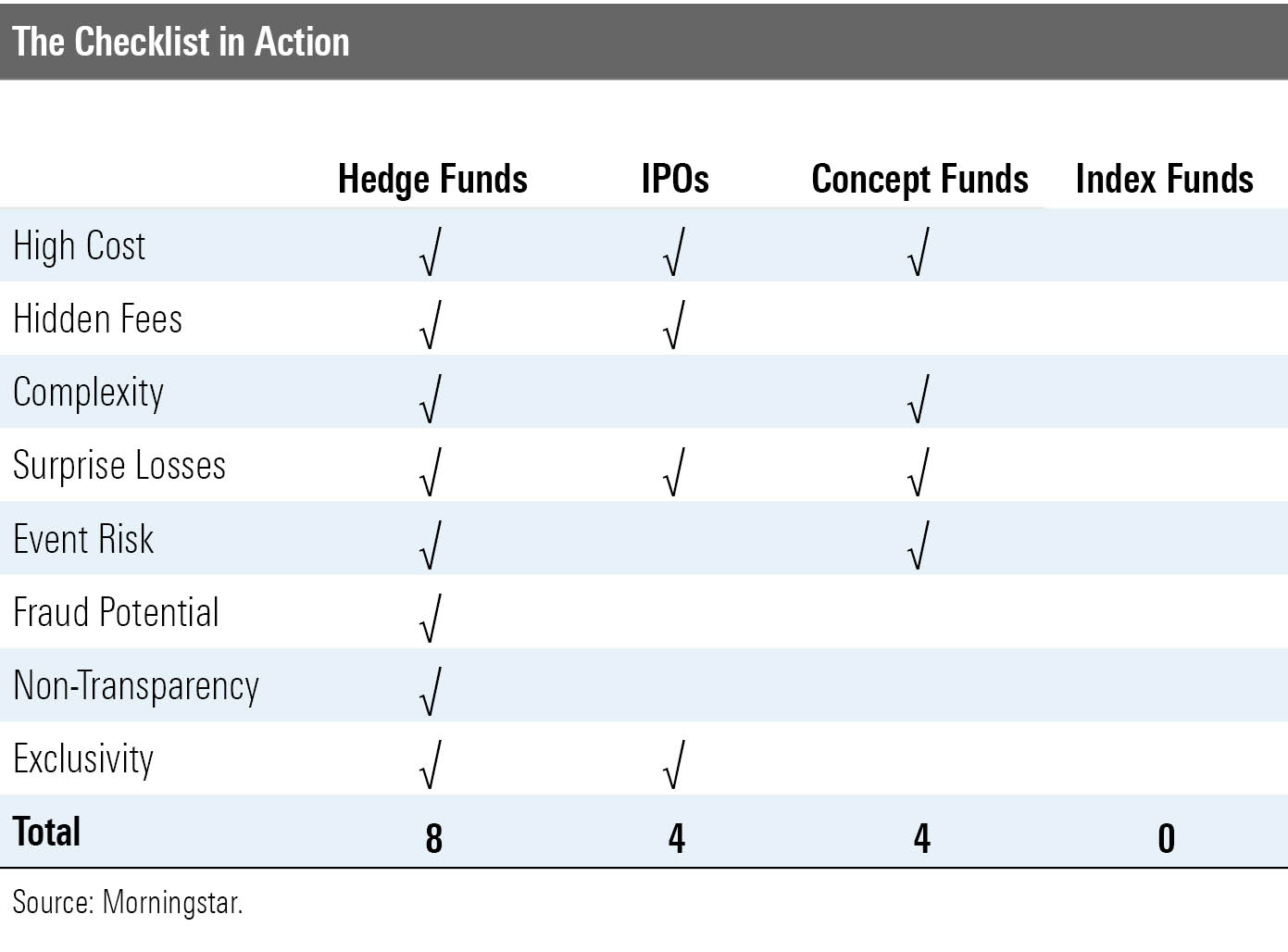

The Checklist To illustrate the difficulty of generalizing about the industry, I devised a Wall Street Checklist. It evaluates investments according to eight attributes of investor unfriendliness. Lower scores are therefore better. (However, the parallel with golf is incomplete, because although even the legendary Kim Jong-il required at least one stroke per golf hole, the checklist can score zero.) These are the measures:

1) High Cost This one is straightforward. Example: A mutual fund with a 2% expense ratio.

2) Hidden Fees Hidden fees are either charges that are buried in the footnotes, or which cannot be known at all by outsiders. Example: The difference between a bank's cost of funds and the yield that it pays its CD investors.

3) Complexity Complex investments cannot be easily modeled. Their results are therefore unpredictable. Example: A short-term multimarket income mutual fund, which was an investment of the late 1980s that bought higher-yielding European currencies while shorting the continent's lower-yielding currencies.

4) Surprise Losses Surprise losses occur when an allegedly safe investment loses money or when one that was known to be risky proves to be even riskier than expected. Example: When European currencies diverged rather than converged in 1992, thereby depressing the prices of short-term multimarket income funds.

5) Event Risk Event risk is a special form of surprise loss, in that it affects only a single investment, as opposed to a larger group. Example: In 2018, an exchange-traded fund called VelocityShares Daily Inverse VIX Short-Term--the name alone violated several criteria--lost more than 90% of its value in a single week. Unfortunately for its shareholders, the fund had gone where no competitor had gone before.

6) Fraud Potential Different investments pose different risks of fraud. Cheating mutual fund shareholders is difficult, thanks to the SEC's oversight. However, fleecing hedge fund investors is an easier task. Example: Madoff, Bernie.

7) Non-Transparency Purchase a stock, you will be notified of the commission that you paid (if any), the number of shares that you now own, and the price commanded by those shares. That transaction was open and clear. However, many investments are not. For example, special purpose acquisition companies, or SPACs, collect investor monies first, then inform shareholders later what their assets procured.

8) Exclusivity Many investments are not open to the broad public but are instead restricted to institutions and/or unusually wealthy investors. Example: Private equity funds.

Of course, these are other possible criteria. This list is not exhaustive. It is instead a suggestion--a framework for distinguishing between those Wall Street offerings that come with extensive strings attached, and those that warrant investor trust.

Four Examples The table below depicts the checklist results for four investments: 1) hedge funds, 2) IPOs, 3) concept funds, and 4) index funds. Hedge funds and index funds are self-explanatory. By IPOs, I mean the launch price of a stock's initial public offering (as opposed to its aftermarket trading). Finally, the term of "concept funds" refers to mutual funds with complicated strategies, such as tactical-allocation funds or the previously mentioned short-term multimarket income funds.

Hedge funds and index funds occupy opposite ends of the spectrum, with hedge funds receiving a perfectly bad score, and index funds one that is perfectly good. Those results cannot be disputed. One can disagree with the grading system, but not with the grades. Hedge funds set off every alarm. Meanwhile, index funds avoid every checklist issue, for the simple reason that they were built that way. Index funds were designed to appeal to Wall Street skeptics.

The scores for the other two investments require some clarification.

IPOs have high costs because investment banks that underwrite IPOs ask 7% for their services (a charge that is usually negotiated, but not substantially lower). Those fees are hidden because buyers do not see them. In theory, IPOs are open to all parties. In practice, however, bankers allot popular IPOs to their largest and best customers. Effectively, the distribution process is exclusive.

Concept funds are partially saved from themselves because they are governed by the Investment Act of 1940. Under its provisions, concept funds cannot levy hidden fees, operate without transparency, or readily commit fraud. True, they can become exclusive by demanding a high minimum investment, but that would undermine their purpose, since they target the unsophisticated. That leaves four potential triggers--and, unfortunately, concept funds check each of those boxes.

A Starting Point The Wall Street Checklist does not provide investment recommendations. Although hedge funds haven't excelled in recent years, they have at times sharply outperformed stock index funds (most notably, during the 2000-02 technology sell-off). Similarly, while competing with institutions to buy IPOs is usually a losing tactic, there are instances when demand is so high that even latecomers turn a handsome profit.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}