Is Cryptocurrency Really a Portfolio Diversifier?

Cryptocurrency has a low correlation with traditional asset classes, but correlations often spike during down markets.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

After spending its first decade or so of life as more of a fringe asset class, cryptocurrency has recently started gaining institutional acceptance. Bitcoin, the oldest and most established cryptocurrency, still accounts for the majority of investor interest and assets, but a long list of other digital currencies has also attracted more attention from both retail and institutional investors over the past couple of years. The value of assets invested in cryptocurrency globally totaled about $1.8 trillion as of Jan. 31, 2022.

In our recently published 2022 Diversification Landscape Report, we looked at how different asset classes performed in the past couple of years, how correlations between them have changed, and what those changes mean for investors and financial advisors trying to build well-diversified portfolios. We found that while cryptocurrency has an unusually low correlation with traditional asset classes, its volatility makes it tough to use in a diversified portfolio.

Recent Performance Trends

Interest in crypto has been driven by several factors, including spectacular long-term returns since bitcoin was first minted in early 2009. Other key drivers include distrust of national governments and traditional financial institutions, fears that resurgent inflation could be more than transitory, and excitement about the technological potential of digital payments and other innovations related to cryptocurrency, such as blockchain, decentralized finance, and nonfungible tokens. As an asset that exists purely in digital form, cryptocurrency is fundamentally different from other major asset classes.

Crypto's performance over the past couple of years puts its unusually volatile characteristics in sharp relief. After posting a 104% runup in the first quarter of 2021, the CMBI Bitcoin Index dropped about 40% in the second quarter, followed by a 25.3% gain in the third quarter, and then another roller-coaster ride in the fourth quarter, when bitcoin briefly hit an all-time high and then plummeted 20% as high-risk assets sold off in December. These dramatic performance swings have continued in early 2022. After dropping 16.5% in January, the CMBI Bitcoin Index partially recovered in February and March, but is still well below previous peak levels.

The turbulent market in 2020 also highlighted crypto's erratic performance trends. As the ultimate risk-on asset, cryptocurrency was hit hard in the early-2020 bear market despite its generally low correlation with major asset classes such as stocks and bonds. The CMBI Bitcoin Index dropped about 38% during the market downdraft from Feb. 19, 2020, through March 23, 2020, while the CMBI Ethereum Index was down about 54%. In other words, major cryptocurrencies lived up to the maxim that all correlations go to 1.0 in a bear market. Both assets then bounced back in a spectacular way, with bitcoin posting a 305.4% for the full year and ether clocking in with gains of 479.4%.

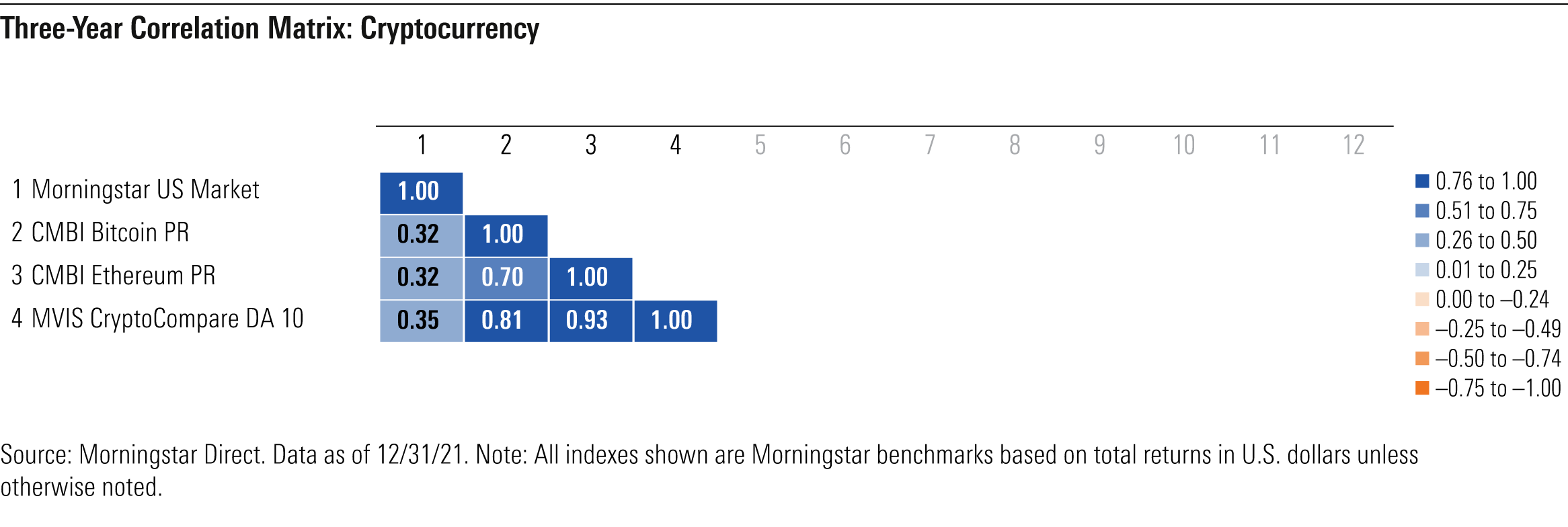

These dramatic performance swings underscore some of the limits of correlation metrics. Correlations often spike during periods of market crisis, and low correlations don't guarantee that a given asset class will hold up better during market drawdowns. That said, cryptocurrency has continued to show relatively low correlations with most other major asset classes, as shown in the table below.

For the trailing three-year period, the CMBI Bitcoin Index had a correlation coefficient of just 0.32 with stocks (as measured by the Morningstar US Market Index) and an even lower correlation of just 0.14 with bonds (as measured by the Morningstar US Core Bond Index). With market sentiment switching to a risk-off mindset, however, bitcoin's correlation with stocks has been significantly higher in recent months. Bitcoin is often described as digital gold, but its performance has been fundamentally different: Bitcoin's correlation with gold was just 0.08 over the trailing three-year period.

While bitcoin remains by far the largest and best-known cryptocurrency, the cryptocurrency market isn't monolithic. The cross-correlation between the CMBI Bitcoin and Ethereum indexes was just 0.70 for the trailing three-year period. (Our recently published Cryptocurrency Landscape report dives into various digital currencies in more detail.)

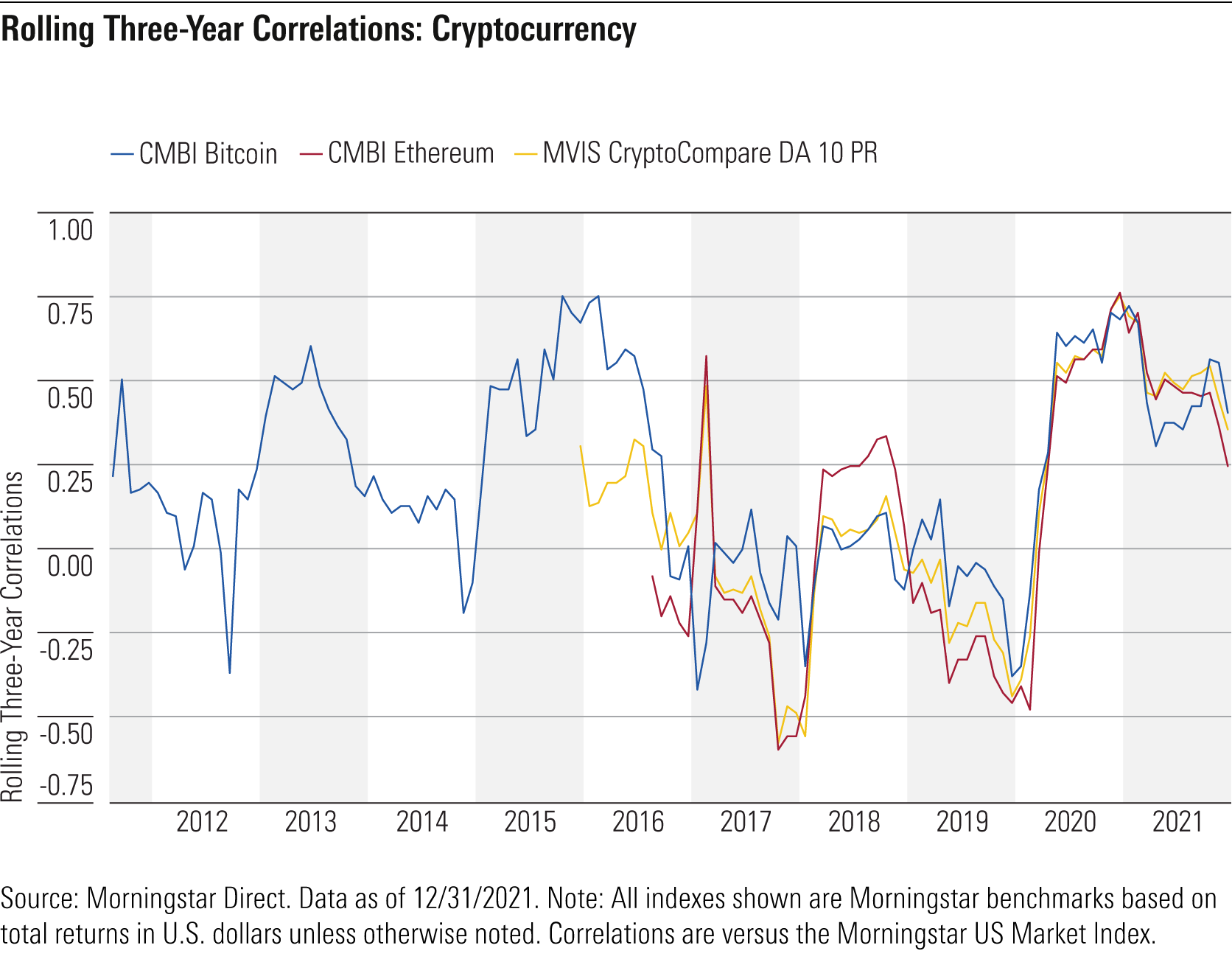

Longer-Term Trends

As cryptocurrency has moved more into the mainstream, its correlation with other major asset classes has trended up a bit, as shown in the graph below. Bitcoin's correlation with the Morningstar US Market Index has been as low as negative 0.05 for some previous periods but has gradually increased over the past few years. Ether and other major cryptocurrencies have shown similar patterns. This trend looks likely to increase as more institutional investors and individuals add cryptocurrency to their portfolios, though current correlation numbers are still quite low compared with most other major asset classes.

Portfolio Implications

As mentioned above, cryptocurrency's low correlation with traditional asset classes may be a bit of a false flag because of its tendency to spike during market corrections. Diversification value is one potential reason to add cryptocurrency to a portfolio, but investors should also consider other factors, such as their ability to hold on through crypto's periodic downdrafts, which have been unusually swift and severe. Crypto aficionados embracing the "hold on for dear life" mindset have fared well over time, but investors who are more skittish can easily get whipsawed by extreme short-term price movements.

It's also worth noting that cryptocurrency's volatility profile means that even small doses can have an outsize impact when added to other portfolio holdings. As a result, most investors will want to keep cryptocurrency exposure to a minimum and carve out any allocations from stocks, not bonds.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HTLB322SBJCLTLWYSDCTESUQZI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TAIQTNFTKRDL7JUP4N4CX7SDKI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)