Is CVS Stock a Buy After Blue Shield of California Dropped the Company?

With new untested service providers attempting to disrupt the industry, here’s what we think of CVS stock.

/s3.amazonaws.com/arc-authors/morningstar/27df33e4-c5eb-4dc8-805e-babc7c688b65.jpg)

CVS Health CVS was dropped by Blue Shield of California as a pharmacy benefit manager last week in favor of a coalition of providers that includes Amazon Pharmacy and Mark Cuban’s Cost Plus Drugs. Here’s Morningstar’s take on this development.

Key Morningstar Metrics for CVS

- Fair Value Estimate: $103

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Narrow

- Morningstar Uncertainty Rating: Medium

What We Thought of CVS’ Lost Deal

PBM landscape shifts: Over the past decade or so, the top three PBMs (CVS, Cigna CI, and UnitedHealth UNH) have been consolidating power. However, in recent years, upstarts like Amazon.com AMZN have said they want to disrupt the industry to help lower drug prices in the United States. We hadn’t seen much traction for those new entrants prior to this contract win, but this could signal the start of a change.

Moat concerns: We don’t think this development changes any of our moat ratings for the managed care organizations we cover. However, according to reports, representatives of Blue Shield of California estimated that this switch could help it save 10%-15% on its drug costs. If such a reduction is achieved and these new PBMs gain further clients, it could erode profitability in the industry. This is why the market reacted so much to this news.

Major client loss came as a surprise: In 2022, CVS generated about 37% of its operating profits from its PBM—its largest business, followed by its retail stores (33%) and medical insurance operations (30%). While we saw some policy risks due to transparency issues, we really didn’t expect a major client to jump ship, especially to untested new entrants. Clients can control whether their pay is fee-based or variable-based. This suggests transparency may be a larger problem than we thought.

New entrants represent a possible threat: It remains to be seen whether customers switching from incumbents to new entrants becomes a massive trend, but we thought it was prudent to recognize that threat with our new fair value estimate for CVS.

CVS stock now looks like a buy: In our opinion, CVS shares remain significantly undervalued (currently in 5-star territory), as do most MCO shares. Centene CNC, Cigna, Elevance ELV, and Humana HUM are all in 4-star territory. The market may be giving long-term investors an opportunity in the MCO space with these discounts.

CVS hit more directly than competitors: Obviously, Cigna and UnitedHealth were not directly affected by the Blue Shield of California development. Also, given how much cash flows had already built up in our valuation model for Cigna, along with the diversity of UnitedHealth’s business (its PBM is only about 16% of its operating profits), our fair value estimates didn’t change materially for those two companies when we adjusted our longer-term profitability estimates on their PBM businesses.

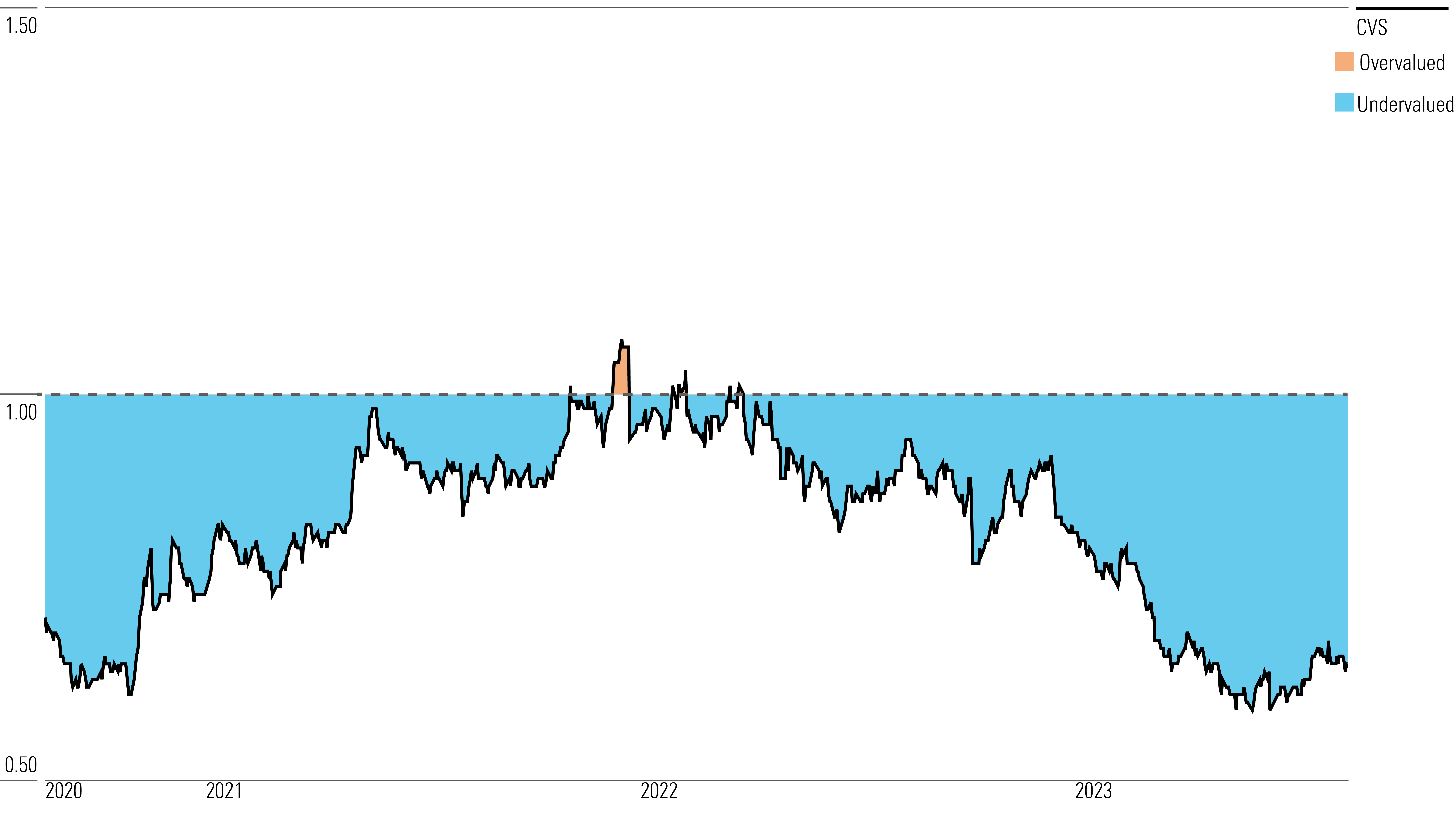

CVS Stock Price

Fair Value Estimate for CVS

With its 5-star rating, we believe CVS’ stock is undervalued compared with our long-term fair value estimate.

We reduced our fair value estimate to $103 per share from $113 to reflect pending contract losses and general uncertainty in its PBM business. This new fair value estimate is based on discounted cash flows but implies roughly a 12 times multiple on 2023 expected earnings.

CVS is especially facing significant growth hurdles in its PBM and Medicare Advantage businesses in 2024-25. New competitive forces in the PBM business create some long-term uncertainty around its top-tier position, which also pushed down our long-term profit growth assumptions.

In this context, we expect revenue to grow in the mid-single digits and operating profits to grow in the low-single digits compounded annually through 2027. We think share repurchases could push up adjusted earnings per share a bit to the mid-single digits annually through that period, including double-digit earnings growth toward the outer years of our five-year forecast period, including share repurchases and expansion of the firm’s healthcare services.

Overall, by major business line, we expect the strongest growth from CVS’ medical insurance operations (high-single digits), especially given recent expansion initiatives and the potential for the company’s employer-based stronghold to benefit from upcoming Medicaid redetermination activities. However, we expect only flat PBM operations and mid-single-digit growth in its retail stores after incorporating potential competitive and policy pressures in those businesses. Newly acquired healthcare services should add a higher-margin, higher-growth opportunity for CVS as well.

Read more about CVS’ fair value estimate.

CVS Price/Fair Value

Economic Moat Rating

We believe CVS has a narrow economic moat. As a top-tier medical insurer, PBM, and pharmacy retailer, we believe it possesses enough scale-related cost advantages to generate economic profits in the long run.

Even after the late 2018 Aetna merger (which cut into returns on invested capital including goodwill) and its recent healthcare services acquisitions, we estimate that CVS’ ROICs should remain above its capital costs throughout our explicit 10-year forecast period. CVS generates profits almost equally among its three major segments, and we see the medical insurance and PBM assets as generally stronger than the retail store chain.

In medical insurance, we see two moat sources: cost advantage and network effects. An insurer’s cost advantages relate primarily to scale, both broadly and locally. The legacy Aetna operations represent the third-largest insurer we cover, with about 26 million members. With such a significant scale in the fragmented health insurance market, we believe CVS benefits from local scale advantages in specific metropolitan markets. Local-scale advantages allow for greater negotiating leverage, which contributes to cost advantages in each location. When these advantages are significant enough, we think CVS’ insurance operations benefit from a network effect.

According to the American Medical Association, the share of local insurance markets in the U.S. that were highly concentrated grew to 75% in 2021 from 71% in 2014, with the leaders likely taking share in those markets. In communities where CVS already has a substantial market share, it can offer lower costs or more benefits per member than its peers. If such offerings are compelling enough, more employers will be attracted to CVS’ insurance plans in those communities, and local service providers, such as hospitals and physician groups, will have more incentive to join and offer lower prices to CVS’ insurance networks to gain access to its large and growing membership rolls.

As CVS’ local market share rises, its negotiating leverage with providers also rises, which can create a virtuous cycle wherein CVS attracts even more clients and more providers to its insurance network in that area. Overall, these dynamics create barriers to entry for would-be competitors, as compiling an attractively priced provider network in a new geography would be difficult without an established membership pool.

We see some switching costs in this business, with contracts typically around three years in length and annual retention rates in the high 90s for all three of the top-tier PBM players. Switching administrative activities, partner relationships, and pharmacy benefit plan specifications to a new PBM can be time-consuming and onerous, which impedes clients with limited realistic alternatives, in our opinion. However, switching is possible, and the loss of specific clients could constrain the firm’s growth eventually, especially as new insurance competitors like Elevance, Amazon, and the Mark Cuban Cost Plus Drug Company take aim at this market.

Read more about CVS’ economic moat rating.

Risk and Uncertainty

CVS has a Morningstar Uncertainty Rating of Medium, with uncertainty stemming from its long-term efforts to derive synergies from acquisitions, as well as the debate around the U.S. healthcare system that will likely continue until universal affordable coverage is achieved.

The Aetna merger and recent Oak Street acquisition pushed off durable double-digit earnings growth for nearly a decade, which remains a source of frustration for investors still waiting for that industry-standard growth rate. Uncertainty surrounds whether CVS will ever achieve that standard, especially if more acquisitions come into play.

Healthcare policy risks may also plague MCOs like CVS until U.S. healthcare is reformed—the key environmental, social, and governmental risk facing this industry. The Medicare for All scenario debated in the 2020 Democratic Party primaries even called for the elimination of the private insurance industry, which would have threatened CVS’ insurance operations. While that strategy was largely rejected in favor of a more moderate approach, we see headwinds emerging from potential regulations to increase PBM transparency in the near term. Also, long-term policy risks may remain intact until healthcare reform is enacted.

Read more about CVS’ risk and uncertainty.

CVS Bulls Say

- CVS’ diverse operations create the opportunity to view a patient more holistically by managing both medical and pharmacy benefits, which could lead to revenue and cost synergies.

- The firm’s entry into provider services has the potential to improve returns for all segments if it can help patients more easily and cost-effectively manage chronic conditions through early intervention.

- CVS’ PBM remains an industry leader due to its intense focus on pharmaceutical cost trends, which should continue to attract clients.

CVS Bears Say

- Healthcare reform will likely remain a recurring political topic until universal affordable coverage is achieved in the U.S., and CVS’ stock may experience volatility if scenarios that threaten its prospects gain traction.

- Foot traffic at physical retail stores could continue to decline as consumers increasingly favor online retailers like Amazon, creating the need to reinvent its retail store footprint’s operations.

- Investors continue to wait for double-digit earnings growth from CVS—an industry standard that CVS has delayed achieving time and again.

This article was compiled by Saaketh Tirumala.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/27df33e4-c5eb-4dc8-805e-babc7c688b65.jpg)