Downturn Has Put Communication Services Firms on Sale

Google's online dominance should be able to withstand any shocks.

/s3.amazonaws.com/arc-authors/morningstar/12c6871b-2322-44d8-bd98-0437fa1a0a07.jpg)

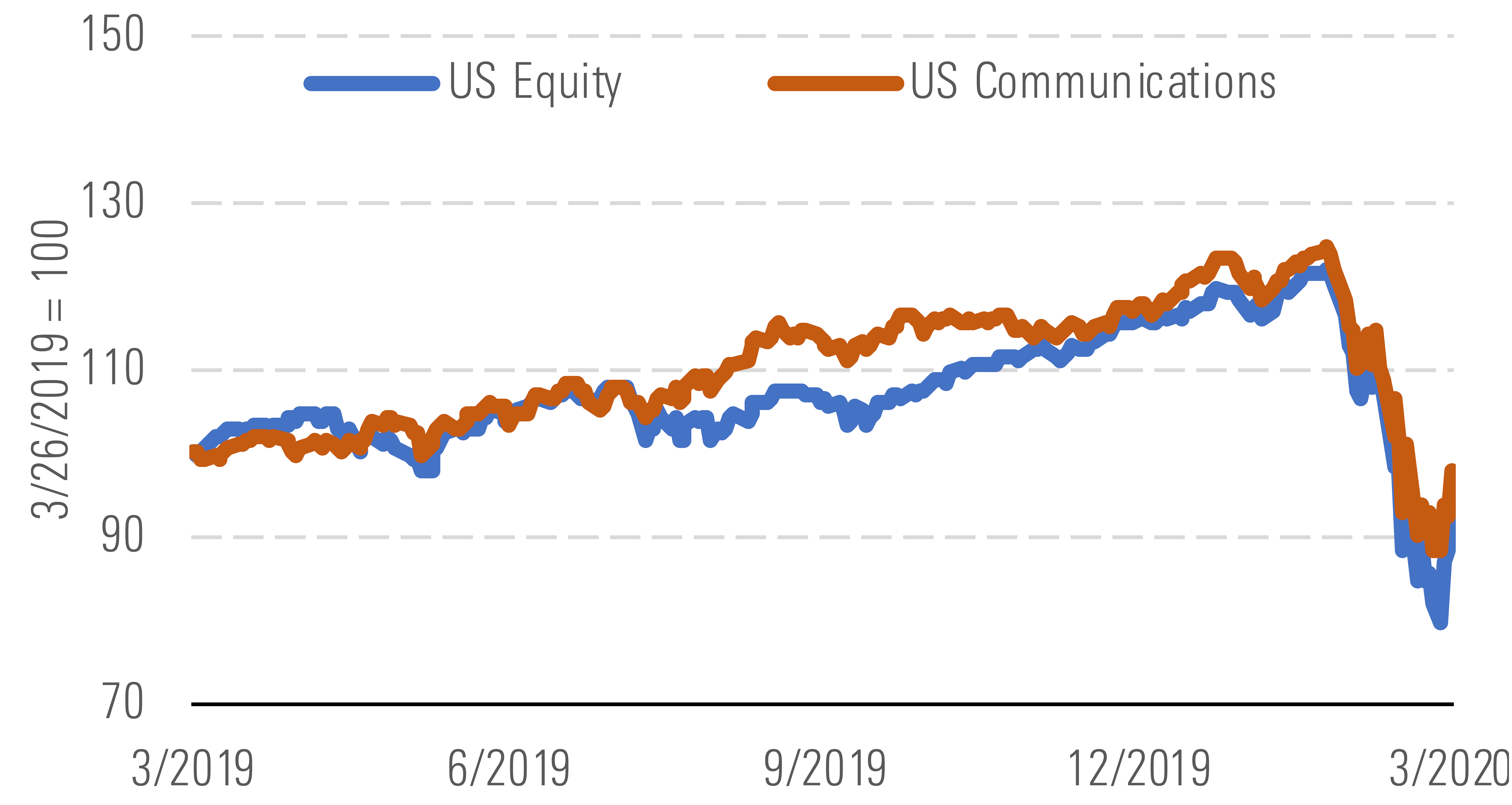

The recently reconstituted communications sector has held up relatively well in the market sell-off but has still seen significant carnage. The Morningstar US Communication Services Index has declined about 16% over the past three months versus 19% for the broader market. Heavyweight Alphabet, which accounts for 28% of the sector index, is down only 15% over this period, though it has shed nearly $150 billion in value. Advertising spending will certainly take a hit as firms tighten budgets in response to COVID-19. Alphabet’s Google and YouTube platforms won’t be immune, but we don’t expect the firm’s online dominance to wane. The stock now looks more attractive to us than it has since the short-lived market downturn in late 2018.

Cold comfort: The sector has outperformed the broader market. - Morningstar

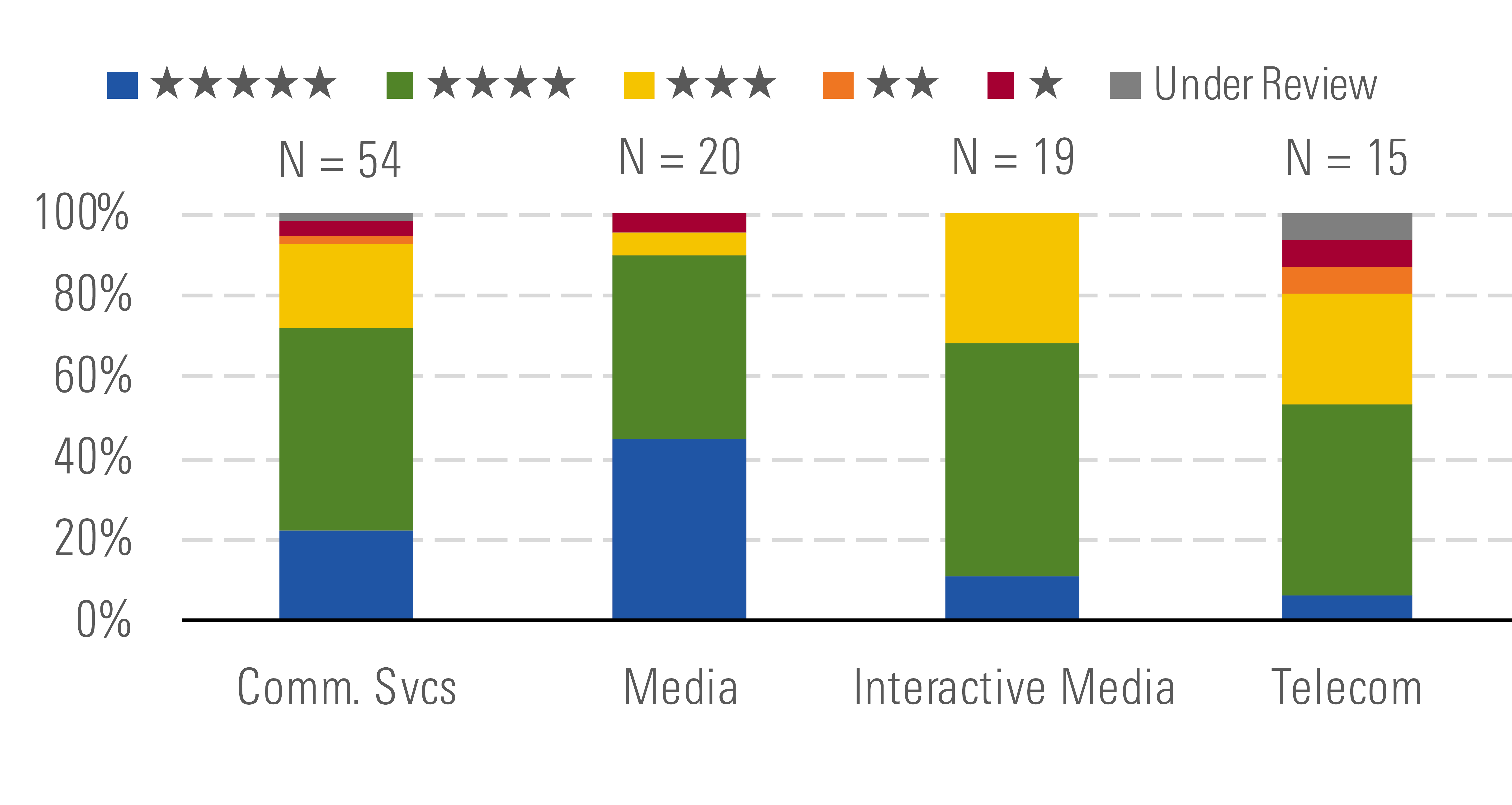

Traditional media looks best, but good valuations abound. - Morningstar

High-quality businesses are also on sale in the traditional telecom sector, including AT&T, Comcast, and Verizon. We expect the telecom business will hold up well even in the face of a significant recession. Internet access, both at home and on the go, has become indispensable for consumers and businesses, enabling communication across a broad array of platforms, access to information, and a wide range of services. As consumers stay indoors, demand for wireless services may decline, but most consumers will still need the ability to communicate when they do leave home. Economic turmoil could accelerate cord-cutting, but television distribution contributes very narrow margins relative to the Internet access market.

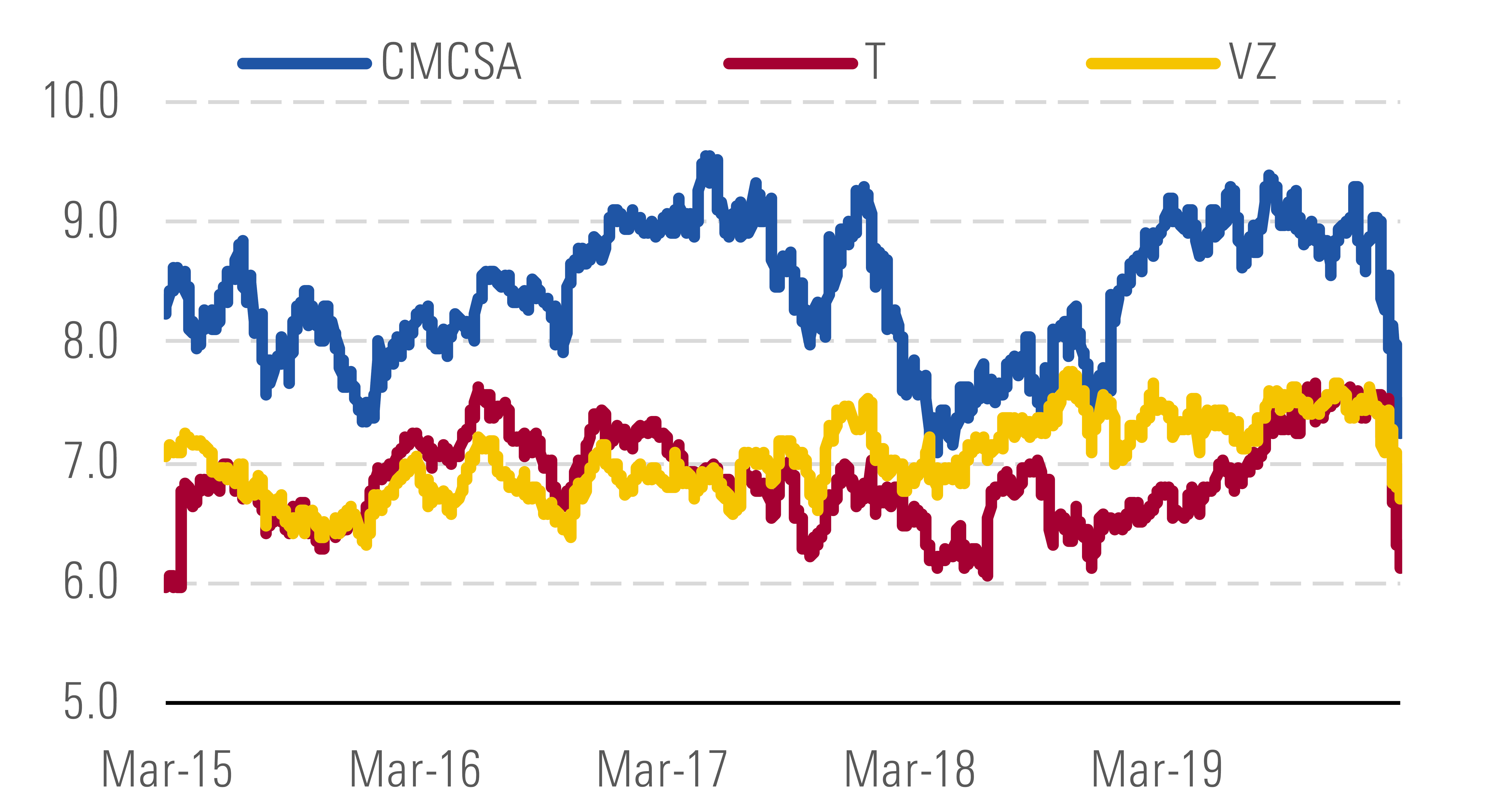

Telecom enterprise value/EBITDA multiples near five-year lows. - Morningstar

The media business hasn’t been immune to COVID-19, especially Disney’s and Comcast’s theme parks. Disney has taken the biggest direct hit from COVID-19 among traditional media firms because its parks contribute about 30% of total revenue (Comcast’s generate 5%). But the pandemic also provides Disney with opportunities to extend its reach in new ways. With children home from school, Disney+ has likely garnered increased attention relative to other streaming services, with moves like the early release of Frozen 2. We expect firms with strong content franchises and solid balance sheets, like Comcast and Disney, will manage reasonably well through a downturn. The market sell-off has hit smaller, riskier firms especially hard. While we generally think current valuations make high-quality firms especially attractive, several shakier firms, like ViacomCBS and CenturyLink, now provide substantially more upside than they did three months ago without a significant increase in risk.

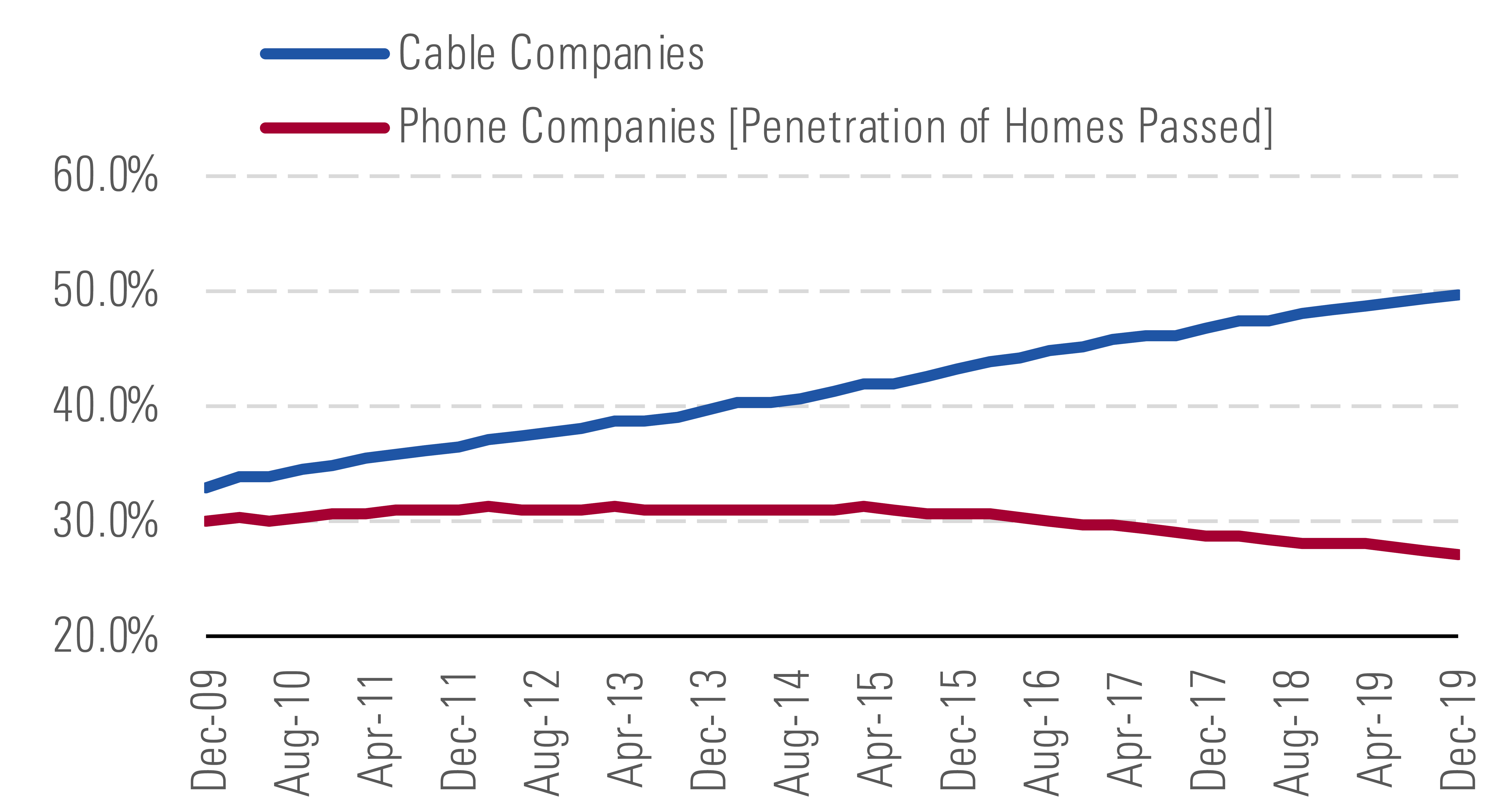

Cable continues to gain share versus the phone companies. - Morningstar

Top Picks

Alphabet GOOGL Economic Moat Rating: Wide Fair Value Estimate: $1,400 Fair Value Uncertainty: High

Google's ad revenue will take a hit this year, but it is likely to maintain its dominance in online advertising, which is bound to recover quickly after the pandemic eases and firms look to quickly regain consumers’ attention. Over the longer term, we expect a return to strong subscription and ad revenue growth at YouTube and further growth in the firm’s cloud offerings. The Waymo and Verily call options represent additional upside to our fair value estimate. Verily's recent efforts to work with government agencies and create sites for coronavirus testing and screening may create commercialization opportunities in the long run.

Comcast CMCSA Economic Moat Rating: Wide Fair Value Estimate: $49 Fair Value Uncertainty: Medium

Comcast’s core cable business (about 70% of consolidated EBITDA) is in great shape and should see minimal impact from COVID-19. An increase in telecommuting and television streaming could further highlight Comcast’s network advantage versus phone rivals. The theme parks business will be hurt, but it is small at 7% of EBITDA in 2019. Longer term, the parks business is a key asset behind Comcast’s media efforts. The Sky acquisition added to Comcast’s debt load, but the balance sheet remains solid. Net debt is at 3.0 times EBITDA versus around 4.6 times EBITDA for cable peer Charter and 5.3 times at Altice USA.

Disney DIS Economic Moat Rating: Wide Fair Value Estimate: $132 Fair Value Uncertainty: High

We believe Disney remains the strongest media company globally, with a tremendous number of content franchises, monetized across multiple platforms, including movies, home video, merchandising, theme parks, and even musicals. We expect that the parks business will bounce back after COVID-19 is contained, as some portion of the lost parks revenue will be recovered as people take trips that had been deferred. An increase in the number of people, especially children, staying home should accelerate Disney+ adoption, helping build the firm’s future connection with its audiences.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/12c6871b-2322-44d8-bd98-0437fa1a0a07.jpg)