Tax-Efficient Retirement-Bucket Portfolios for Schwab Supermarket Investors

Equity index products are plentiful, but cheap muni funds are scant.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

There’s much to like about investment supermarkets like Schwab’s. They allow investors to graze among individual stocks and bonds, as well as mutual funds and exchange-traded funds. Supermarket investors can build portfolios composed of investment products from many different firms, but yet receive a single statement and trade on a single platform.

Yet building a portfolio with the funds on Schwab’s platform isn’t without challenges—specifically, some of Morningstar’s favorite low-expense bond funds are unavailable on a no-transaction-fee basis—Fidelity, Vanguard, and Dodge & Cox, for example. The same challenge exists for investors looking to use Schwab’s supermarket for their taxable accounts: Inexpensive municipal-bond options that are available without a load or transaction fee are few and far between. Yet one bond manager that has long been a favorite for Morningstar’s analysts is well represented on Schwab’s no-load, no-transaction-fee list: T. Rowe Price. Thus, I populated all three portfolios with T. Rowe’s muni funds.

About the Portfolios

These portfolios employ a bucket strategy, pioneered by financial-planning guru Harold Evensky. The central premise is that the retiree holds a cash bucket (Bucket 1) alongside his or her long-term assets, both stocks and bonds. If the long-term components of the portfolio, especially stocks, hit a rough patch, the cash bucket ensures that the retiree has enough liquid assets to use for living expenses. Bucket 2 covers another eight years’ worth of cash flow needs. It’s designed to deliver slightly more income than Bucket 1, albeit with the potential for some volatility. Bucket 3 is the growth engine of each of the portfolios, geared toward years 11 and beyond of retirement.

The portfolios are designed to be strategic—that is, they’re meant to be bought, held, and rebalanced—rather than tactical. I’ll make changes only when there’s a meaningful negative development in one of our holdings, or if another investment that I like better becomes available. In short, I expect to make very few changes to these portfolios over time, because many retirees don’t want to have to make frequent trades in their portfolios, either.

How to Use Them

The goal of the portfolios isn’t to outperform every other retirement portfolio or strategy ever devised. Rather, the objective is to illustrate sound portfolio-construction and cash-flow-generation principles. Nor do retirees need to completely upend their portfolios in order to implement a similar bucket strategy. Assuming they have solid core building blocks—both stock and bond holdings—they have most of the raw ingredients needed for a bucket portfolio.

Investors should take care to customize their portfolios to suit their own situations—risk tolerance and capacity, of course, but also planned spending. An investor’s own cash Bucket, and in turn the allocations to the other two Buckets, will depend on his or her portfolio spending rate. If an investor is using a lower starting withdrawal rate—say, 3% in the first years of retirement—Bucket 1 would accordingly be smaller (6% versus 8% in my Aggressive portfolio).

Additionally, I used municipal bond funds for the portfolios’ fixed-income exposure. But investors who are in lower tax brackets may be able to earn a higher take-home yield with taxable bonds than they can with municipals.

Aggressive Tax-Efficient Retirement-Bucket Portfolio for Schwab Supermarket Investors

Anticipated Time Horizon in Retirement: 25-plus years

Risk Tolerance/Capacity: High

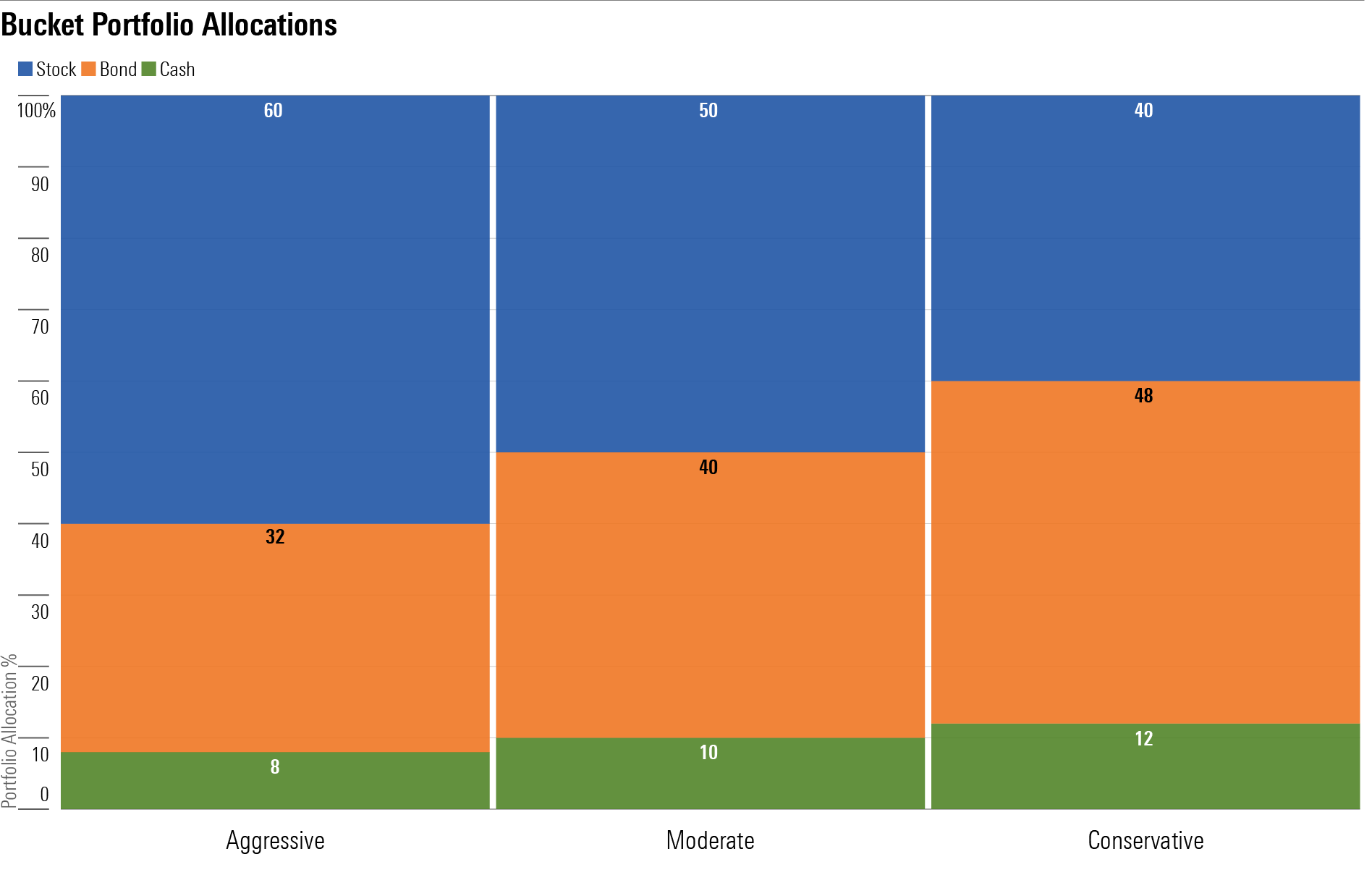

Target Stock/Bond/Cash Mix: 60/32/8

Bucket 1: Years 1-2

- 8%: Cash

Bucket 2: Years 3-10

- 10%: T. Rowe Price Tax-Free Short-Intermediate PRFSX

- 22%: T. Rowe Price Summit Municipal Intermediate PRSMX

Bucket 3: Years 11 and Beyond

Moderate Tax-Efficient Retirement-Bucket Portfolio for Schwab Supermarket Investors

Anticipated Time Horizon in Retirement: 15-25 years

Risk Tolerance/Capacity: Moderate

Target Stock/Bond/Cash Mix: 50/40/10

Bucket 1: Years 1-2

- 10%: Cash

Bucket 2: Years 3-10

- 15%: T. Rowe Price Tax-Free Short-Intermediate PRFSX

- 25%: T. Rowe Price Summit Municipal Intermediate PRSMX

Bucket 3: Years 11 and Beyond

Conservative Tax-Efficient Retirement-Bucket Portfolio for Schwab Supermarket Investors

Anticipated Time Horizon in Retirement: Fewer than 15 years

Risk Tolerance/Capacity: Low

Target Stock/Bond/Cash Mix: 40/48/12

Bucket 1: Years 1-2

- 12%: Cash

Bucket 2: Years 3-10

- 20%: T. Rowe Price Tax-Free Short-Intermediate PRFSX

- 28%: T. Rowe Price Summit Municipal Intermediate PRSMX

Bucket 3: Years 11 and Beyond

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)