The Pros and Cons of Variable Dividends

Some companies are adopting variable dividend policies. Will the trend catch on?

/s3.amazonaws.com/arc-authors/morningstar/32fdd21d-72cb-4981-8f21-b7d0a3f7c87e.jpg)

A version of this article first appeared in the March 2022 issue of Morningstar DividendInvestor.

“As American as apple pie” is a phrase I don’t hear much these days. But if you apply it to the payment of dividends, the standard American approach is to cut the pie in four equal pieces. The vast majority of U.S. dividend-payers distribute quarterly dividends of an equal amount until they set a new--preferably higher--dividend rate.

Yet there’s no regulatory requirement that U.S. companies pay a fixed quarterly dividend, and there are plenty of exceptions to this standard, including multiple monthly dividend-payers in the REIT space. Realty Income O has even trademarked “The Monthly Dividend Company” as a marketing slogan. On the other end of the spectrum, some U.S. companies pay a single annual dividend. Walt Disney DIS suspended its dividend at the beginning of the pandemic and has yet to resume it, but the company paid an annual dividend for years before switching to semiannual payouts in 2015.

Some companies outside the United States, like British American Tobacco BTI and Taiwan Semiconductor Manufacturing TSM, pay a fixed quarterly dividend, but annual and semiannual dividend payments are also common, with many companies paying an interim dividend followed by a final payout for the year, based on full-year earnings. There are some merits and downsides to both of these methods. The four-equal-payments approach provides income-focused investors with a fairly high degree of certainty. Barring a dividend cut or suspension, investors know exactly how much they’re set to receive each quarter from the shares they own. And when evaluating potential investments, they can make apples to-apples comparisons of the current forward yields of different dividend-paying stocks.

One criticism of equal quarterly dividends appeared in a June 2020 article in The Wall Street Journal. London Business School professor of finance Alex Edmans wrote that fixed quarterly dividend payments harm the companies that pay them (and therefore the investors who purchase the shares) because it encourages them to make what he believes could be unwise capital allocation decisions. He argued that quarterly payments of a fixed amount are inflexible and that companies--fearful of the stock price decline that generally accompanies any dividend cut--too often continue to pay their dividends when they can't afford them, or at the expense of better uses of those dollars.

Edmans made the case for buybacks and special one-off dividends as superior ways to return cash to shareholders, because investors don’t have the same expectation that they will continue, as they do with quarterly dividends. Hence, there’s no negative reaction when the same buyback or special dividend doesn’t occur in the subsequent year. There’s another argument--one that Edmans didn’t mention--that can be made against fixed quarterly dividends: Earnings and cash flow aren’t guaranteed, and some dividend-paying companies, especially those in industries that typically see a great deal of variation in cash flow from year to year or quarter to quarter, could be reluctant to devote too much cash to the dividend. They may take an overly conservative approach, keeping the dividend low enough to avoid future dividend cuts and the subsequent punishment of the share price by the market.

A Hybrid Approach: Variable Dividends

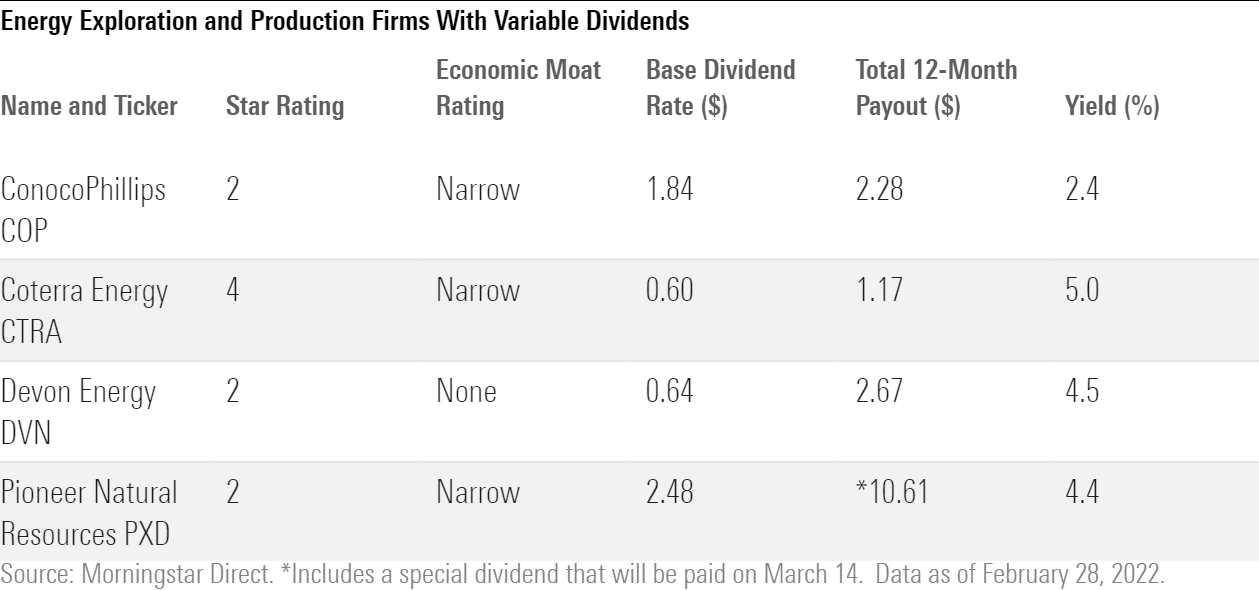

Over the past six months, a number of energy companies, all in the energy exploration and production industry, have introduced variable dividend plans, as detailed in the table below. In most cases, this involves a fixed quarterly dividend amount with a variable component that’s based on a set percentage of the previous quarter’s cash flow, minus the fixed amount.

Why is this taking place in the E&P industry? In general, rising commodity prices are good for the energy sector, and that's certainly something we've seen over the past year. Oil prices are up around 55% over the past 12 months as of Feb. 28. But the energy sector isn't homogenous, and as Morningstar director of research for energy and utilities Dave Meats discussed with me in the latest Dividend-Stock Deep Dive video, different industries within it have varying levels of sensitivity to commodity prices. E&P companies' cash flows are driven by commodity prices directly, whereas refiners make money on commodity spreads rather than prices themselves, and revenues for midstream firms and oil-services companies are merely second derivatives on oil prices (from pipeline toll fees and E&P capital expenditures, respectively).

Watch: Dividend Stock Deep Dive: Energy Ideas

All the E&P companies that Meats covers are trying to boost shareholder returns in one way or another, and some have embraced variable dividends as a method of doing so. Devon Energy DVN CEO Rick Muncrief made this clear during the company’s November earnings call: “This unique dividend policy is specifically designed for our commodity-driven business and provides us the flexibility to return more cash to shareholders....”

Pros and Cons of Variable Dividend Plans

The obvious appeal of the variable dividend approach for income-focused investors is that it is likely to get more cash into their hands than they would receive via a fixed quarterly payout, as these commodity-price-driven companies would otherwise be unwilling to commit to a dividend rate that isn’t tenable from quarter to quarter. And (arguably) receiving the variable component on a quarterly basis is better than having to wait until the end of a company’s fiscal year to receive it.

The main downside is the same one we see with the interim/final approach to dividends: There’s some uncertainty from quarter to quarter, as well as the question of how to calculate a yield rate. One way is adding total dividend payments over the past 12 months and dividing by the current share price.

As to whether this trend will expand to other industries and sectors, we can already see companies outside E&P that have payouts in addition to their regular quarterly dividends, though not necessarily on a quarterly basis. CME Group CME, for instance, pays a special dividend at year-end that is nearly equal to the sum of its quarterly dividend payments for the year.

I believe any further adoption is most likely to occur in industries where companies have highly variable cash flows, though I imagine that investor reaction will drive changes in corporate policies. That is, if corporate boards believe investors are embracing such companies and buying their stock because of such policies, the approach is more likely to propagate.

Morningstar Investment Management LLC is a Registered Investment Advisor and subsidiary of Morningstar, Inc. The information contained in this document is the proprietary material of Morningstar Investment Management. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar Investment Management, is prohibited. Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use.

The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes, and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Dividends are not guaranteed and are paid at the discretion of the stock-issuing company.

This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

Investment research is produced and issued by subsidiaries of Morningstar, Inc. including, but not limited to, Morningstar Research Services LLC, registered with and governed by the U.S. Securities and Exchange Commission.

Morningstar Investment Management LLC is a Registered Investment Advisor and subsidiary of Morningstar, Inc. The Morningstar name and logo are registered marks of Morningstar, Inc. Opinions expressed are as of the date indicated; such opinions are subject to change without notice. Morningstar Investment Management and its affiliates shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Before making any investment decision, please consider consulting a financial or tax professional regarding your unique situation.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/32fdd21d-72cb-4981-8f21-b7d0a3f7c87e.jpg)