Does Factor Profile Diversification Still Work?

Correlations for the major factor profiles are relatively high, but they can still show different returns in different types of markets.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

In our recent examination of asset-class correlations, the "2021 Diversification Landscape," we found that correlations for the five major factor profiles-- value, small-cap, momentum, quality, and low volatility--are all relatively high, but there's still a case for diversifying by factor.

Factor profiles are another way of measuring the underlying factors that help drive equity market returns. Since the 1990s, asset managers and other researchers have focused considerable effort on trying to identify additional characteristics (beyond traditional metrics such as sector, market cap, and value/growth) that help to explain investment management styles and resulting performance differences. Theoretically, each factor should have its own set of performance characteristics and succeed or fail in different types of market environments.

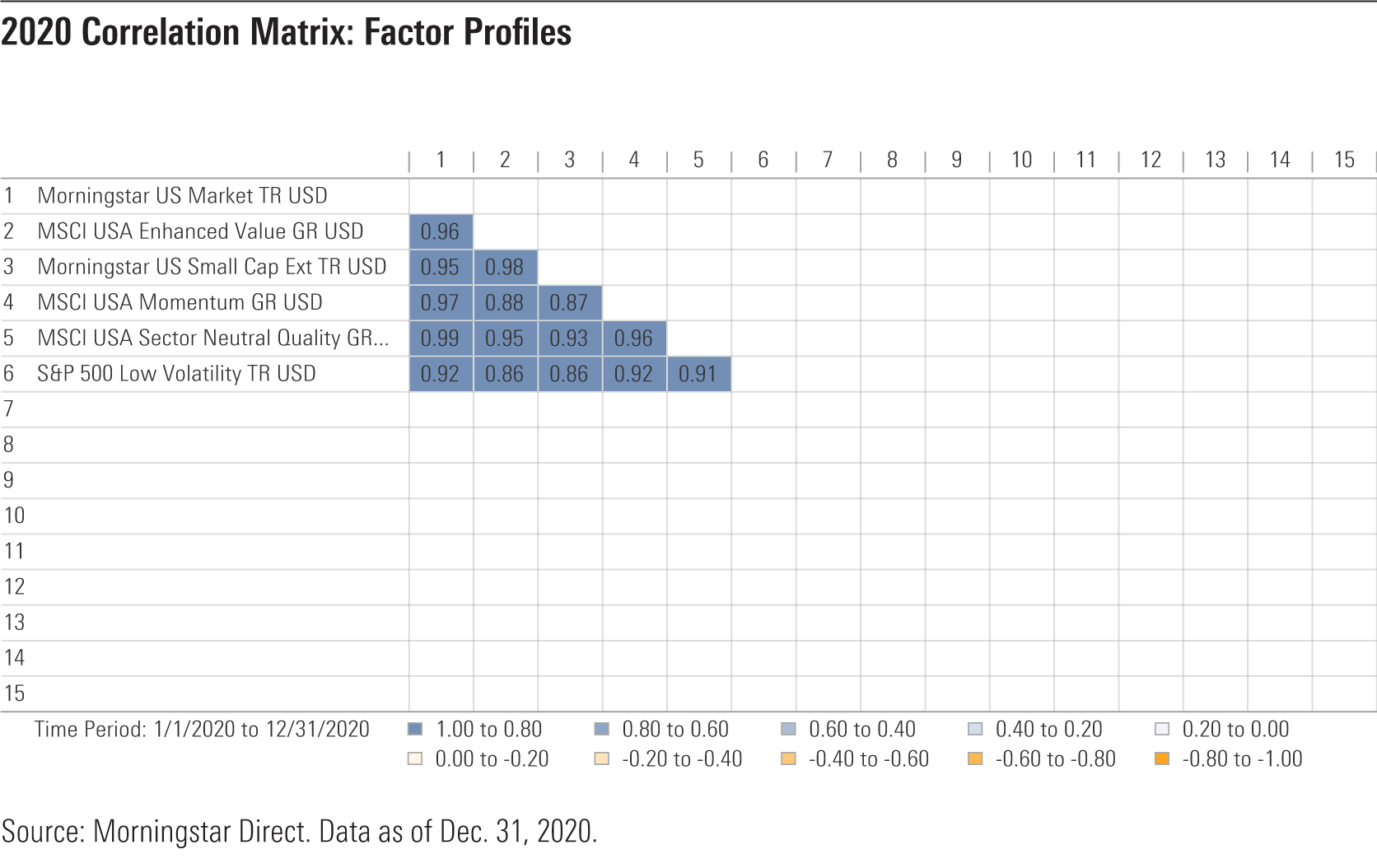

2020 Correlations for Factor Profiles

In early 2020, however, all five of the major factors suffered losses of at least 30%. At the margins, quality and momentum-driven stocks held up slightly better, while small-cap and value-oriented stocks suffered the deepest losses.

Surprisingly, the low-volatility benchmark actually lost more, on average, than the Morningstar US Market Index. Many low-volatility stocks also have higher-than-average dividends, which suffered deep losses during the downturn. The benchmark also fell behind because of its light weighting in technology stocks, which continued to outperform.

For 2020 overall, correlations fell in a fairly narrow range. The quality factor showed the highest correlation with the broader equity market, followed by momentum, value, and small cap. The low-volatility factor, while slightly lower, still showed a correlation of 0.92 with the Morningstar US Market Index.

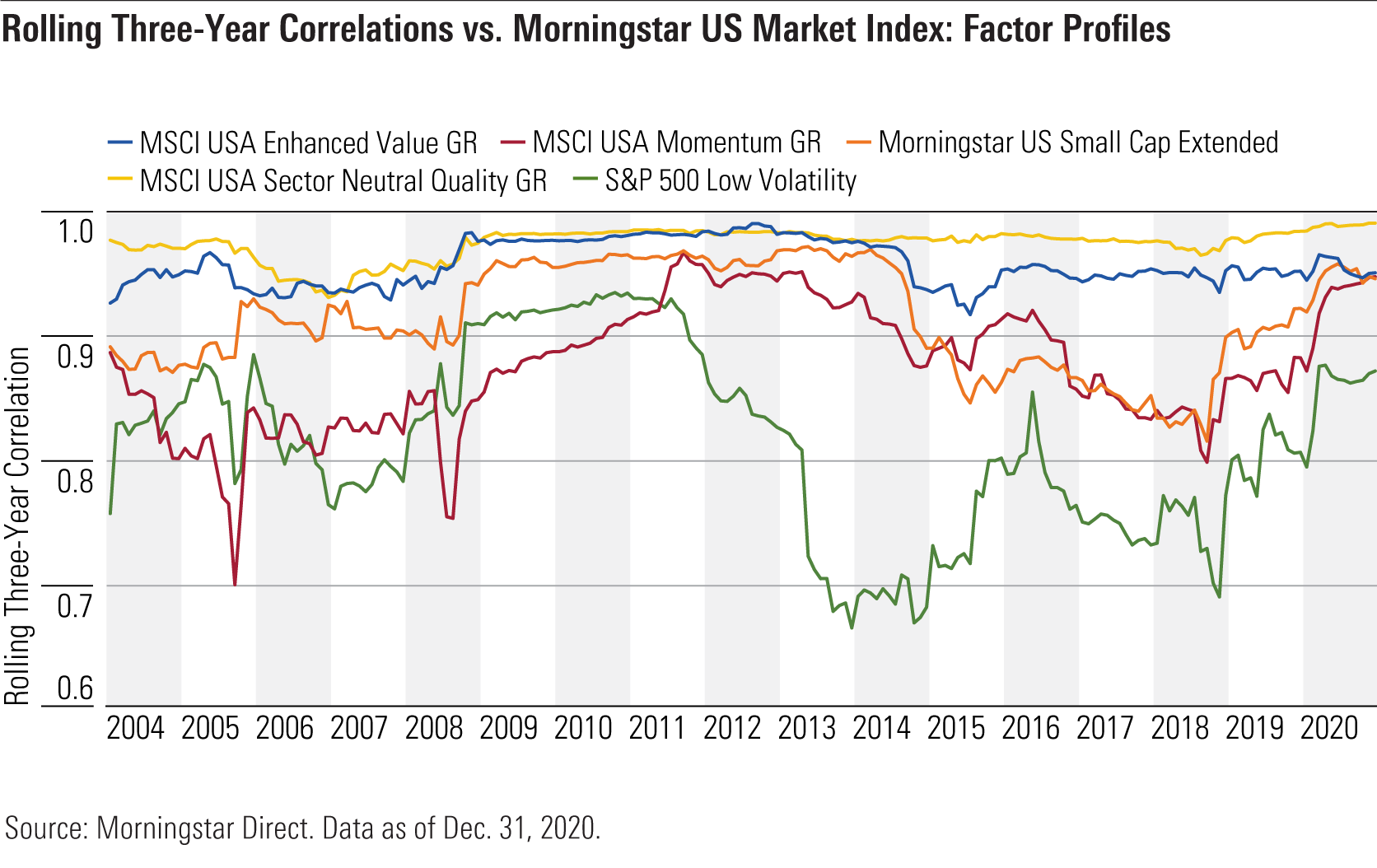

Longer-Term Trends for Factor Profiles

These patterns are generally consistent with patterns shown over longer periods, with quality showing the strongest correlation with the broader equity market and low volatility the weakest correlation. Over time, though, correlations for all five factor indexes have generally trended up, as shown in the graph below. With performance moving more in line with the overall market, correlations between factor profile benchmarks have also converged. Now that factors are so widely studied and embraced by asset managers, one possible cause for this convergence could be that so many investors are following the same factors that their performance has become less and less discrete.

Portfolio Implications

A general upward trend in correlations has reduced the diversification value of factor profiles. However, correlation only measures the direction of returns, not the magnitude. Factor profile indexes can therefore still shed light on differences in performance, and different factors could still show higher or lower returns in different types of markets.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)