What Lower Withdrawal Rates Mean for Retirement Savings

You might need to save a lot more.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

My colleagues Christine Benz, John Rekenthaler, and Jeff Ptak recently did a deep dive into the current state of retirement income.

The upshot: They found that the 4% standard rule of thumb for retirement withdrawals--which assumes retirees use that percentage to set a starting dollar amount for annual portfolio withdrawals and then adjust the withdrawal amount each year for inflation--should probably be considerably lower.

Because of the twin perils of low starting yields on bonds and historically high equity valuations, retirees are unlikely to receive returns that match those of the past. Assuming that future investment returns are lower than in the past, they estimated that the standard rule of thumb should be lowered to 3.3% (for investors holding a balanced portfolio of 50% stocks and 50% bonds. (I came up with a similar number when I wrote about this issue in March 2021.)

Ratcheting down the sustainable withdrawal rate has major implications for retirement savers. On the positive side, investors who are currently close to retirement age have benefited from favorable market tailwinds over the past three to four decades. But younger investors may need to save considerably more to build up enough savings to sustain withdrawals when they eventually retire.

What Lower Withdrawal Rates Mean for Retirement Savings

Because withdrawal rates are based on a percentage of portfolio value, one way to estimate how much retirement savings you might need is to use this percentage to back into a dollar amount for savings needed at retirement.

For example, an investor who estimates she’ll need $40,000 in retirement income would need a portfolio value of $1,000,000 at retirement assuming a withdrawal rate of 4%. (This is $40,000 divided by 4%, or 0.04). Changing the withdrawal rate to 3.3% means she would need a portfolio value of $1,212,121 ($40,000 divided by 3.3%, or 0.033). In other words, she’d need to accumulate about 20% more in retirement savings.

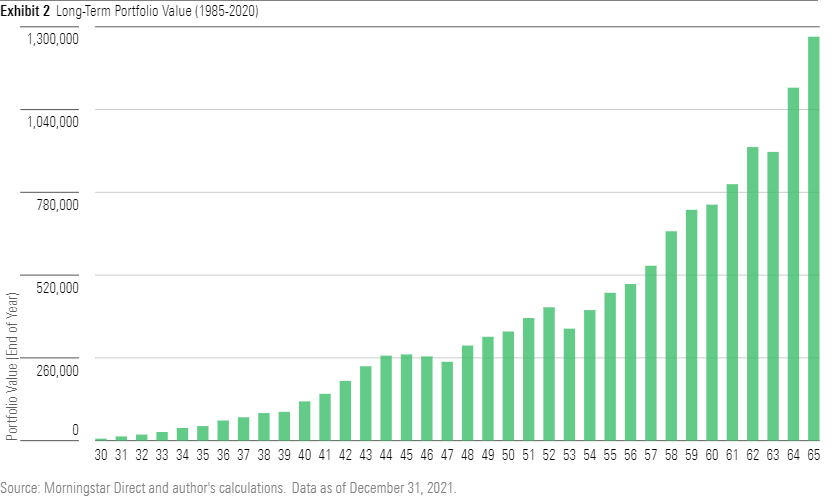

Fortunately, today’s retirees are probably in decent shape thanks to favorable market conditions over the past three or four decades. (In addition, some current retirees still have pension income, which is icing on the cake.) As shown in the exhibit below, an investor who started saving for retirement at age 30 in 1985 could have surpassed the target by simply contributing $5,000 to a retirement plan each year, keeping the assets in a balanced portfolio, and earning annual returns in line with market averages.

Individuals who didn’t start saving for retirement until later in life (or who struggle with income insecurity) might still be running behind, but the long-running bull market has made things easier. Over the past 35 years ended in December 2020, a simple balanced portfolio combining 60% stocks and 40% bonds generated annualized returns of 9.89%--well above the 8.72% long-term historical average since 1926. In addition, the sequence of returns has been pretty benign, as most market downturns (such as 2008, 2018, and early 2020) have been relatively short-lived.

Note:Portfolio values assume $5,000 annual contributions, a balanced portfolio of 60% stocks and 40% bonds, and annual returns in line with each year's market averages.

Younger Investors Face an Uphill Battle

Younger investors who are just getting started with retirement savings face a double set of challenges: First, they need to accumulate more assets, and second, it will be tougher to reach a given savings target if future returns are lower than in the past.

In fact, Morningstar's return assumptions suggest that young adults may need to save roughly twice as much each year as current retirees previously did. (I came up with these numbers by using the savings goal calculator available at www.investor.gov. Note: If you're starting with no retirement balance, you may need to enter $1 in the initial value field to get the calculator to work.)

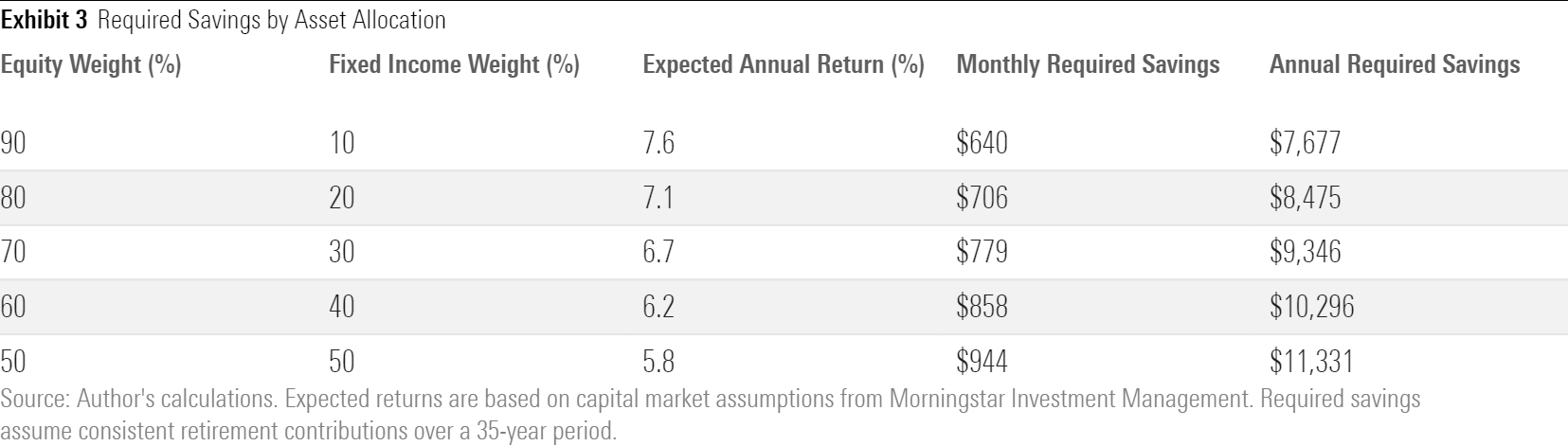

As shown in Exhibit 3, investors willing to take on the risk of a higher equity allocation may be able to save slightly less, but it’s prudent to keep some fixed-income exposure on hand, especially as you get closer to retirement age.

Don’t Panic

The numbers presented above might seem daunting, but there are a few reasons to be more sanguine. For one, retirement withdrawals aren’t set in stone.

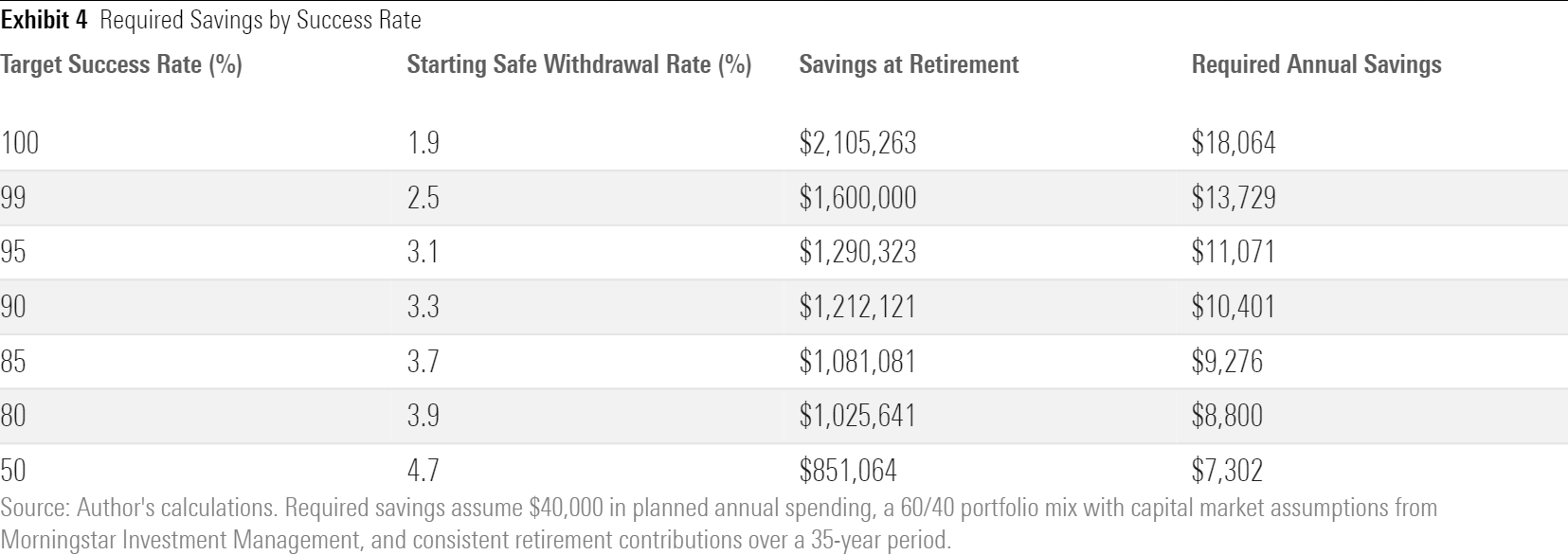

As we’ve detailed in other articles, there are various flexible withdrawal strategies that can significantly increase sustainable withdrawal amounts--and therefore decrease required savings. Some of the major strategies include forgoing the inflation adjustment after any years when your nest egg loses value, employing a “guardrails” strategy that involves cutting back on withdrawals in down markets but giving yourself a raise in good ones, or using required minimum distributions to determine the withdrawal amount. Investors who are willing to tolerate more uncertainty around the odds of success can also afford to save less, as shown in Exhibit 4.

In addition, we’ve written about numerous nonportfolio strategies that can improve the odds of success, such as delaying retirement, cutting back on planned spending, maximizing Social Security and pension payouts, supplementing retirement income by purchasing an annuity, or tapping into income from other sources, such as rental properties or part-time work.

Finally, it’s important to emphasize that our numbers for both sustainable withdrawal rates and required savings amount are based on conservative estimates for future market performance. If the market continues chugging along, retirement savers might find themselves in considerably better shape. In the meantime, though, it’s prudent to save as much as you reasonably can, as well as checking in periodically to see whether your retirement savings are on track.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BZ4OD6RTORCJHCWPWXAQWZ7RQE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)