These Pre-Retirees Look Forward to the Next Chapter

But they worry that their sizable portfolio is more complicated than it needs to be.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

Editor’s Note: This portfolio makeover is from 2021. Keep in mind that the current market environment may be different than when this makeover was executed.

Having established an enviable life together, Conrad and David are happily anticipating the next chapter.

Conrad, a 63-year-old scientist for the federal government, and David, 58, a marketing executive, have established successful careers, but they're looking forward to a less frenetic schedule at some point in the not-too-distant future. Conrad would like to retire at age 66, and David hopes to continue working through his mid-60s.

They've amassed a healthy $4.4 million portfolio, and they'll also have ample pension income. In addition, they own two mortgage-free homes, their primary residence in an East Coast city as well as a vacation home in the desert. With retirement on the horizon, they're looking forward to having more time to pursue travel and relax at their desert oasis.

By any reasonable measure, they're home-free from a financial standpoint. But with success often comes complexity, and Conrad and David worry that their portfolio is more complicated than it needs to be, especially as they get closer to retirement. "I want to simplify our portfolios, which have way too many moving parts," Conrad wrote.

As is so often the case with dual-earner couples, they currently have several separate accounts with many holdings apiece--eight separate accounts and 50 underlying holdings in all. "We are concerned with portfolio investment overlap and that our portfolios are overly complicated, which will make it difficult to determine how to draw them down in retirement."

Additionally, Conrad is five years older than his partner and wants to ensure that their money lasts for both of their lifetimes. "I want to make certain that we will have enough income to support us in our retirements, especially with concerns over rising healthcare and housing costs," Conrad wrote. While the couple's two homes are paid off, they entail substantial annual carrying costs: $40,000 on the city property and another $13,000 on the desert condo. Conrad has long-term care insurance through his work--a terrific perk--but it only covers two years' worth of care and only for him.

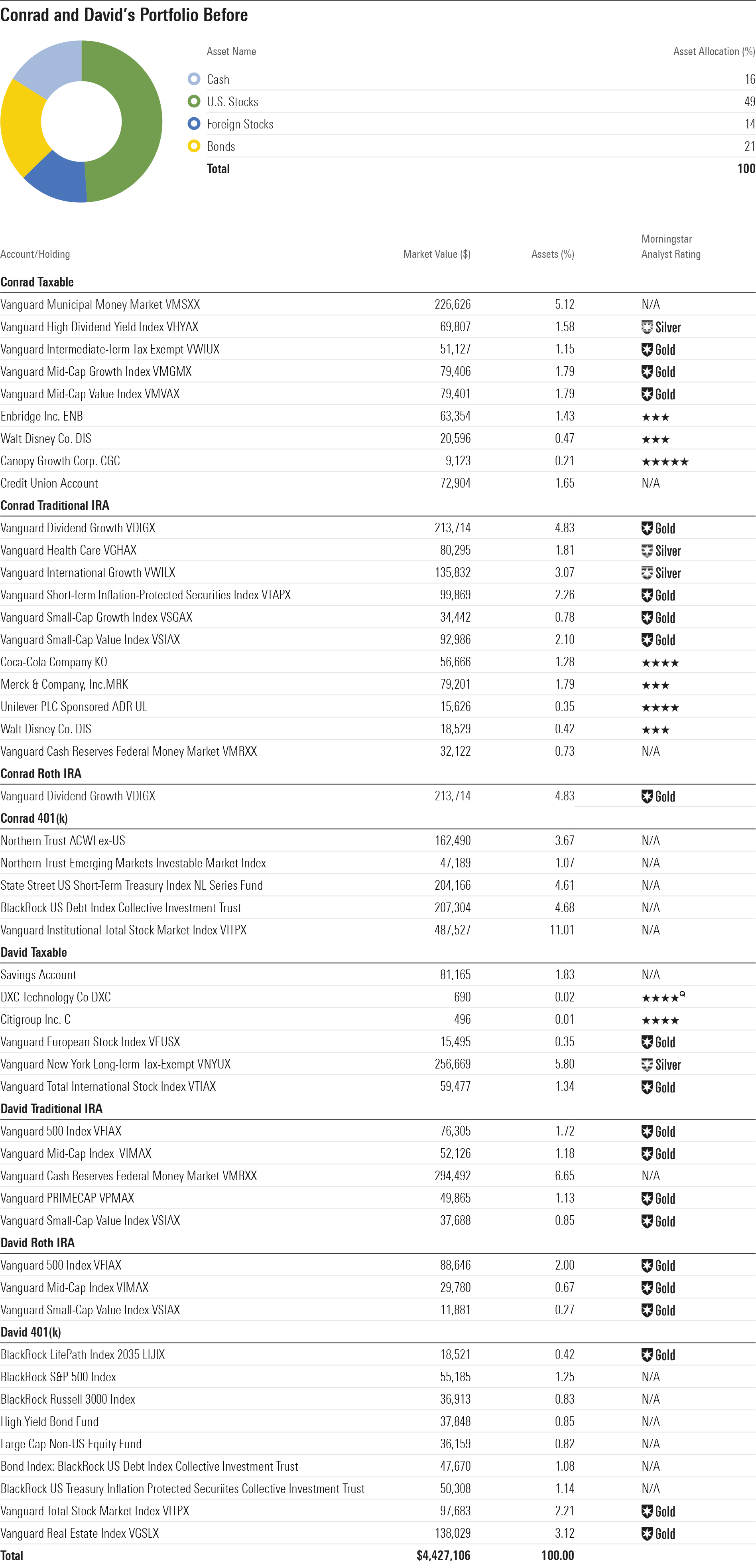

The Before Portfolio

Conrad and David's holdings are arrayed across eight separate accounts; each of them has a 401(k), traditional and Roth IRA, and taxable account. Overall, the couple's asset allocation is fairly balanced, with 62% equity, 22% bonds, and 16% cash, per Morningstar's X-Ray feature. The portfolio's equity investment-style exposure is nicely dispersed across the Morningstar Style Box, with the largest concentration of assets (25%) in the large-growth square. Their holdings are generally quite highly rated; Morningstar Analyst Ratings of Gold and Silver dominate their mutual fund holdings.

Conrad's 401(k) is the largest silo: While he's an employee of the federal government, his agency isn't covered by the Thrift Savings Plan for government workers. His 401(k) holdings are low-cost collective trusts and mutual funds from Vanguard, BlackRock, and Northern Trust. (Collective investment trusts are like mutual funds, but often feature lower fees because they're not subject to the same reporting requirements as mutual funds. They’re becoming increasingly popular in 401(k) plans.) Conrad's traditional IRA is the next largest account; it consists of index funds and a smattering of blue-chip stocks. His taxable account holds individual stocks, some tax-efficient fixed income and cash holdings, and a high-dividend-yielding equity fund. Conrad's Roth IRA account is his smallest asset pool and holds just a single fund, Vanguard Dividend Growth VDIGX.

In addition to his investments, Conrad has a pension that will provide $75,000, adjusted for inflation, per year throughout both his and David's lifetimes. (Conrad opted for a reduced pension benefit to cover his partner's life as well as his own.) He is also currently receiving about $15,000 in annual income from pensions from previous employers, and he is sensibly investing those funds into Vanguard Intermediate Tax-Exempt VWITX in his taxable account. He plans to rely on those assets early on in his retirement so that he can delay Social Security filing until age 70. As with his federal pension, Conrad opted for a reduced benefit from the smaller pensions so that they'll provide income for David's lifetime as well as his own.

David's 401(k), his largest account, features collective investment trusts, mainly from BlackRock and Vanguard. Index funds and cash dominate David's traditional and Roth IRAs and his taxable account, though he also owns a smattering of individual stocks and actively managed funds, including Vanguard Primecap VPMCX. David also has a pension through his employer, but it was frozen about 20 years ago, meaning that no new contributions have been going in. At retirement, he'll be able to take a lump sum of about $42,000 or a payout of $221 per month.

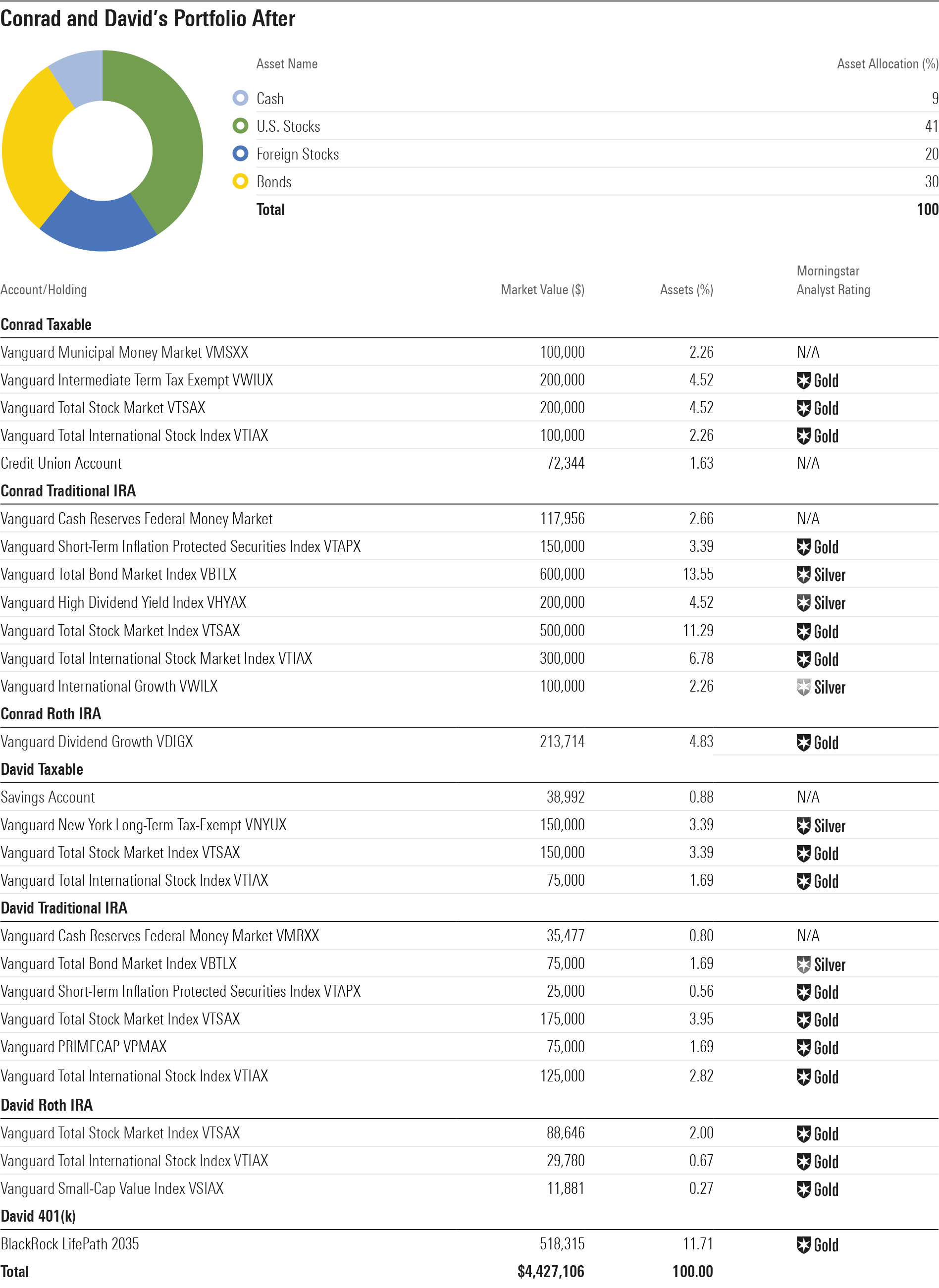

The After Portfolio

Conrad and David have done a lot of preliminary work on the viability of their retirement plan, and it appears that they're in good shape overall from the standpoint of not outliving their assets. They expect to need $130,000 in total annually in retirement. Meanwhile, Conrad's pension and income from Social Security will provide $160,000 in annual income, assuming that Conrad starts Social Security at age 70 and David files immediately after retirement at age 67.

With any plan, however, it's worth thinking through the potential risk factors. For example, David notes that ageism is rampant in his industry: While he'd like to work until age 67, there's a possibility he may not be able to do so. An early retirement for David would necessitate tapping their portfolios more aggressively in those years order to facilitate his plans to delay Social Security filing. Conrad will also need to spend from his assets in the early years of his own retirement, before he files for Social Security at age 70. Once the pensions and Social Security for both of them kick in, they should be able to scale back on the portfolio spending.

If anything, their portfolio is a bit conservative given that they're unlikely to place meaningful demands on it anytime soon. Their cash holdings, at 16% of assets, seem particularly high given that portfolio spending isn't imminent. With inflation ticking up, the opportunity cost of cash is higher than it was even a year ago. My After Portfolio reduces cash to about 10% of assets.

Their non-U.S. exposure is on the low side, so my After Portfolio bumps up that weighting. I targeted a 2:1 ratio of U.S. equity relative to non-U.S.

I also took a few steps to simplify and reduce portfolio sprawl. Because Conrad is older than age 59.5, he can roll over his 401(k) assets to his traditional IRA, which will give him a single tax-deferred account for retirement. Given the size of their overall portfolio, the small individual-stock positions weren't making much of a difference in performance. My After Portfolio includes funds only, with an emphasis on index funds to reduce oversight and facilitate easy rebalancing among the major asset classes. Those changes are easily enough enacted within their tax-deferred accounts, though they'll want to be careful about making changes and realizing gains in their taxable accounts, especially right now, in their peak earnings years and with the market near an all-time high.

In the interest of reducing complexity and improving tax efficiency, I swapped in total market index funds for the equity exposure in Conrad's taxable portfolio. I relocated the excellent but tax-inefficient Vanguard High Yield Index VHYAX to his traditional IRA. Within David's 401(k), I supplanted the several distinct holdings with a single target-date fund that was already in his portfolio, Gold-rated BlackRock LifePath Index 2035 LIJIX. With just 0.14% in annual operating expenses, the fund provides inexpensive diversification across the major asset classes, as well as built-in oversight on asset allocation.

Conrad and David are also entering a good life stage to do some tax planning, to help reduce required minimum distributions and related tax bills once each of them passes the age 72 threshold. Conrad has roughly $2 million in RMD-subject accounts, and David has another $1 million-plus. The early years of Conrad's retirement, especially, may provide the opportunity to convert some of their traditional IRA and 401(k) assets to Roth IRAs and/or spend from their traditional IRAs when they're in a relatively low tax bracket relative to their working or later-retirement years. Doing so would lessen the tax bills that will eventually be due on those assets.

To help give them maximum flexibility to draw upon their taxable or tax-deferred portfolios as their tax situation dictates in the early years of retirement, I retained exposure to bond and cash assets in their taxable and tax-deferred accounts. I left their Roth IRAs equity-heavy, figuring those will be last in their distribution queue. Conrad and David will also be ideal candidates to make annual charitable gifts via qualified charitable distributions once they hit age 70.5.

The couple appears to be reasonably well protected from the standpoint of long-term care. While Conrad's long-term-care policy would only provide for his own care, should he need it, the couple's investment portfolio is sufficient to cover out-of-pocket long-term-care expenses that might arise. That's especially true given their modest rate of spending.

Conrad notes that he and David haven't married but have contemplated doing so, in part so that David can be covered by Conrad's health insurance in retirement. I like the idea of them engaging a financial planner or estate-planning attorney who specializes in planning for same-sex couples, to help think through the pros and cons of tying the knot. The National Association of Personal Financial Advisors' website includes a screening tool for fee-only financial advisors' specialties, including planning for LGBTQ couples.

Editor’s note: Names and other potentially identifying details in portfolio makeovers have been changed to protect the investors’ privacy. Makeovers are not intended to be individualized investment advice, but rather to illustrate possible portfolio strategies for investors to consider in the full context of their own financial situations.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WDFTRL6URNGHXPS3HJKPTTEHHU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)