Why Buffer Funds Aren’t a Perfect Fix

Despite their complexity, buffer funds have generally performed according to plan.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

Buffer funds--which promise to limit downside losses from equity-market exposure while capping upside returns--have grown increasingly popular. By my count, there are now roughly 80 exchange-traded funds plus a handful of open-end mutual funds following this approach. [1] Since the first buffer products appeared on the scene in 2016, assets have grown to more than $5.2 billion.

These funds typically invest in a broad market index along with a standard options collar to limit downside risk. The idea is to provide a shock absorber against a certain level of market losses over a defined outcome period (typically one year). The collar strategy involves selling call options (which limits upside returns) and using the proceeds to buy put options (which limits downside risk). Some of the more established ETFs, such as the Innovator Power Buffer series, have downside buffers ranging from 9% to 30%. In down markets, shareholders are only exposed to losses that exceed the buffer. Upside caps vary depending on the issue date and generally increase along with market volatility.

In this article, I’ll dig into how these funds have performed so far and discuss the role they could play in a portfolio.

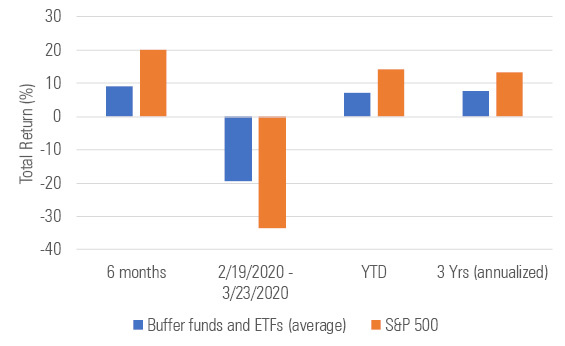

Initial Results This is a new area, so most funds don't have long track records. So far, though, buffer funds have largely performed as expected. As shown in the table below, they've sacrificed some returns in up markets while cushioning returns on the downside. When the market dropped in February and March, for example, the average buffer fund dropped about 19.8%, compared with a 33.5% loss for the S&P 500. As the market has rebounded over the past six months, buffer funds have gained about 9.3%, versus close to a 20% run-up for the benchmark.

Exhibit 1: Buffer-Fund Performance

- source: Morningstar Direct. Data as of 11/30/2020.

However, while these funds promise to limit losses in down markets, they still court some downside risk. As mentioned above, buffer funds seek to protect investors from a certain level of losses, but shareholders are still exposed to drawdowns beyond that point. During the coronavirus-driven downturn from Feb. 19 through March 23, 2020, losses on these funds ranged from about 11% to 27%.

The details behind how the buffers work are complicated. Because the buffer only applies to a specific outcome period, shareholders could still suffer losses over shorter periods. Buffer terms also vary by fund. While most funds are designed to cushion against all losses between zero and the buffer level, for example, Innovator S&P 500 Ultra Buffer ETF UAPR was designed with a buffer that only kicked in after the first 5% of losses (buffering losses between negative 5% and negative 35%). Shareholders who held the ETF for the one-year period ended March 31, 2020, therefore still lost 5.77% net of expenses.

Return Trade-Offs Another drawback inherent in buffer funds is their asymmetrical return profile. Innovator S&P 500 Power Buffer PSEP is a case in point. With about $360 million in assets, it's one of the largest funds in the group and has a fairly typical structure. Investors are protected against the first 15% of market losses, but upside returns are capped at 11.75%. That means shareholders who hold for the full one-year outcome period could lose as much as 85% of their initial investment but can only gain up to 11.75%.

This trade-off might be appealing for investors who are wary of losing money, but it’s fundamentally at odds with how markets generally perform. Statistically speaking, markets tend to generate positive returns more often than not. Therefore, buffer-fund shareholders are more likely to sacrifice upside returns than benefit from downside protection.

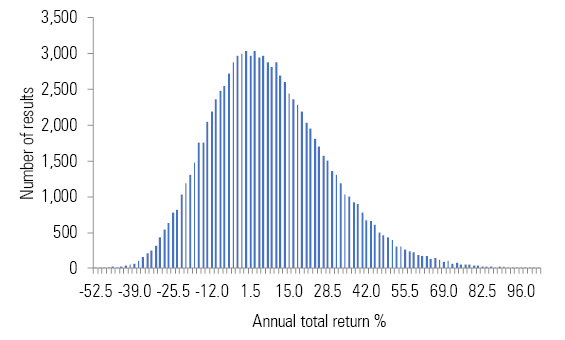

My colleague Maciej Kowara ran some numbers to illustrate this point. He started with actual data for the S&P 500’s annual price returns between 1929 and 2019 to estimate mean returns and standard deviations, and then randomly generated 100,000 potential return paths. This mathematical technique--also known as a Monte Carlo analysis--generates multiple scenarios with the goal of estimating the probabilities of different outcomes. He then summed the payouts and looked at the frequency of how often each total appeared as a result. The histogram of the results, which represents the distribution of the results from the 100,000 different scenarios in the simulation, is shown below.

Exhibit 2: Distribution of Potential Annual Returns

- source: Morningstar Analysts

Because this simulation assumes a log-normal distribution, it’s not surprising that the results cluster around the middle. About 49% of the return paths land between the lower limit of negative 15.0% (buffer) and the upper limit of 11.75% (cap). So strictly from a statistical perspective, the most likely outcome is that the buffered ETF structure would provide neither a benefit (in the form of limited losses) or a cost (in the form of limited upside returns). The second most-likely outcome, with 38% of the results, is that returns land above 11.75%, which would result in shareholders foregoing some positive returns. The odds that returns land below zero but above the downside buffer, meaning shareholders would be fully protected from losses, are about 26%. In a minority of paths (13%), returns landed below the negative 15% buffer. In that case, shareholders would have partial protection from losses, but only up to the buffer level.

This distribution of returns means the average expected return for the buffered ETF is only 4.8%, compared with 7.5% for unbuffered exposure to the S&P 500 Price index. In other words, shareholders are likely to give up nearly 3 percentage points of annual returns, on average, even before fees and expenses. What’s more, both expected return numbers trail the long-term average return for stocks, which highlights another drawback of buffer funds’ structure. Because they’re most often linked to a price index, they don’t benefit from dividend yields, which have historically made up a significant portion of equity-market returns.

Is there Still a Rationale? Buffer-fund defenders would probably argue that Monte Carlo or no Monte Carlo, these funds aren't geared toward investors who expect the market to perform in line with longer-term trends. Indeed, they often describe these products as best used by investors who realize they need to have some equity market exposure but fear the market could drop over a certain period, typically the next year. There are at least two problems with this argument: 1) someone expecting the market to go down shouldn't be investing in stocks to begin with, and 2) it's impossible to predict market performance over any period.

Despite these flaws, the buffer-fund structure could still be a helpful antidote for some of the most common behavioral traits often shown by investors. Behavioral science researchers have found that investors have an outsize negative response to losses; people tend to experience about twice as much psychological pain from a loss as they do pleasure from an equivalent gain. This common characteristic--also known as loss aversion--can cause investors to fear equity exposure, even if it might be in their own long-term best interest.

Researchers have also found that human beings are acutely uncomfortable with uncertainty; this aversion to uncertainty can often affect investment decisions. By removing part of the uncertainty inherent in investing, buffered products may make it easier for beginning investors to take initial steps into the market.

Buffered funds also stack up well against other defined-outcome offerings, namely structured notes, which are bank-issued securities that often include some level of downside protection. Like structured notes, buffered funds cater to reluctant investors who fear downside losses. But as registered investment companies, buffered funds are far more liquid and transparent. And in contrast to structured notes, which are senior unsecured debt obligations of the issuing bank, buffered funds don’t court any credit risk.

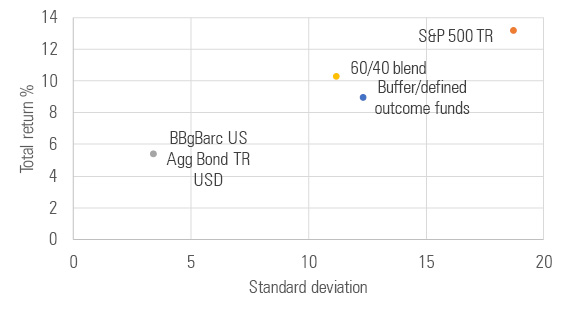

They’ve also offered a decent, if not stellar, risk/return profile. There are only a handful of funds with three-year records, but those funds have generated lower returns than broad equity-market benchmarks, while keeping volatility (as measured by standard deviation) significantly lower. Overall, though, risk-adjusted returns have lagged a bit behind a simple 60/40 blend of stocks and bonds.

Exhibit 3: Trailing Three-Year Risk/Return Profile for Buffer Funds versus Other Benchmarks

- source: Morningstar Direct. Data as of 11/30/2020.

While they're less expensive than structured notes, which often come with large embedded fees, most buffered funds and ETFs aren’t exactly cheap, either. The average expense ratio is about 0.87%, which seems pricey for a product that's essentially an index fund with an option overlay. (Granted, options can be complex and intimidating for many investors, making it less likely that most DIY investors would want to replicate these products on their own.)

Conclusion Despite their complexity and other drawbacks, buffer funds have generally performed according to plan and kept risk in check. They could be viewed as catering to investors' own worst traits, but it's a fairly innocuous behavioral crutch. It's sort of like buying snack-size packages of cookies or chips: maybe not optimal from a nutritional perspective, but potentially helpful if it helps a person avoid overeating and stick to her diet. Similarly, buffered funds could be helpful for investors who might otherwise avoid equity funds entirely or bail out at the first sign of losses.

[1] For the purpose of this article, the buffer funds group includes funds that quantify downside protection and excludes funds with more general downside protection mandates, such as bear market, limited volatility, long-short equity, and other options-based offerings.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)