What Investors Should Do After the Fed Meeting

As stocks and bonds continue to slide, the Fed’s fight against inflation means investors need to keep their seat belts buckled.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

Fresh losses in the stock and bond markets following this week’s Federal Reserve meeting make one thing clear for investors: Be prepared for still more turbulence ahead.

The central bank this week raised the federal-funds rate by 0.75% for an unprecedented third-straight meeting, taking the funds rate target to 3.0% to 3.25%. At the same time, Fed officials indicated they expect continued rate increases that could take this key short-term rate to 4.6% next year. (Stay updated with our look at the November Fed meeting.)

In addition, while it sometimes can be difficult for investors to interpret what Fed officials mean, the message was clear when Chairman Jerome Powell spoke following the decision to again aggressively raise interest rates: The Fed will do what it takes to get inflation down from 40-year highs. And to do that will mean slowing down the economy.

“We have got to get inflation behind us. I wish there were a painless way to do that, there isn't,” Powell said. That pain, he said, includes higher rates, slower growth, and a weaker jobs market.

And while Powell didn’t say it directly, that increasingly is expected to include a recession, not just a so-called soft-landing where the economy cools off but doesn’t shrink.

“As an investor it’s not an easy message to hear,” says Chris Konstantinos, chief investment strategist at the RiverFront Investment Group.

Here are six takeaways for investors:

Rates Will Keep Rising

There clearest takeaway from the Fed meeting is that short-term interest rates will continue to rise, and they will keep raising rates until officials are comfortable with the idea that inflation has really turned the corner and is heading lower.

“The Fed has been surprisingly clear about the direction it’s going to take,” says Jason Trennert, chief investment strategist at Strategas Research Partners. While the Fed officially has a dual mandate of delivering maximum sustainable employment and stable prices, “for all intents and purposes, the Fed has only one mandate right now and that’s price stability.”

Currently, the Fed’s projections suggest that the federal-funds rate will rise by another percentage point by the end of the year, an exceptionally fast pace for rate increases by historic standards.

In a bit of a twist, the fact that the economy has remained as healthy as its been— especially the job market—may mean the Fed will feel more comfortable staying on an aggressive rate hike path. In addition, the fact the rates have been lifted as much as they have means that when it comes time to lower rates, there is also plenty of room to bring them down, says Matt Freund, head of fixed income strategies and co-chief investment officer at Calamos Investments.

“The Fed generally believes they have room to tighten without lasting damage,” he says. Freund adds that he believes the Fed will be able to slow down its rate hikes as we move into next year.

A Recession Is Looking More Likely

It’s not just Powell’s comments that have market watchers looking for a more meaningful economic slowdown. The warning signs in the markets and the economy are increasingly flashing yellow about the potential for an economic downturn. (Technically, gross domestic product growth has already been negative for two quarters, which is generally seen as a recession.)

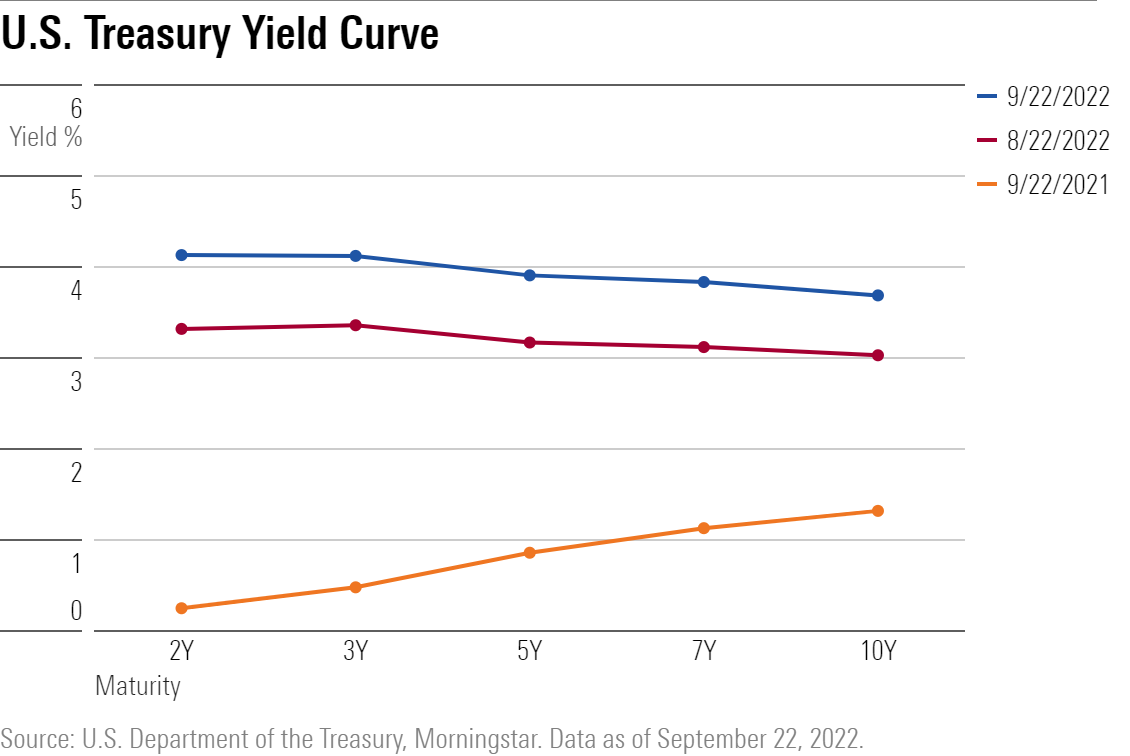

In the bond market, short-term interest rates are now meaningfully above long-term interest rates , which is known as an inverted yield curve, and is historically a strong indicator a recession is coming.

In the wake of the Fed meeting, “We’ve seen further inversion, which suggests that the probability of a hard landing is increasing,” says RiverFront’s Konstantinos.

Morningstar

In the real economy, data is accumulating that a slowdown is building. Richard Weiss, chief investment officer for multi-asset strategies at American Century Investments, notes that manufacturing surveys are almost uniformly pointing to a contraction, and now evidence is growing of a slowdown in the housing market.

“It’s becoming more apparent now that this thing ain’t getting better in the near term, it’s getting worse,” he says.

Keep an Eye on the Earnings Outlook

While fears of a recession have been building for months, the stock market has been supported by continued strong corporate earnings. The question is at what point will earnings roll over and turn negative.

“People have been taking down their expectations down for earnings growth,” says Strategas’ Trennert, but not yet factoring in a decline. “We’ve never had a recession without earnings being down.” In the average recession, he says, earnings fall 30% and the median decline is 22%.

The tricky aspect of this for investors is that in a matter of weeks, third-quarter corporate earnings will come out. However, they’ll largely reflect an economy with continued strong consumer spending and a strong job market, albeit with the continued pinch from inflation.

That will likely mean an even greater-than-usual focus on what companies have to say about the outlook. Weiss says investors should be braced for bad news.

“I think we will be seeing many in the C-suite talk about layoffs and the forward (earnings) guidance becoming a lot more pessimistic,” he says. “If we want to get together in three to six months and place a gentlemen’s bet, I think earnings will have a negative in front of them.”

A caveat is that inflation lifts corporate earnings in nominal terms and could offset some of the downward pressure from an economic slowdown. “It’s not a done deal that earnings are going to collapse even if the economy gets slower,” says RiverFront’s Konstantinos.

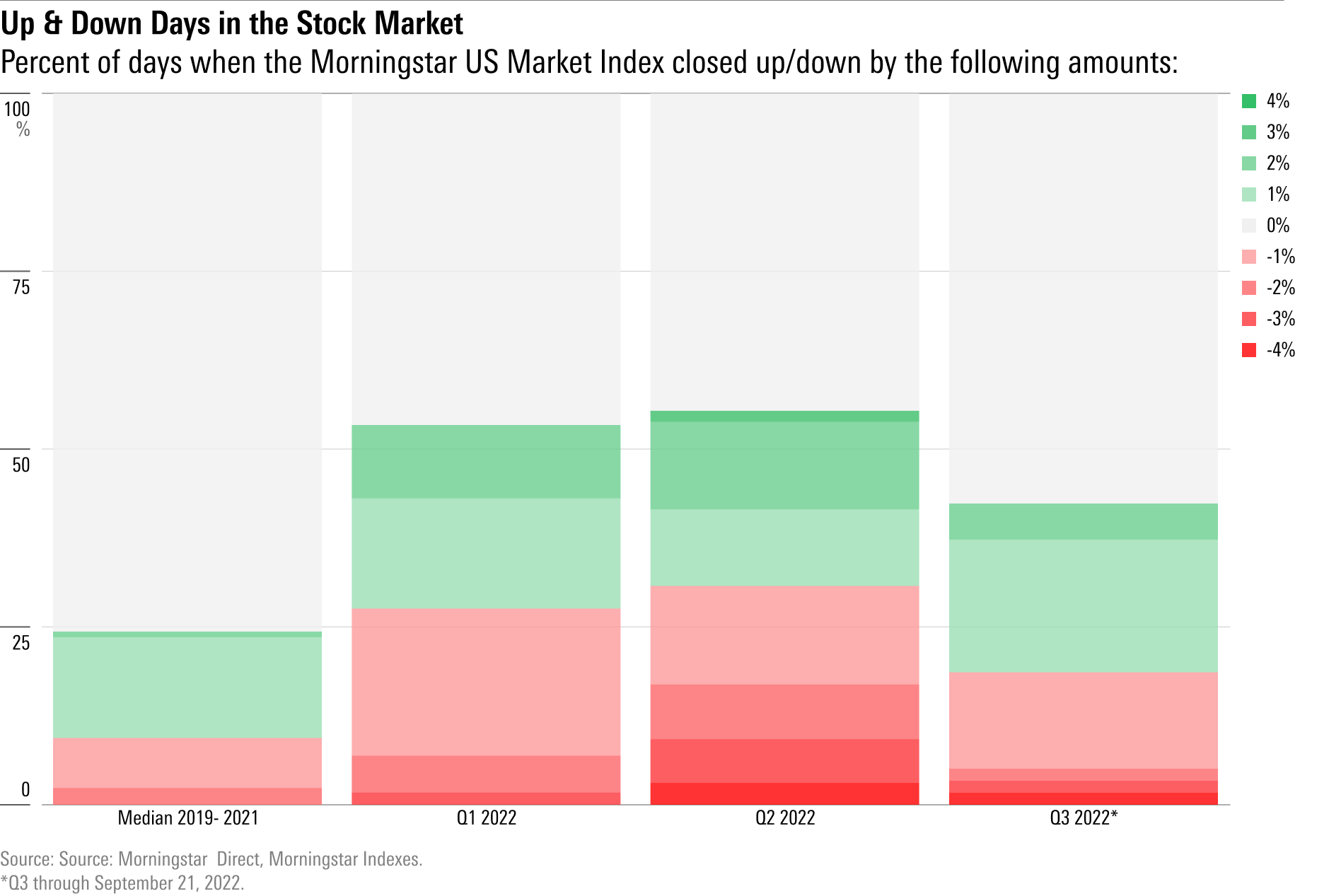

Uncertainty Will Mean Volatility

The stock market has already been volatile this year thanks to the ripples from the Fed rate hikes and uncertainty about the inflation outlook and policy response.

Following the Fed meeting, Konstantinos says investors should be braced for continued back-and-forth swings in the stock market.

“I think the market is going to be rangebound and pretty volatile for the next couple of months,” he says. While that can make for more rallies such as the one seen this summer, “the equity market will have a hard time making progress higher.”

In that environment, Trennert notes investors should remember the tendency for the market to stage very strong bear market rallies but remain in a downtrend. During the dot.com bubble collapse from 2000 through 2002, there were eight significant rallies, he says. “The last rally was 44% and after that the market fell for another year,” Trennert says.

“This is going to be very difficult for the market,” he says.

Morningstar

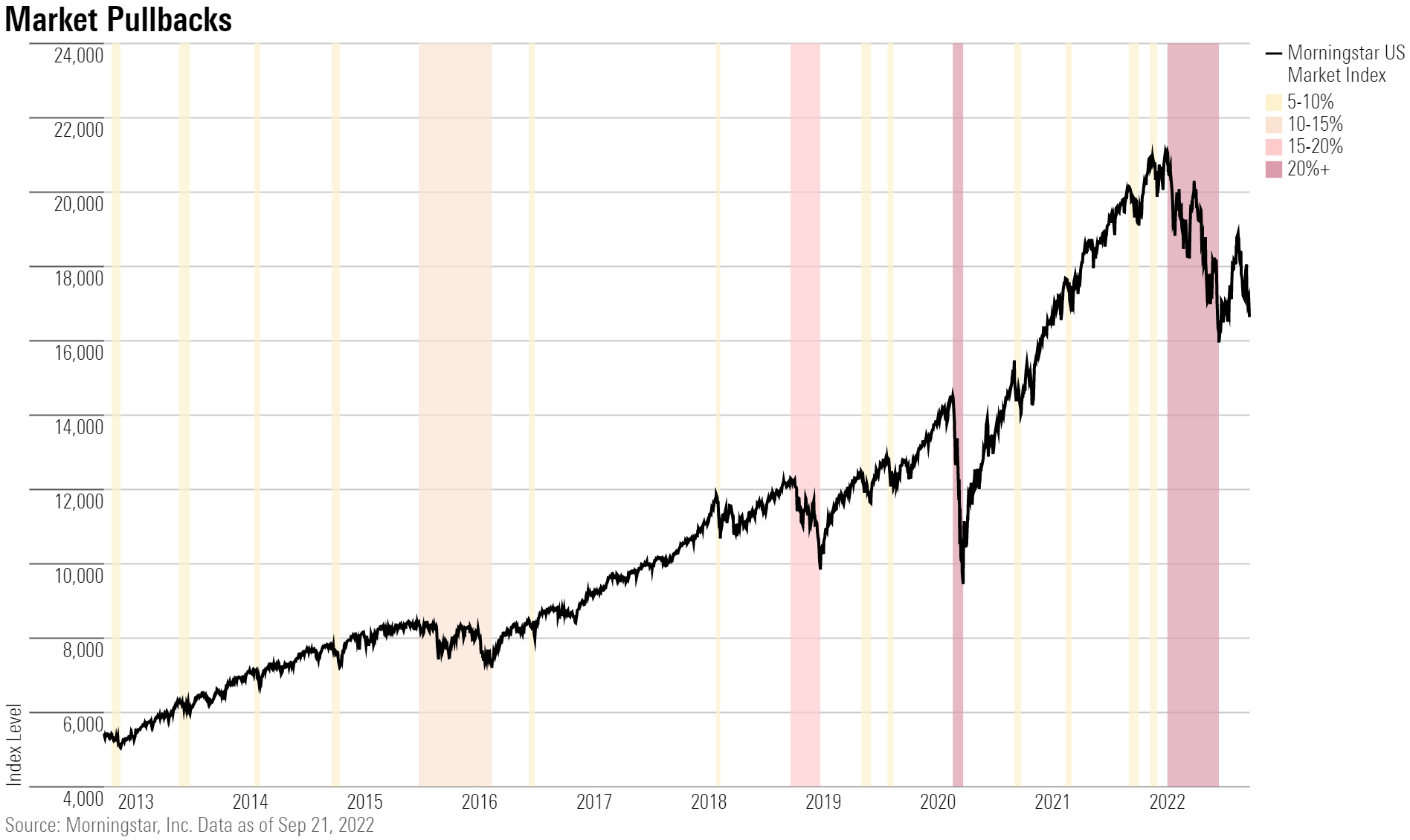

Forget About a `V-Shaped' Bounce

During the pandemic-driven bear market, stock investors were in essence bailed out by the Fed’s extremely aggressive efforts to support the economy through the financial markets. A quick bounce back in the markets is often referred to a “V-shaped” recovery because of how it looks on a chart.

“This is not a pandemic that cold-cocks the economy and we have a V-shaped rebound,” says American Century’s Weiss. That’s unfamiliar territory for many investors. “A lot of investors have joined the markets after the 2008 financial crisis and only seen V-shaped recoveries” in the markets, he says.

Traders will often refer to “The Fed Put” which takes a term from the options market to say that the Fed will come in at the bottom and effectively buy financial assets.

But with the Fed in a determined tightening mode, “there is no Fed Put,” says Trennert. “People have been very conditioned that everything is V-shaped, but most of the time it doesn’t happen.”

Morningstar

It Will Pay to Stay Defensive

Against this backdrop investors should be braced for difficult markets.

“We are cautious,” says RiverFront’s Konstantinos. Overall, they are neutral to slightly underweight weightings of stocks, but are more focused on generating yield in a portfolio in the current market environment. He points to the difficult stock market of the 1970s, as an example of how to be positioned. “A lot of your returns in the market came from dividend yields.’’

At Strategas, Trennert says they’re favoring traditional defensive sectors such healthcare and consumer staples, but also, unique to this economic cycle, energy stocks. “Normally you would want to be out of energy stocks in a recession, because when the economy goes down so do energy prices,” he says. However, with a shift toward clean energy limiting the desire of energy companies to pump more oil despite high prices, that should limit a recessionary drop in oil prices, Trennert says. “We have a feeling energy companies will be distributing a lot of cash to shareholders and dividend yields will stay robust.”

American Century’s Weiss says his team has been defensive since the start of the year, favoring value over growth, along with defensive stocks. “We’re staying there,” he says. “It’s gonna be rough.”

Correction (Sept. 23): An earlier version of this story misspelled the name of Richard Weiss, chief investment officer for multi-asset strategies at American Century Investments.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)