January CPI Report Shows Sticky Inflation Is Back

With new data showing inflation has been stronger than previously reported, the Fed is seen keeping rates higher, longer.

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

After months of good news in the fight against inflation, the January Consumer Price Index report showed that progress in bringing inflation down is moving slower than many in the markets had been thinking was the case.

While the trend toward lower inflation appears to be still on track, it’s not just the direction of inflation that matters to the outlook for the economy, markets, and Federal Reserve policy but also the levels. With the January CPI report, inflation remains well above the Fed target and the pace of declines in the inflation has slowed significantly.

For investors, stickier inflation means interest rates potentially staying higher for longer. That’s especially the case with other economic data, such as the most recent jobs report, showing the overall pace of growth remains healthier than had been expected and few clear signs of an imminent recession. A strong economy could make it harder for the Fed to bring inflation down toward its 2% target rate, necessitating a more hawkish interest-rate policy.

The January CPI report is potentially tough news for both the bond and stock markets, which increasingly had been betting that the Fed would soon stop raising interest rates and beginning lowering them well before the end of 2023. Investors have been looking for rate cuts even as Federal Reserve Chair Jerome Powell has repeatedly said the Fed is not yet thinking about easing monetary policy.

In the wake of the January CPI report, bond markets once again shifted the outlook for Federal Reserve policy, with the Fed now seen holding the federal-funds rate at a higher level until later this year and only making a small cut to interest rates by the end of 2023.

“Another rate hike of 0.25 percentage points in March now looks almost assured, although this is as much because of the strong jobs report as today’s inflation data,” says Preston Caldwell, chief U.S. economist at Morningstar.

In addition, much of the attention hasn’t been on the January CPI report itself but on the picture painted by routine revisions to 2022′s inflation data. The new data shows that inflation hasn’t been falling as fast as the original reports had suggested.

“Although new data shows a lesser decline in core inflation at the end of 2022 than previously thought, we shouldn’t be overly discouraged,” Caldwell says. “Core inflation is still trending down, and we expect that to continue throughout 2023.”

A Largely As-Expected January CPI Report

The January CPI report itself came in fairly close to consensus forecasts, but it’s the more recent trend and the details under the hood that are attracting attention.

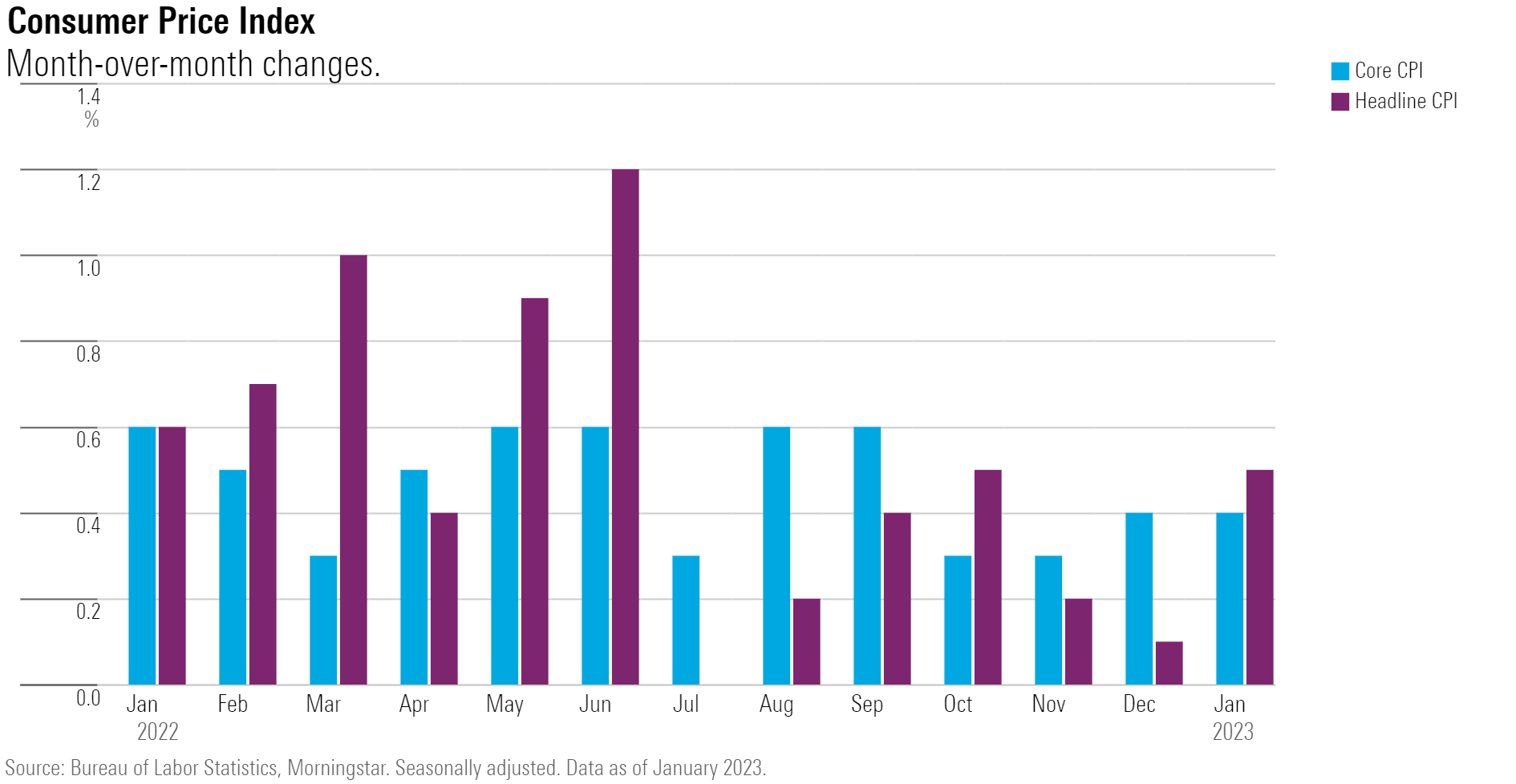

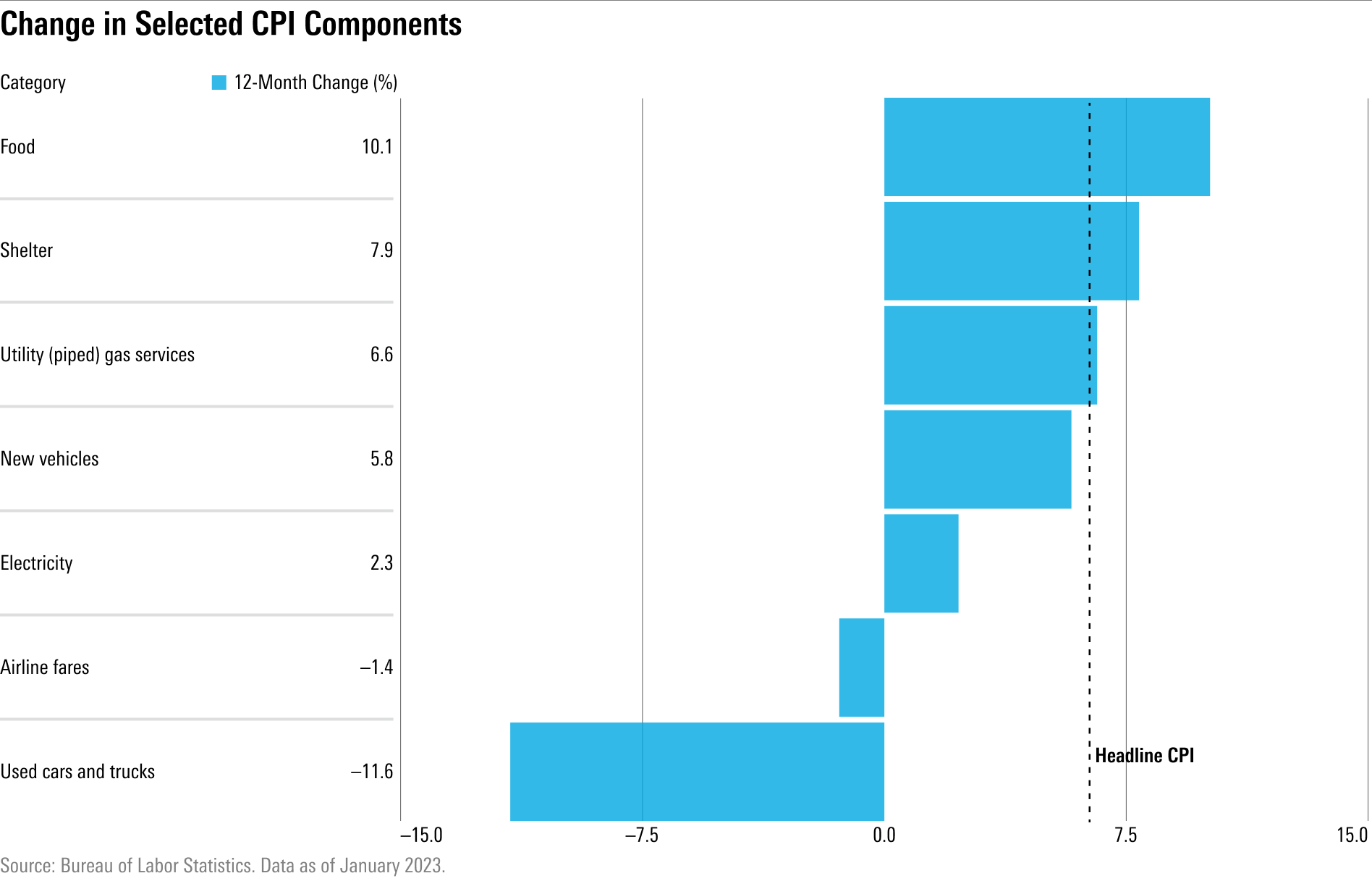

The Bureau of Labor Statistics reported an overall rise of 0.5% in the Consumer Price Index for January, in line with consensus estimates, for its fastest month-over-month reading since October 2022. The increase in the inflation rate was mainly led by a rise in shelter prices, which contributed nearly half of the overall increase in consumer prices. Food, gasoline, and natural gas prices also contributed to the increase.

Core CPI, which excludes the volatile food and energy components, rose 0.4% in January, also in line with forecasts. Drivers of the increase in core inflation in January included shelter, motor vehicle insurance, and apparel.

January CPI Report Key Stats

- CPI rose 0.5% for the month versus 0.1% in December, in line with expectations.

- Core CPI (excluding food and energy) rose 0.4% for the month after rising 0.4% in December, in line with forecasts.

- CPI, year over year, rose 6.4% versus expectations for a 6.2% increase and 6.5% in December.

- Core CPI, year over year, rose 5.6%, just above expectations for a 5.5% increase and versus 5.7% in December.

Data Revisions Show Stickier Inflation

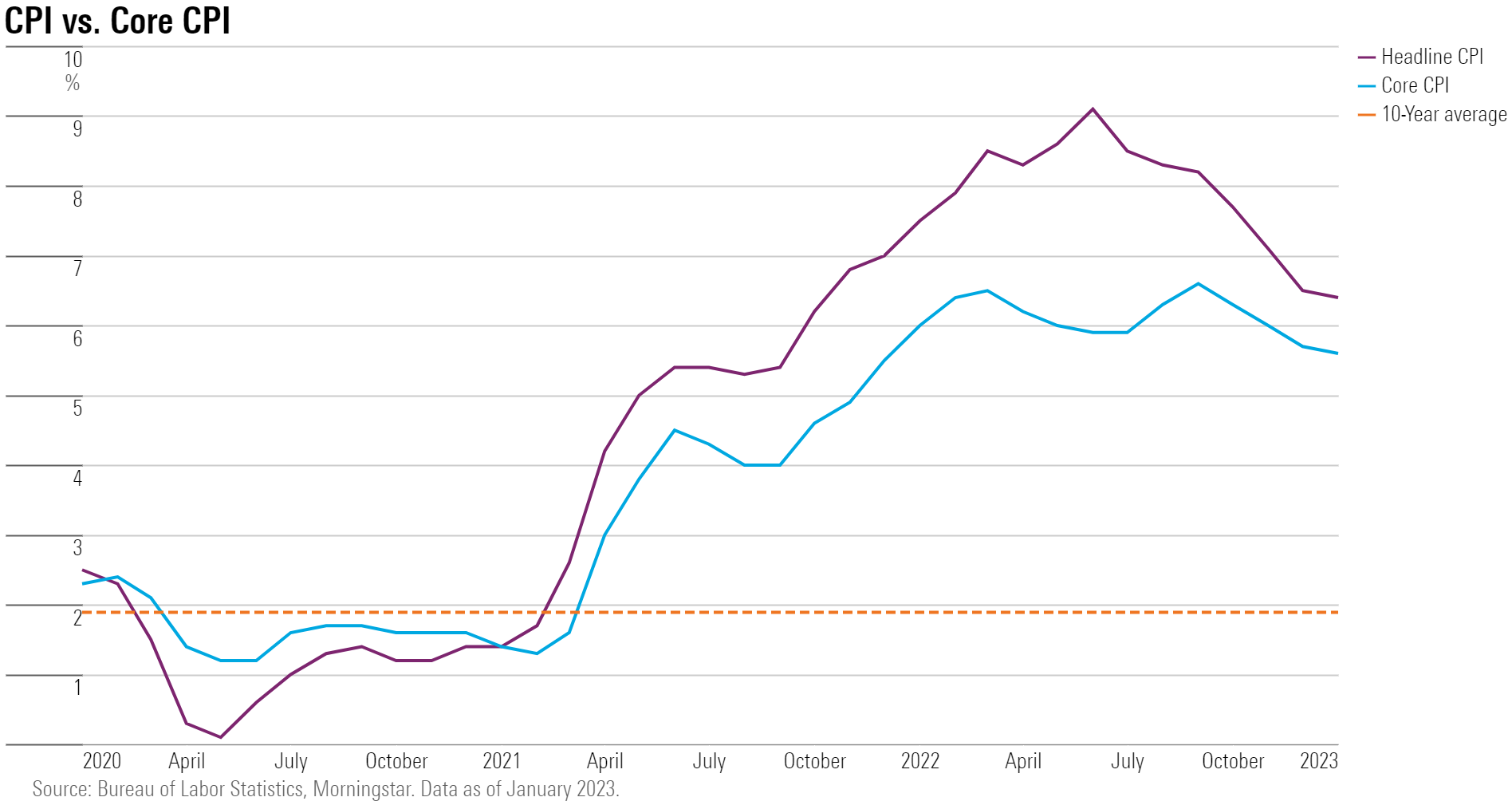

On a year-over-year basis, inflation is still trending lower: CPI increased 6.4% for the 12 months ended in January, its smallest 12-month increase since October 2021. Core CPI rose 5.6% year over year for the smallest reading of its kind since December 2021.

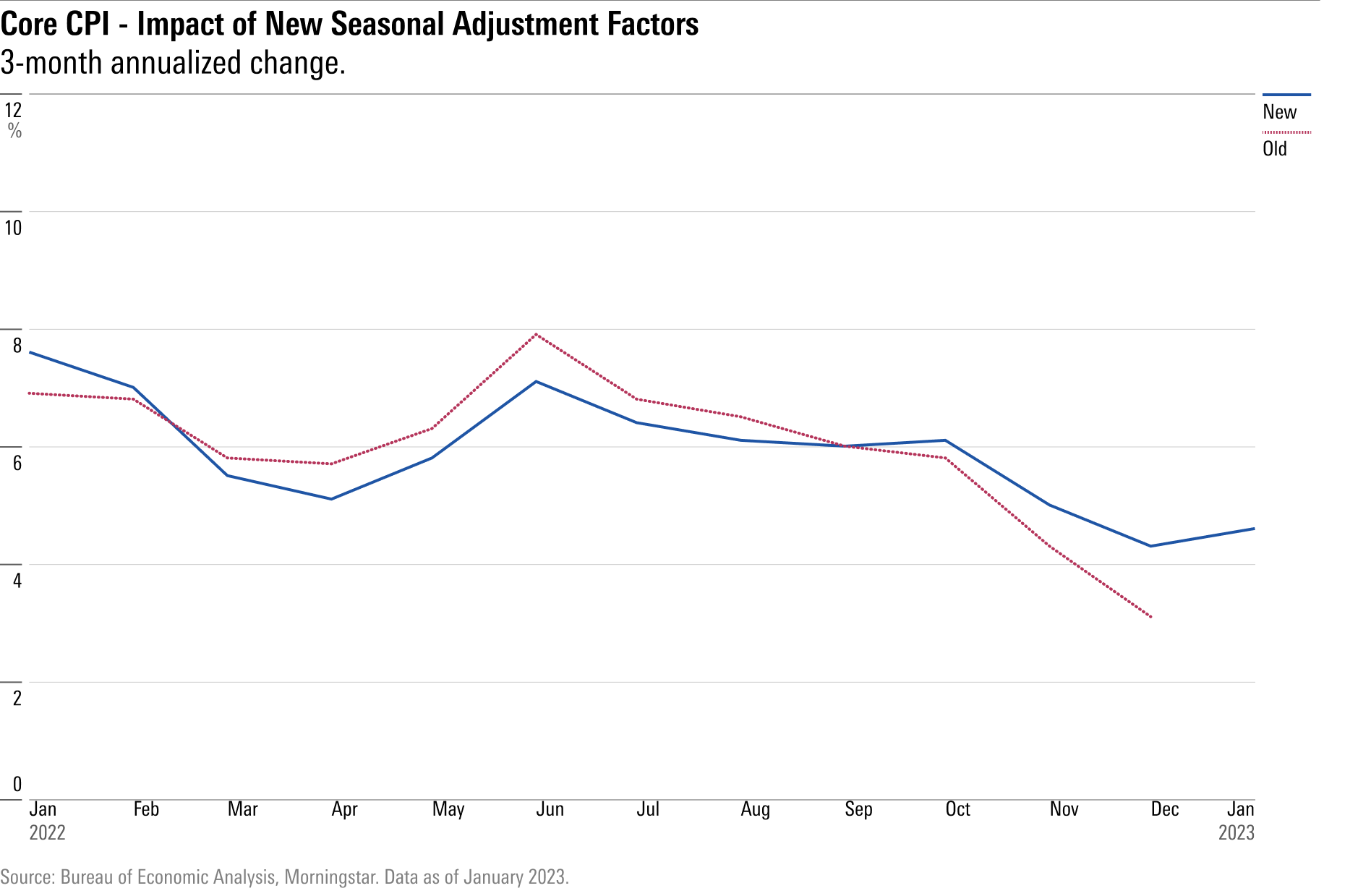

“Based on the revisions to recent historical data, the decline in core inflation now looks less impressive than previously shown,” Caldwell says.

“For 2022, inflation is now thought to have been slightly lower in the middle of the year, while slightly higher toward the end of the year,” he says. Previously, core CPI averaged a 3.1% annual rate in the three months through December, according to Caldwell, “but the BLS now estimates it at 4.3%.”

The data revisions are due to an update in the seasonal adjustment factors used by the BLS, a process that occurs annually, Caldwell says.

“This year, the revisions were quite large, as the pandemic has produced large changes in the seasonal pattern of price changes.” Caldwell emphasizes that the BLS hasn’t revised up its assessment of how much prices have gone up; rather, it reallocated the rate of inflation among different parts of the year.

Caldwell adds that the Fed’s preferred inflation gauge—the personal consumption expenditures price index, or PCE—will not be affected by the latest data revisions to the CPI. Core PCE inflation averaged a 2.9% annualized rate in the three months ended in December, Caldwell says.

CPI Report Shows Inflation Still Trending Downward

Rather than a precipitous drop at the end of 2022, the updated data for core CPI shows more of a gradual decline from a peak early in the year, Caldwell says.

“This new picture makes sense given the macroeconomic backdrop. Growth in consumer spending and economic activity has trended down since mid-2021.” Caldwell says the revisions fall closer in line with the past year’s economic trends: In addition to the slowdown in consumer spending growth, supply chain disruptions (outside of the impact of Russia on oil and gas markets) have also declined over the past year. “Both of these factors should have acted to cool off core inflation over the past year.”

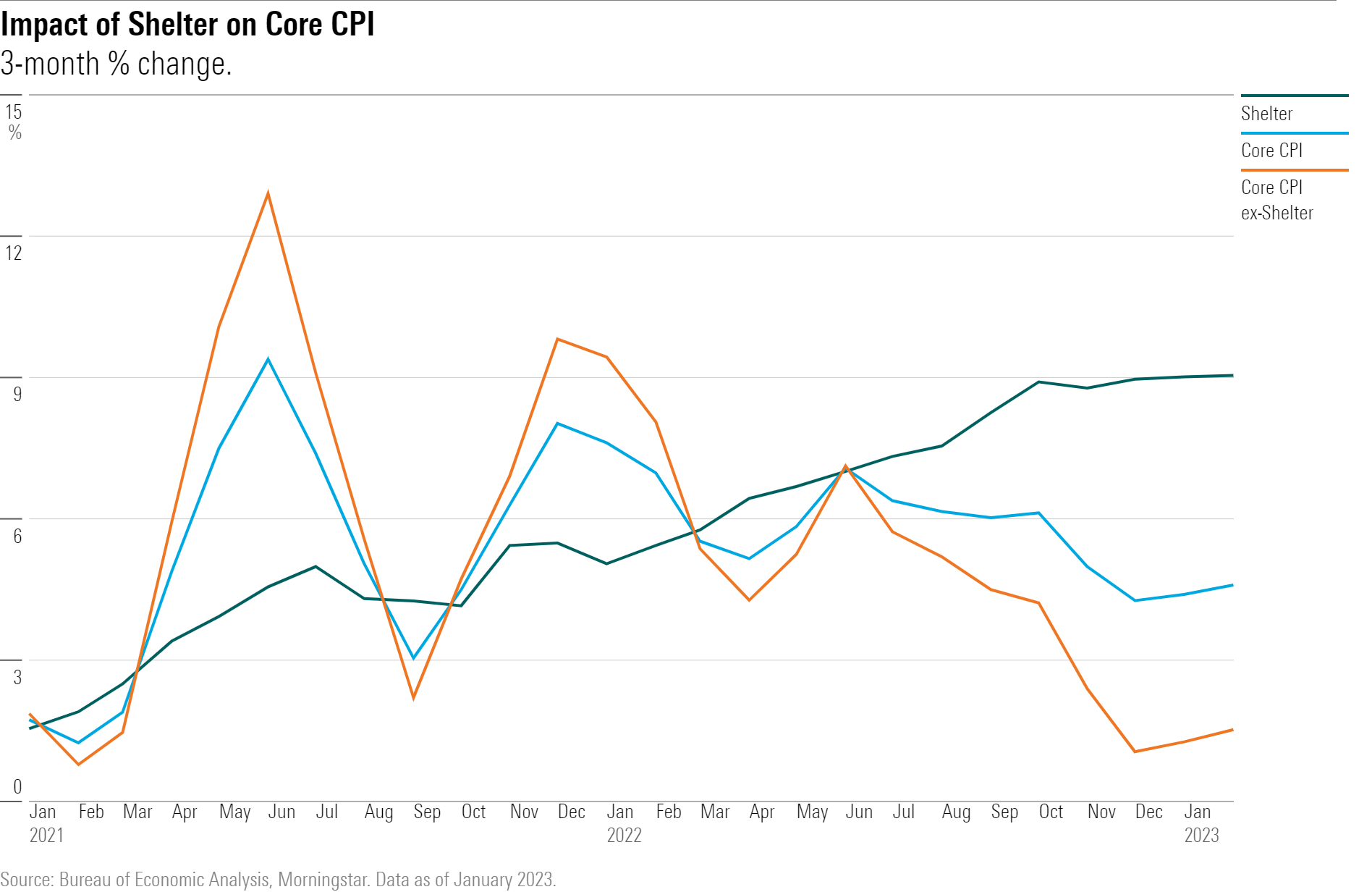

Shelter Costs Drive CPI Growth, for Now

“Currently, shelter prices are single-handedly propping up core CPI growth,” Caldwell says.

Excluding shelter costs, the rest of core CPI has averaged just 1.5% annualized over the past three months, according to Caldwell. “That’s below the Fed’s 2% target.”

Shelter inflation is still running at a blistering pace of 9%, but Caldwell says this won’t last much longer. “Market rent inflation has continued to decelerate and now stands at about zero, owing to falling housing demand and rising supply.”

In addition, “Shelter prices in the CPI reflect market rents with a lag,” Caldwell says, “So we can be highly confident that shelter inflation will fall greatly over the course of 2023.”

In January, energy prices rose 2.0% over the month as gasoline prices rose 2.4% and utility (piped) gas services prices rose 6.7%. In terms of core goods and services, apparel prices rose 0.8% over the month in January and medical care commodity prices rose 1.1%.

Prices fell over the month for used cars and trucks, down 1.9%.

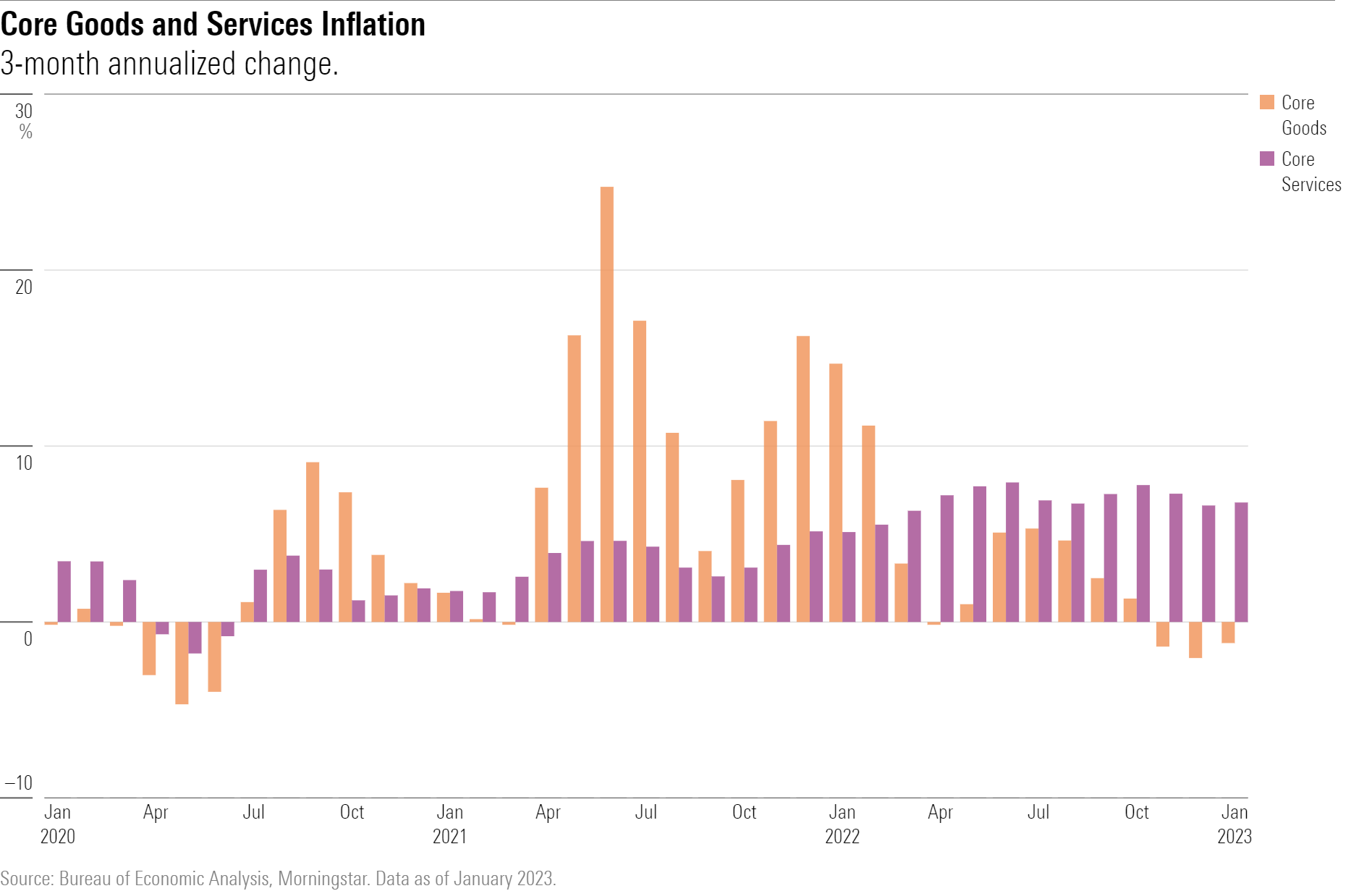

Goods and Services Inflation

The bulk of the decline in core inflation has been driven by core goods prices, Caldwell says.

“Pessimists would argue that this is a temporary factor and that core inflation will rebound once it abates.” Caldwell thinks, however, that the decline in core goods prices still has a long way to play out, “as prices—especially for durable goods—are still well above their prepandemic trends.”

The Fed has been keeping a keen eye on core services prices, excluding housing. Caldwell says that prices in this area, excluding healthcare as well, have averaged a 5.8% annualized inflation rate over the last three months. “Services ex-shelter, ex-healthcare prices are still quite elevated—though they’ve come down from November levels of 7.8%.”

Interest Rates May Stay Higher, Longer

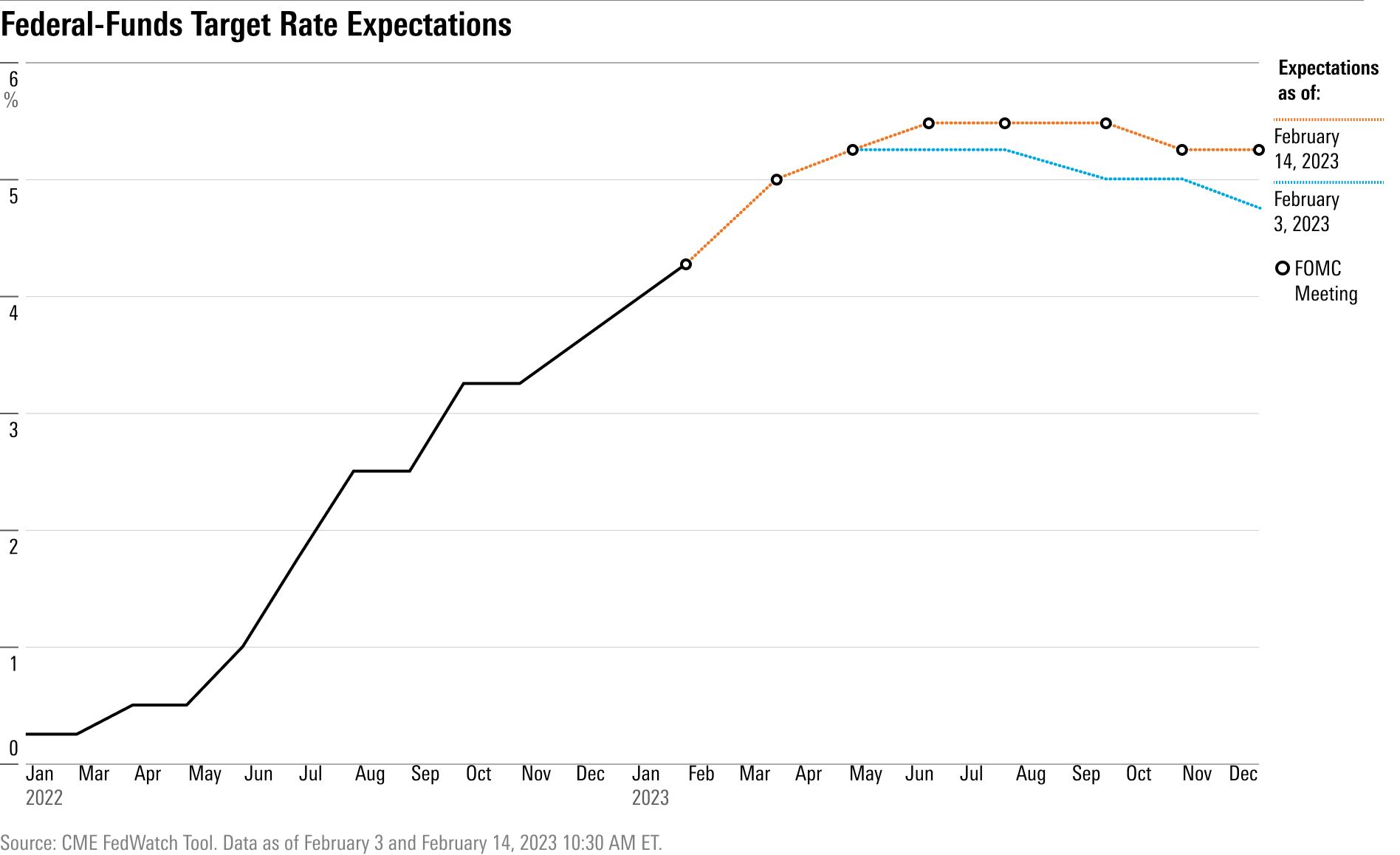

For investors, who increasingly have been looking for the Fed to halt its interest-rate increases by the end of the year, the latest inflation report, coupled with the strong jobs report released earlier in the month, shows that those hopes may be diminishing.

The latest data has prompted a shift in expectations for the Fed raising rates higher and holding them in place longer. According to the CME FedWatch Tool, the majority of market participants expect the federal-funds effective rate target to rise to 5.50% this summer, up from a high of 5.25% that was widely expected earlier in the month. And for the end of the year, the market now sees the Fed trimming the funds rate to 5.25% through December, as opposed to falling back down to 4.75%.

And for the short term, “today’s report will have some impact on the Fed’s decision on whether to hike the federal-funds rate again at its March meeting,” Caldwell says.

The market’s expectations have held strong regarding a quarter-point increase in the federal-funds rate at the upcoming March meeting, unchanged from where expectations had lain after the release of the strong jobs report earlier in the month.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)