Don’t Lose Faith in the 60/40 Portfolio

Inflation holds the key, but over time, the approach still looks sound.

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

Perhaps no development caught investors off-guard last year more than the failure of the tried-and-true diversification strategy of owning bonds to cushion against losses in the stock market.

The inability of so-called 60/40 portfolios—shorthand for diversified strategies with 60% stocks and 40% bonds—to offer investors protection from the bear market in stocks has upended what had become conventional wisdom among the markets: Stock prices and bond prices tend to move in opposite directions. So during a bear market for stocks like last year’s, bonds should have helped a portfolio, not inflicted more damage. That thinking has been a foundation of diversification for many years.

“The question many investors are asking themselves is this: Does diversification still make sense? Will it still provide value?” says John Queen, lead fixed-income portfolio manager at Capital Group and a manager on the $198 billion American Funds Balanced Fund.

For Queen, the answer is a resounding “yes.” For others, it’s a “probably” depending on the outlook for inflation and investors’ time horizon. In the end, much depends on the bond side of the equation.

“In the long run, whether bonds will do their job within the 60/40 depends on what happens to inflation on a structural level,” says Jurrien Timmer, director of global macro at Fidelity Investments.

To get a better understanding of last year’s dismal showing by 60/40 diversified portfolios and what will shape future performance, we spoke to experts at five of the largest mutual fund companies: BlackRock, Capital Group, Fidelity Investments, T. Rowe Price, and Vanguard Group.

Among the key takeaways:

- 2022 was an extreme environment for bonds.

- The stock/bond performance relationship isn’t set in stone. Inflation has a big impact.

- Stocks and bonds move together more often than investors might think.

- Higher bond yields will help the 60/40′s effectiveness.

- The mix between stocks and bonds—60/40, 80/20, and so on—matters.

- Diversification still works.

“Chances of a repeat of last year’s poor performance are low,” says Wei Li, global chief investment strategist at BlackRock. At the same time, she says, “We’re entering an era of higher market volatility. And that has implications on the 60/40 as well.”

It Wasn’t Just Bad—It Was Very Bad for 60/40 Portfolios

There’s no doubt about it: Last year was a disaster for investors relying on bonds to protect against a significant drop in the stock market.

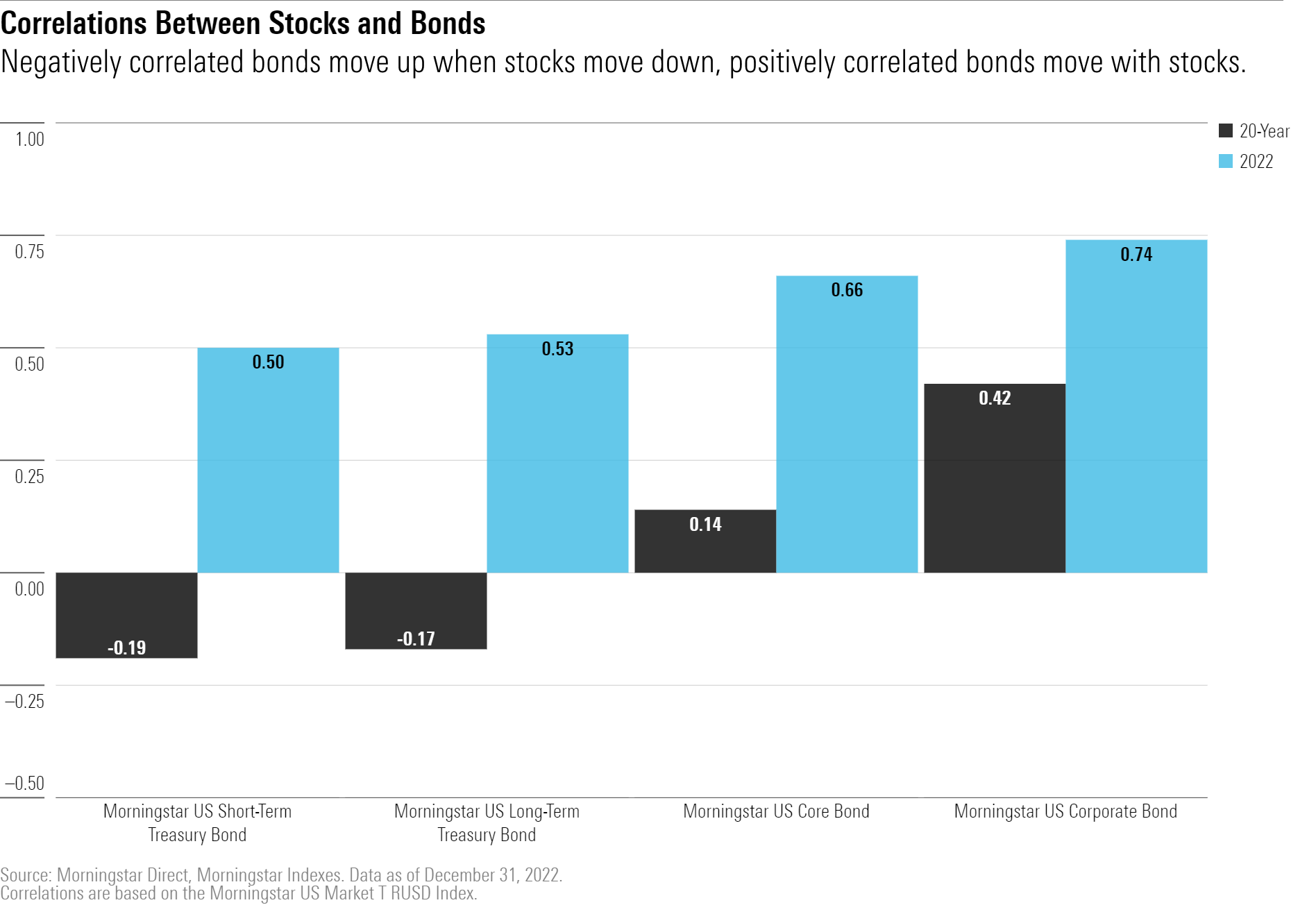

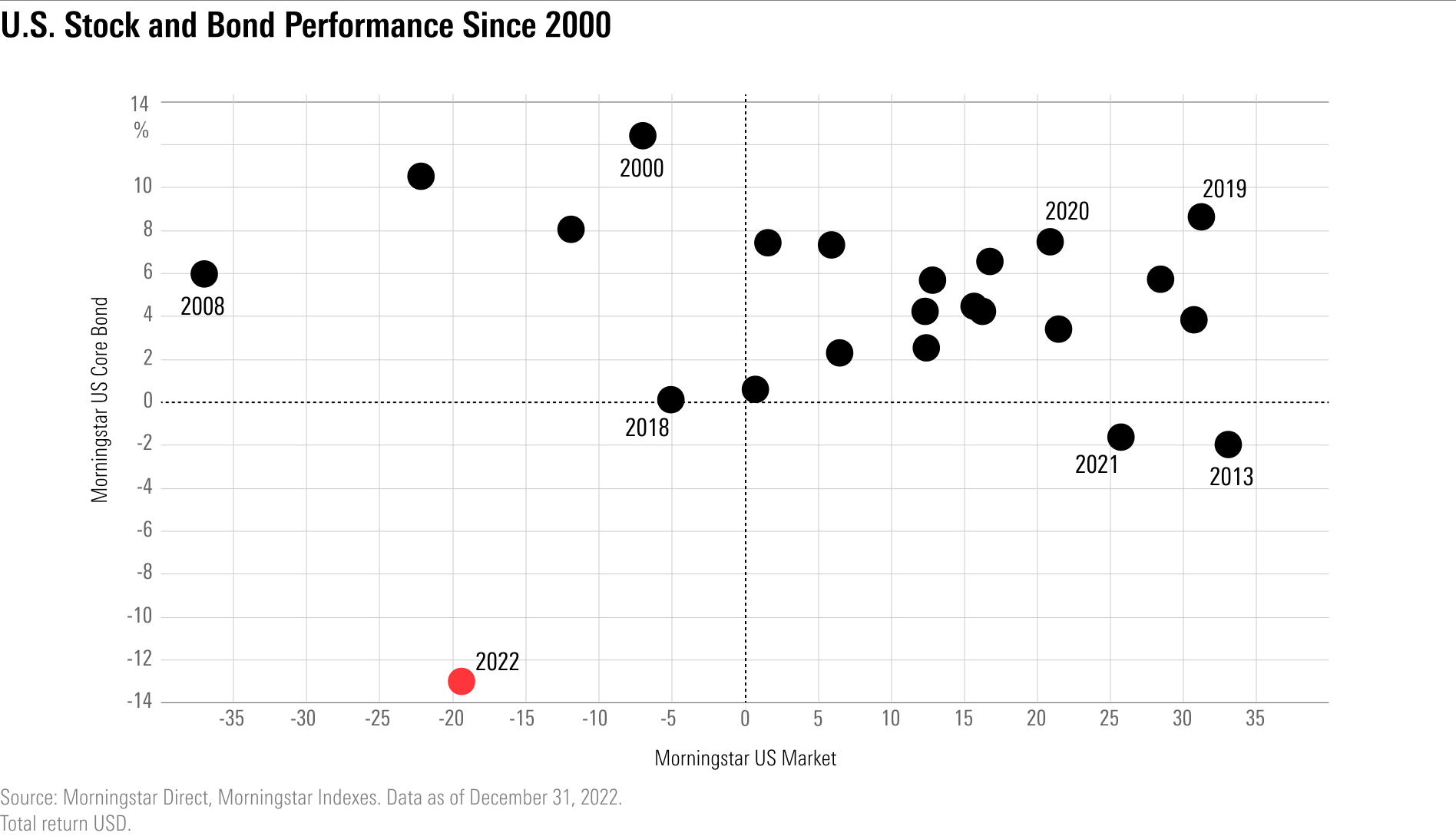

On the stock side of the equation, the Morningstar US Market Index fell 19.4% in 2022 for its biggest loss since 2008. Meanwhile, the Morningstar US Core Bond Index had the worst year in its history, down 12.9%.

Put the two together and it was bad news for investors. The Morningstar US Moderate Target Allocation Index—a diversified mix of 60% equities and 40% bonds designed as a benchmark for a 60/40 allocation portfolio—fell 15.3% in 2022, just 4 percentage points better than the stock market’s decline of 19.4%, as measured by the Morningstar US Market Index. Those double-digit losses made for the 60/40 index’s worst calendar year since 2008.

Why 60/40 Works … and Doesn’t Work

At the heart of diversification is the idea of owning investments that have different performance characteristics. If one takes a big hit, there’s something else in the portfolio that goes up, or at least doesn’t fall very much.

And underlying that is the concept of correlation. Correlation measures the tendency of different investments to move up or down at the same time.

When measuring correlation, a reading of 0 indicates stocks are moving with no relationship, while 1 means gains or losses in perfect unison. Positive readings mean direct correlations. Negative readings are known as inverse correlations.

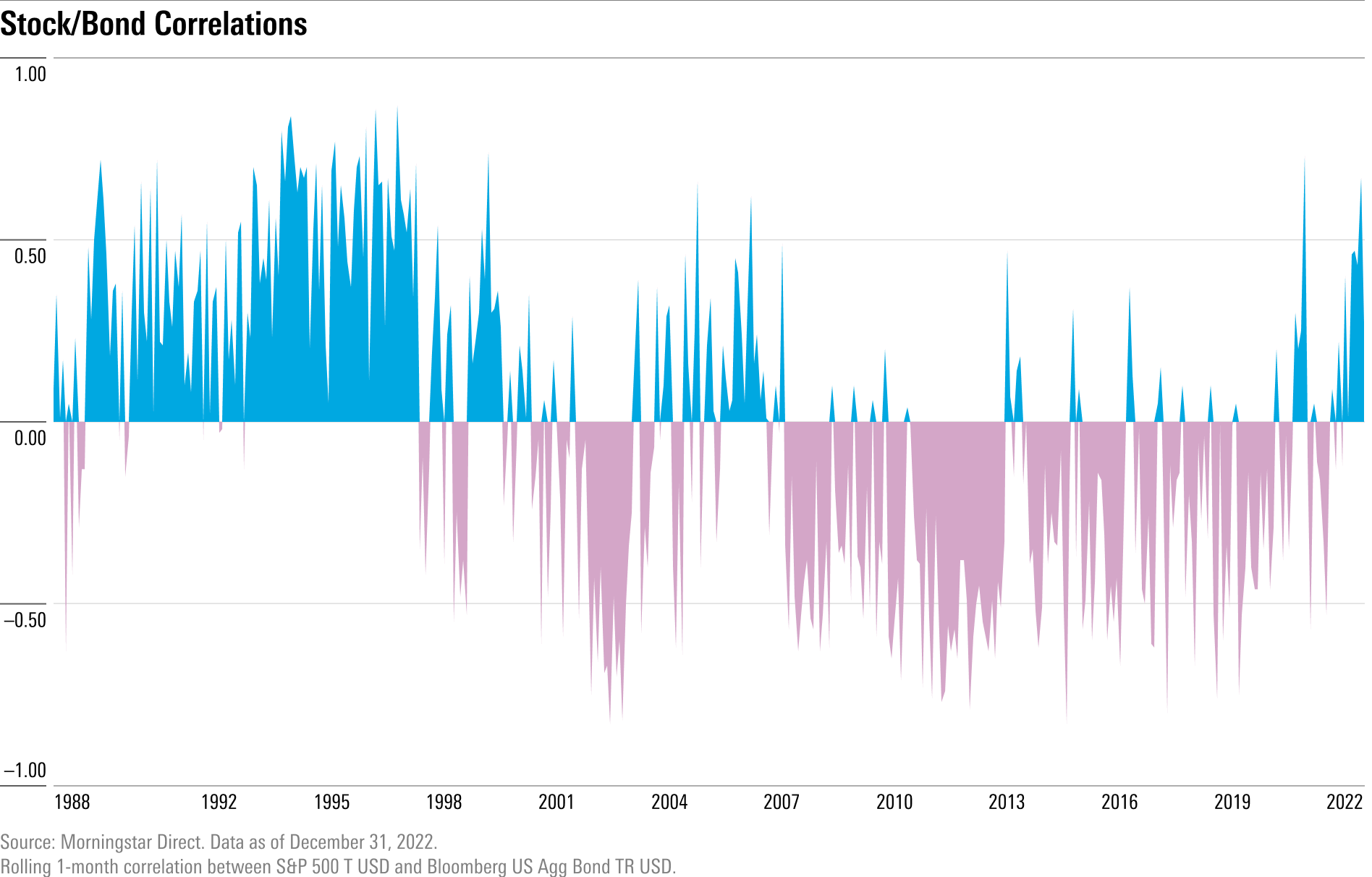

Over the past 30 years, stocks and bonds have, overall, been negatively correlated most of the time. That’s been the basis of the 60/40 diversification strategy: When stocks fall, bonds serve as ballast.

“When stocks go through big, broad selloffs, generally one of two distinct drivers is behind the losses: economic weakness, or a spike in inflation,” says Tim Murray, capital markets strategist at T. Rowe Price. “When economic weakness is the driver—and this is the most common scenario—interest rates often go down, which is good for fixed income,” Murray says.

But when losses in the stock market are driven by unexpected, surging inflation, Murray says, as was the much rarer case last year, both stocks and bonds tend to suffer.

Fidelity’s Timmer also emphasizes that the overall level of inflation can affect the correlation between stocks and bonds.

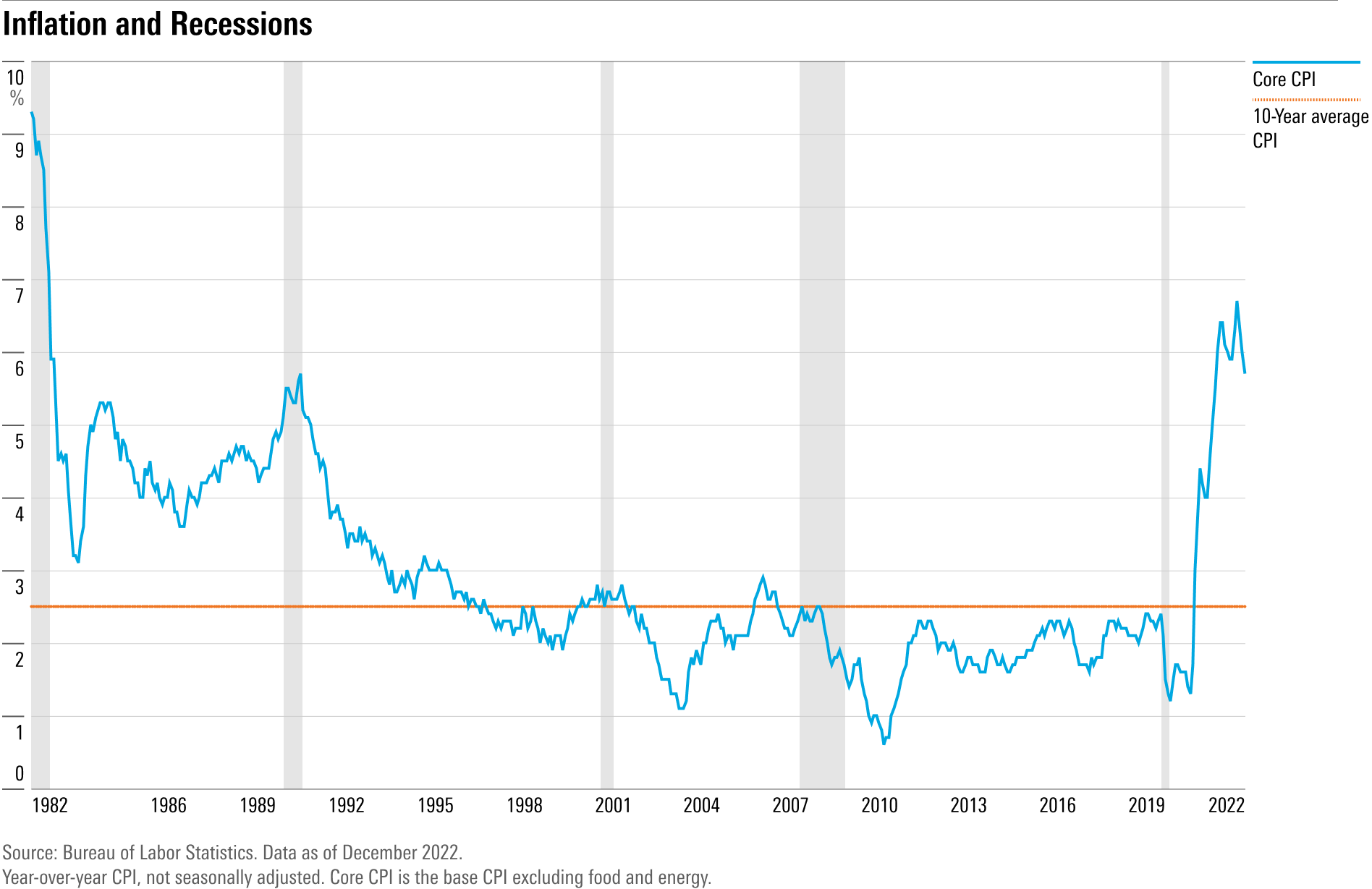

“Looking over the past 150 years, disinflation—that’s when inflation rates are trending lower—tends to produce a negative correlation between stocks and bonds,” Timmer says. “That means the ‘40′ (bonds) side of the portfolio becomes a port in the storm when the ‘60′ (stocks) doesn’t do well.”

On the other hand, Timmer says, for periods of time when the inflation rate has been above its long-term average, “The negative correlation between stocks and bonds isn’t really there: Bonds don’t protect against losses in the stock market.” The sky-high inflation of the past year was a big part of why stocks and bonds suffered together in 2022.

Bonds and Stocks Move Together Often—but Mostly Higher

When stocks and bonds both move in the same direction, it only hurts when they’re both on a downswing.

Last year was a clear anomaly, with both bonds and stocks in double-digit loss territory. But the two had already shown some positive correlation—when one falls, so does the other; when one rises, so does the other—in the years leading up to 2022. In four of the five most recent calendar years before 2022, both stocks and bonds rose, as measured by the Morningstar US Market and US Core Bond Indexes.

In fact, overall stocks and bonds have shown positive correlations in 15 of the past 20 calendar years leading up to 2022, each earning positive returns every time. The risk of double-whammy losses was there, but positive correlations had mostly been favorable for investors, until 2022 flipped things upside down.

“A big takeaway from last year is that bonds and equities really can go down at the same time,” says Todd Schlanger, senior investment strategist at Vanguard. “We can’t let ourselves forget that this can happen.”

Correlations Can—and Do—Change

What many investors don’t realize—or had forgotten—is that correlations aren’t written in stone.

“One of the things that we hear a lot about is that bonds and stocks are negatively correlated,” says Capital Group’s Queen. “The fact is, though, that really only started in the ’90s when Alan Greenspan was Fed chair.”

The driver of this shift, Queen says, was what became known as the Greenspan Put: Whenever equities started to fall, the Fed would lower rates to support equities and put a damper on the strong, quickly globalizing economy. “Inflation stayed low during that time, and the Fed was able to be incredibly accommodative,” bringing the negative correlation between bonds and stocks to life. (This later became more generally known as the Fed Put. The term put comes from the options market, where investors use put contracts to protect against suffering losses in stocks.)

In fact, going way back to the 1970s, says Vanguard’s Schlanger, both stocks and bonds have experienced losses in tandem around 30% of the time on a monthly basis and 15% of the time on an annual basis. “It’s not unprecedented for equities and bonds to go down together,” especially as inflation has heated up to decades-high levels over the past year.

Inflation Wasn’t the Only Problem

Decades-high inflation may have been the primary problem for the 60/40 portfolio, but there was another important variable: near-zero interest rates at the start of the year.

Because of the way bond pricing works, the three-decades-long decline in interest rates that lasted through 2021 meant that bond valuations were extremely high at the start of 2022, so they had a lot of room to fall.

The key, Fidelity’s Timmer says, was those starting valuations. “When it comes to bond performance, interest rates rising from zero to four is an entirely different equation than interest rates rising from four to seven.” Bond performance will always suffer when interest rates rise, but starting from zero is “an entirely different ballgame. And that’s what led to extreme losses for bonds in 2022.”

But, says Timmer, “Last year was a hundred-year storm. If we go back in history, we cannot find this kind of juxtaposition with equity and bond returns both being as low as they were.”

Where Does 60/40 Go From Here?

In the near term, the key to how 60/40 diversification works for investors could be the degree to which inflation continues to decline from the four-decade highs seen last year.

Timmer says that the near-term outlook for bonds—and diversification—depends on the macroeconomic environment. Specifically, he says, whether the Fed can engineer a soft landing for the economy and avoid a recession, as well as its success in bringing down inflation. “Either way, though, the bond landscape has reset itself” to higher yields, he says. “That’s a much better starting point for the 60/40.”

Capital Group’s Queen echoes the importance of higher yields. “We may not have quite the strong negative correlations anymore, but now, we’ve got some income,” from bond yields well above inflation, Queen says. “I really do think it still makes sense to think about diversification and balance in portfolios.”

BlackRock’s Li sees a significantly different economic landscape than the one investors were used to before 2022, but one that should still see a better outcome for bonds as a diversifier.

“Chances of a repeat of 2022 are low,” Li says.

“In 2023, inflation will fall quickly, but it will settle at a level higher than what we’ve been used to,” says BlackRock’s Li. “We’re entering a new environment where the ‘goldilocks outcome’—equities and bonds both being part of a multidecade bull market—is over.”

However, “the next year has the mix of various ingredients that make me believe this is going to be better for equities and also certain parts of the bond market—especially the front end” of the bond market.

This new environment has implications for the 60/40 portfolio and how investors should diversify, Li says. “The mix of the portfolio matters a lot more in this environment. Our research shows that the equity-bond mix will matter four times more than it did before. Getting your mix correct and not letting your portfolio drift is more important than ever.”

While the specific percentage of bonds versus equities in a portfolio will matter more than returns, Li believes that the basic principle of diversification will still hold. When it comes to stocks versus bonds, “either-or will go up, not both at the same time.”

Diversification Will Still Work, Most of the Time

An important lesson from 2022, says Vanguard’s Schlanger, is that “the 60/40 is a long-term strategy. With any long-term strategy, you’re not expecting it to insulate you from losses altogether.” Schlanger’s research shows that when expanding the period to five-year intervals, the 60/40 has only experienced losses 0.1% of the time.

Given all that, “When we take the losses of 2022 into account,” he says, “the outlook for the 60/40 is better than it has been in over a decade.”

Capital Group’s Queen has strong faith in the continued value of diversification: “We had a bad year in the markets, so it was a bad year for the 60/40. Does balance suddenly not make sense? Does diversification suddenly not make sense? To me, it still does.”

Queen uses the analogy of highway driving to help investors understand the importance of owning bonds with a balanced portfolio. Investing is like driving, and many investors seek the highest return, the fastest. “If I ask investors, ‘What’s the fastest way to get from L.A. to San Francisco?’ A lot of them would choose some kind of race car. But the thing is, race cars are hot, loud, and they lack cushioning. Race car drivers come out of a couple hours of racing looking like they’ve been in a fight.”

Queen says that even race car drivers would need to get off the road when the going gets tough: The most important thing is to stay “on the road” over the long term. “You need a strong windshield, air conditioning, and comfortable seats: These things slow you down, but they make the ride comfortable. To stay diversified over the long term, you need bonds to smooth out the ride.”

Some investors can accept a rougher road than others, Queen says, but balance serves most everyone: “Whether diversification means 60/40 or 80/20 or 20/80 depends on the investor. But diversification smooths the road.”

Says Fidelity’s Timmer: “Just because the 60/40 didn’t work last year doesn’t mean it will never work again.”

Timmer says that the near-term outlook for bonds—and the effectiveness of 60/40 diversification—whether the Fed can sustain a soft or hard landing, and the long-term outlook depends on what happens with inflation. “Either way, though, the bond landscape has reset itself, and real interest rates are back in positive territory,” he says. “That’s a much better starting point for the 60/40.”

Correction: (Jan. 26, 2023): A previous version of this article misspelled the name of former Federal Reserve Chair Alan Greenspan.

Correction: (Jan. 26, 2023): This article was updated to correct the 2022 performance difference between the Morningstar US Market Index and the Morningstar US Moderate Target Allocation Index to 4 percentage points.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)