Busting the Tech-Stock, Bond-Yield Connection Myth

While rates matter to technology stock valuations, they haven't been driving performance.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

In late September 2021, technology stocks were rolling over, a summertime rally having suddenly deflated. Market pundits and investors cited a laundry list of causes for the sell-off, but one reason seemed to make the rounds more than others: a jump in Treasury bond yields was leading investors to ditch tech stocks.

"It really doesn't matter what Nasdaq stock we're talking about," said a well-known television markets pundit. Whenever Treasury bond yields rise, tech stocks fall, he and others claimed. "The linkage is so clear," he said.

But is it true?

It isn't.

It turns out that when the numbers are crunched, over the past 15 years there has only been a small inverse correlation between technology stocks and bond yields. In other words, when bond rates rise, there is a slight tendency for tech stocks to fall.

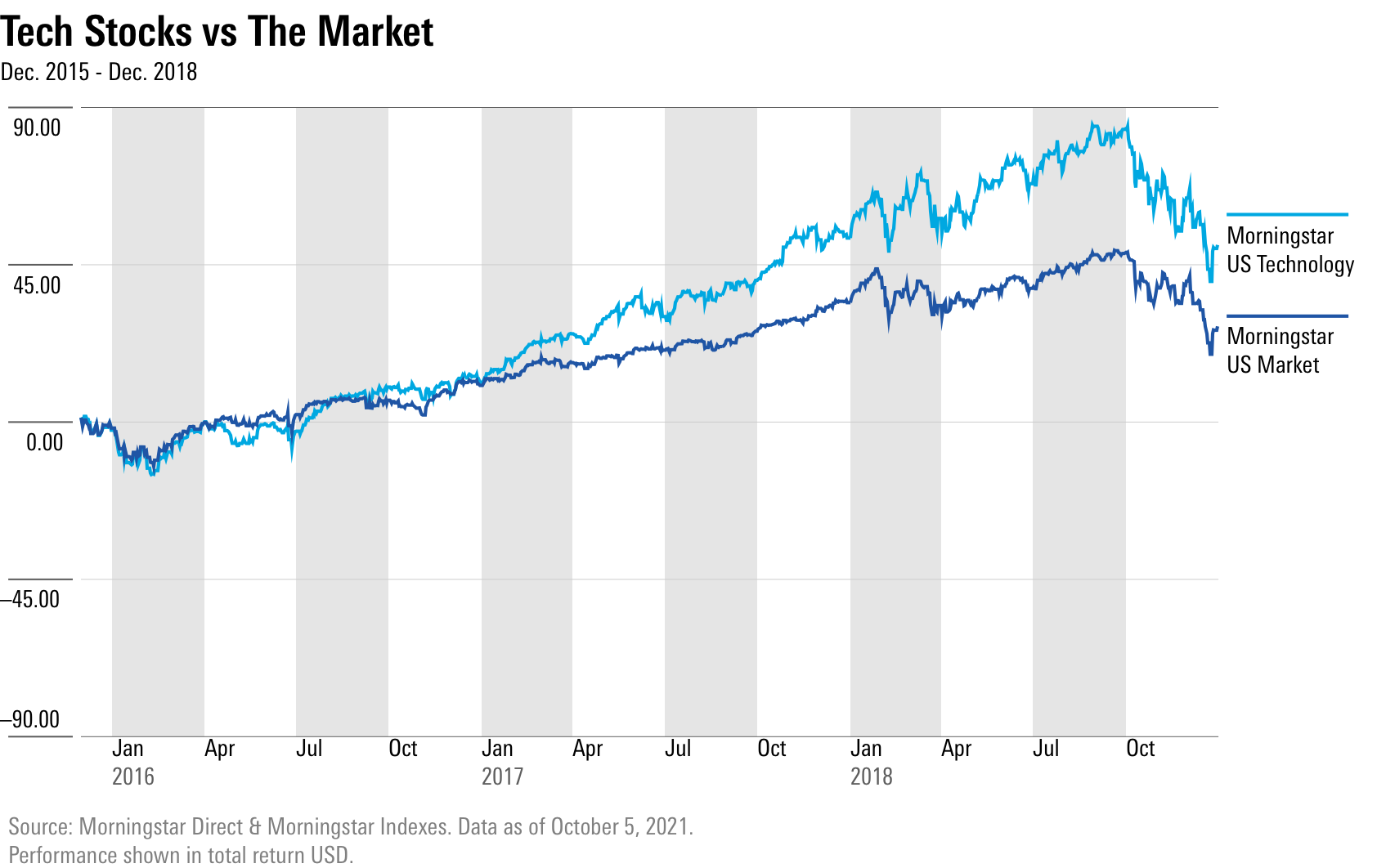

That was true also during the last time the Federal Reserve was raising interest rates, from late 2015 through the end of 2018.

This doesn't mean there is no connection whatsoever between technology stocks and interest rates. Rates are an important variable when coming up with valuations for tech stocks and other fast-growing companies. But when it comes to real-world stock prices, there hasn't been much of a connection.

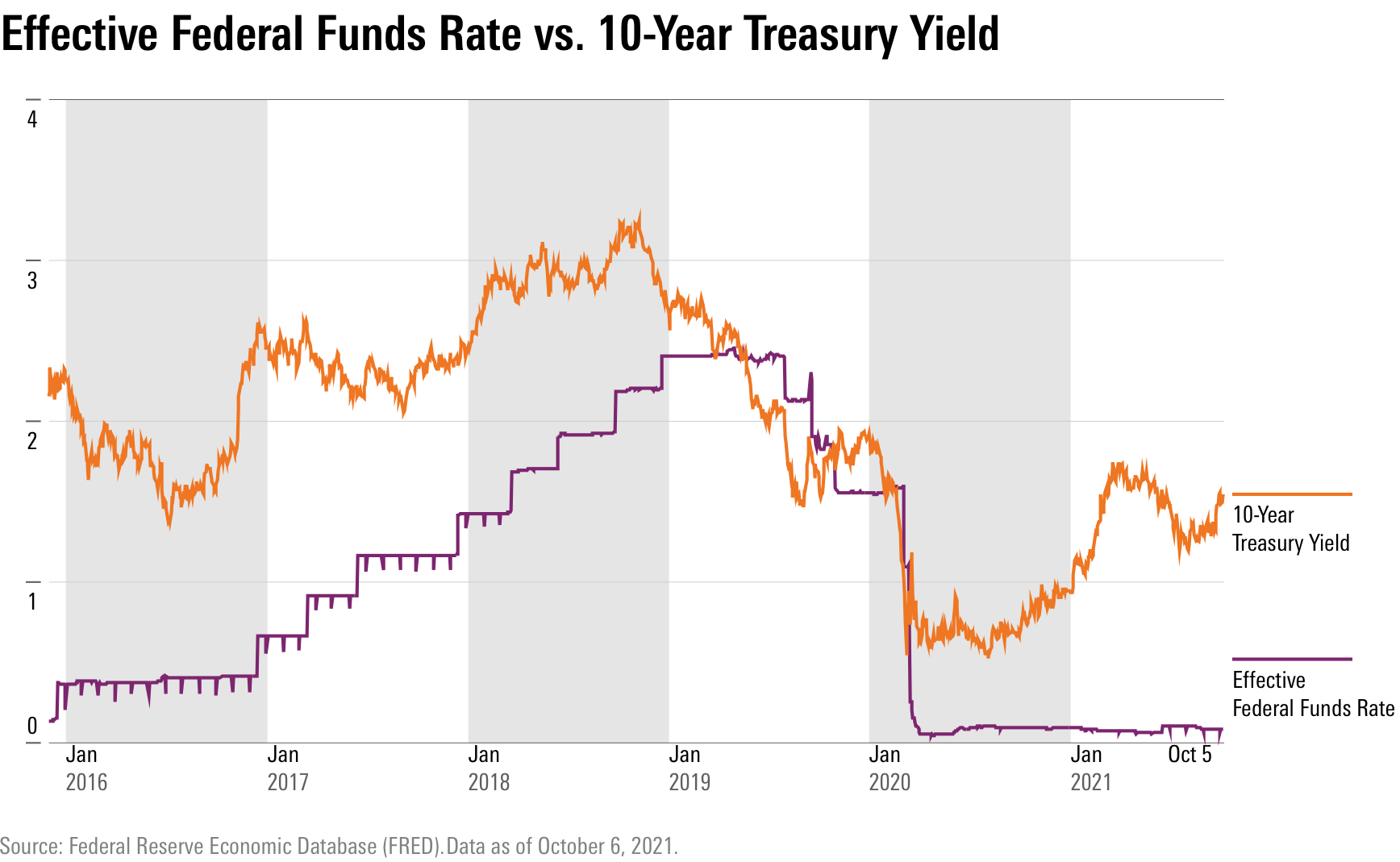

We'll start with where interest rates have been.

Although longer-term Treasury yields have moved higher this year as the economy has recovered from the pandemic-recession lows, by historical standards, yields are still relatively low. Meanwhile, the Fed has kept official interest rates low, with the federal-funds rate essentially at zero and expected to stay that way into next year.

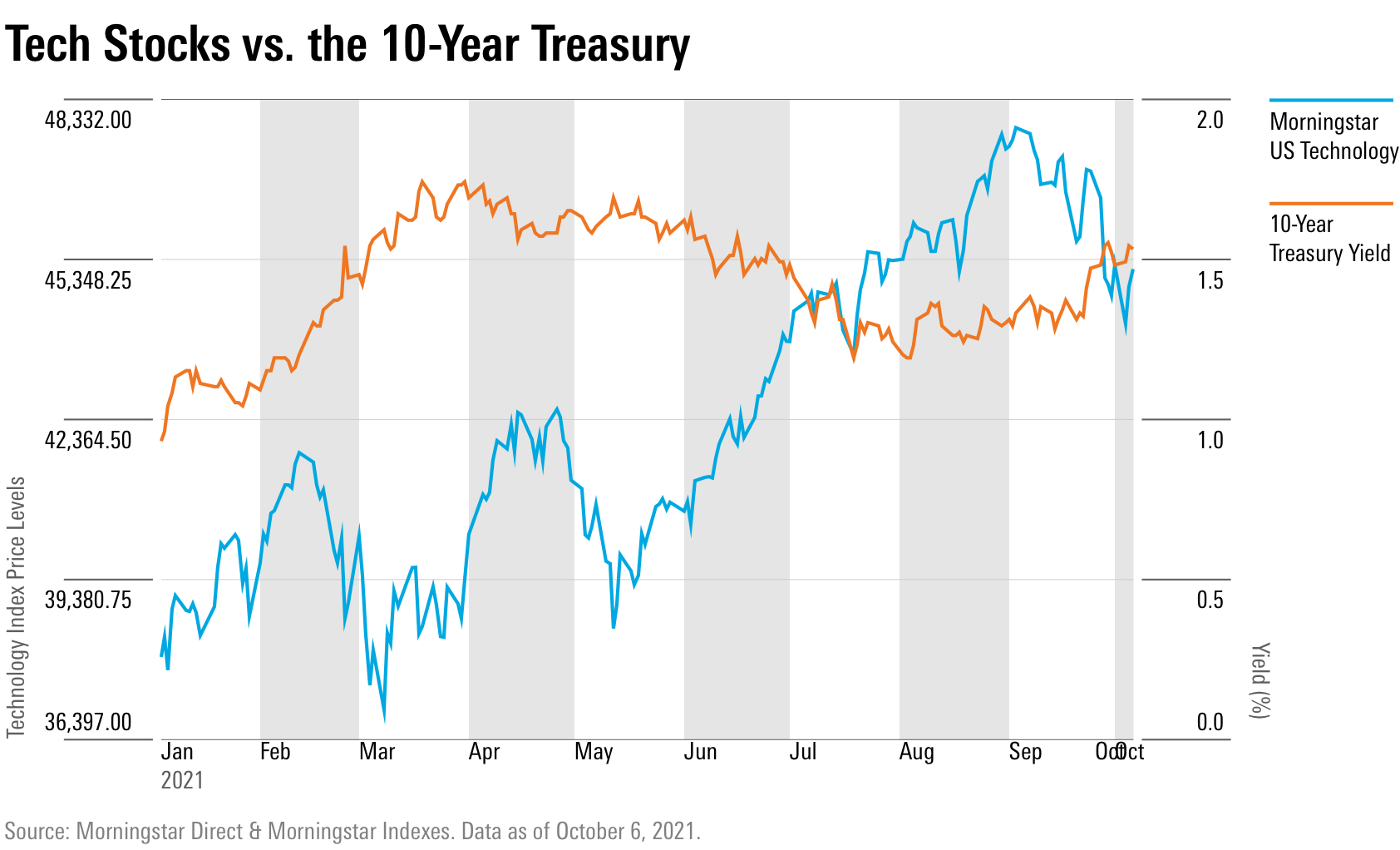

Let's drill down into 2021.

To start the year, yields rose markedly as the U.S. economy recovered from the pandemic recession, until the delta variant spread and expectations for the economy began to cool. However, as September got underway, inflation concerns were growing and bond yields jumped 21 points.

Technology stocks, meanwhile, started the year with a rally even as bond yields began to rise. After some seesaw movement during the remainder of the first half, the tech sector rocketed higher. By the beginning of September, the Morningstar US Technology Index was up 15.7% year to date, but over the course of the month it fell 5.8%.

On the surface it's possible to see that there might be a correlation. But how strong is it?

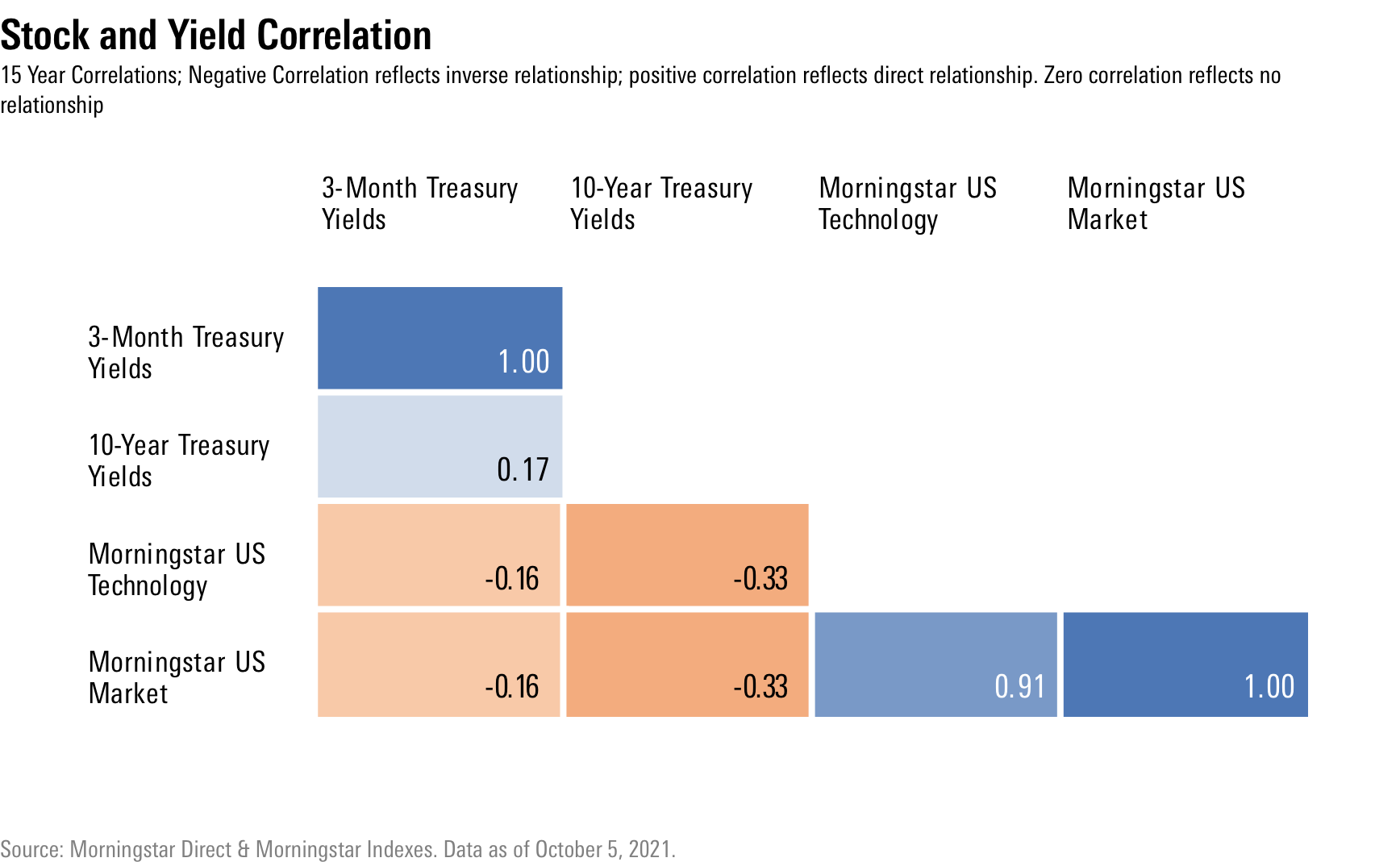

We ran correlation data between the Morningstar US Technology Index and the 10-year U.S. Treasury yield in Morningstar Direct. We added in short-term rates in the form of Treasury bills along with the broader Morningstar US Market Index. A reading of 0 indicates stocks and yields are moving with no relationship, 1 means gains or losses in perfect unison, and negative 1 means gains or losses occur in the opposite direction.

With a correlation of negative 0.33 between tech stocks and 10-year Treasury yields over the past 15 years, the inverse relationship is relatively low. When it comes to Treasury bill yields, there's almost no relationship.

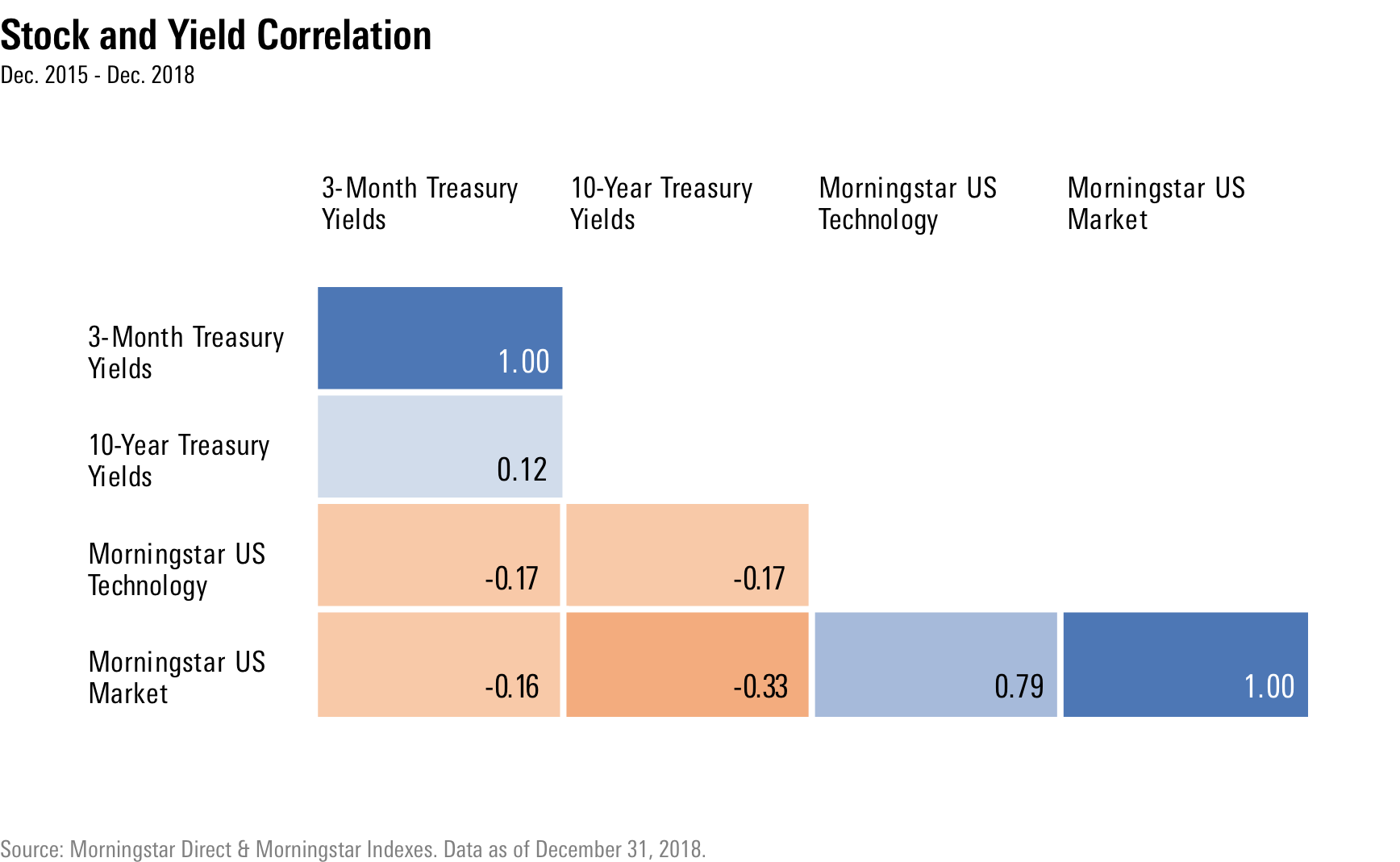

Perhaps it's only relevant when rates are rising? We looked at correlations during the period of the last Fed rate increase and found even less of a relationship between tech stocks and 10-year Treasury yields.

In fact, during this period, tech stocks outperformed the broader market.

Brian Colello, the technology sector director for Morningstar, notes that in theory, there should be a a solid inverse relationship between interest rates and tech stocks that relates to the way investors assess the value of a stock. It starts with the fact that the bulk of a fast-growing, tech company's earnings will occur in the future. In order to peg what the value of a stock is today based on those future earnings, an investor needs to discount the value of those future earnings. Higher interest rates translate into higher discount rates, which reduce the value of future cash flows and reduce the value of the stock today. "All else equal, tech stocks with more earnings in the future will face a greater hit with higher interest rates than mature companies where more of their earnings are in the present or near term," Colello said.

Why doesn't that seem to be playing out in the markets? Colello offers several theories. The first is that because rates have been especially low for a long period of time, any of the minimal increases were perhaps too small to matter much.

Another theory is that the tech expansion over the past 10 to 15 years has been exceptional and able to more than overcome any rise in interest rates. "The rise of the smartphone, the Internet of Things, cloud computing, and software as a service has been a strong secular tailwind within technology, and adoption has occurred during good times and bad," Colello said. "Even during the depths of the COVID-19 pandemic, enterprises rushed to upgrade their PCs and servers, while buying a host of remote-working software tools, such as those offered by Zoom ZM, DocuSign DOCU, and Shopify SHOP."

Lastly, "Tech stocks may have simply been due for a pullback," Colello said. "Tech was one of the stronger sectors in 2020 during the pandemic and generally outperformed the broader market. This led to many overvalued stocks at the start of 2021. It's possible that the latest pullback might simply be a healthy breather."

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)