Why Funds Die

A closer look at the traits associated with funds that have shut down in recent years.

/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)

Fund mortality is an often overlooked but important component of fund selection. Dead funds don't compound investors' capital, let alone beat the market.

Shutting down a fund may hurt investors in other ways. Liquidated funds may saddle an investor with the costs of closing a fund, an unexpected tax bill, and opportunity costs tied to reallocating assets. And merged funds potentially push investors into strategies that they didn't originally sign up for.

In our new paper, "Why Funds Die," we examine all U.S.-domiciled mutual funds and exchange-traded funds in Morningstar's database that launched between 2005 and 2020 to identify several common characteristics among those that eventually closed. (A note about the methodology: For this analysis, the term "closed fund" refers to those that cease to exist, meaning they were either liquidated or merged into another fund. Funds that continue to exist but restrict access to investors are considered open funds.)

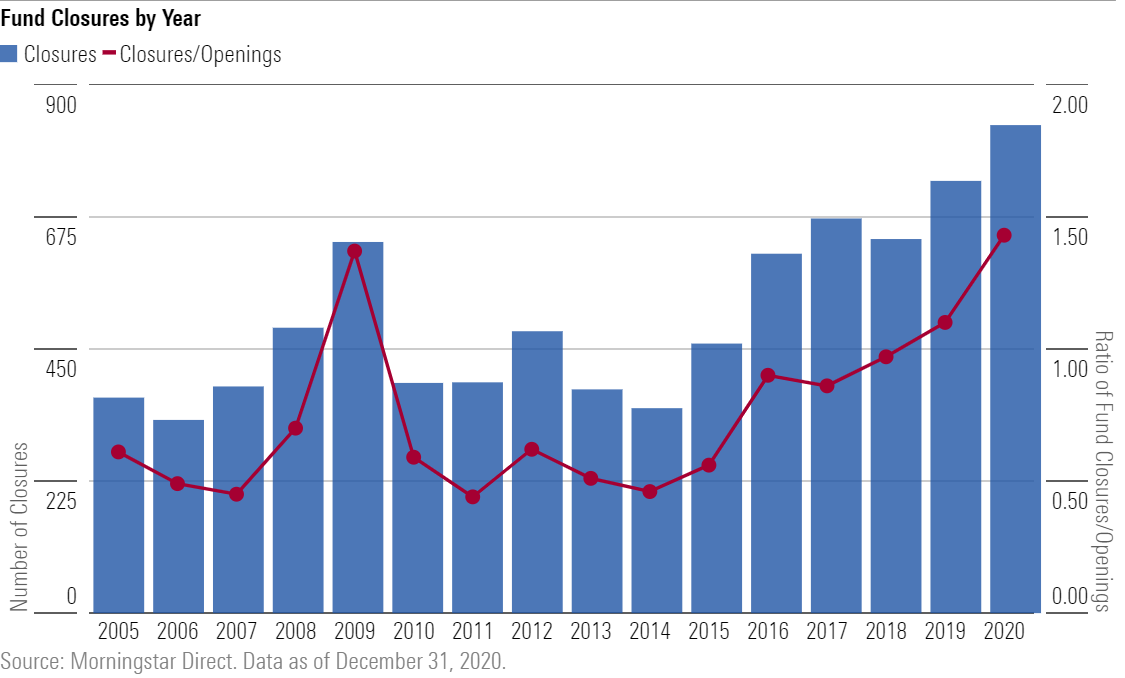

The increasing number of fund closures over the last five years underscores the importance of this topic. The chart below shows the number of funds closed and the ratio of funds closed to new launches for each calendar year from 2005 through 2020--both of which increased over this period. Additionally, the sharp rise in closures in the 2008-09 period indicates that the global financial crisis contributed to a higher-than-normal tendency (at the time) to shutter funds.

The fund characteristics that are associated with closures are short lives, low assets under management, high fees, poor performance, and ties to certain fund providers. By spotting funds with these traits, investors can avoid those that are more likely to close.

Fund Age

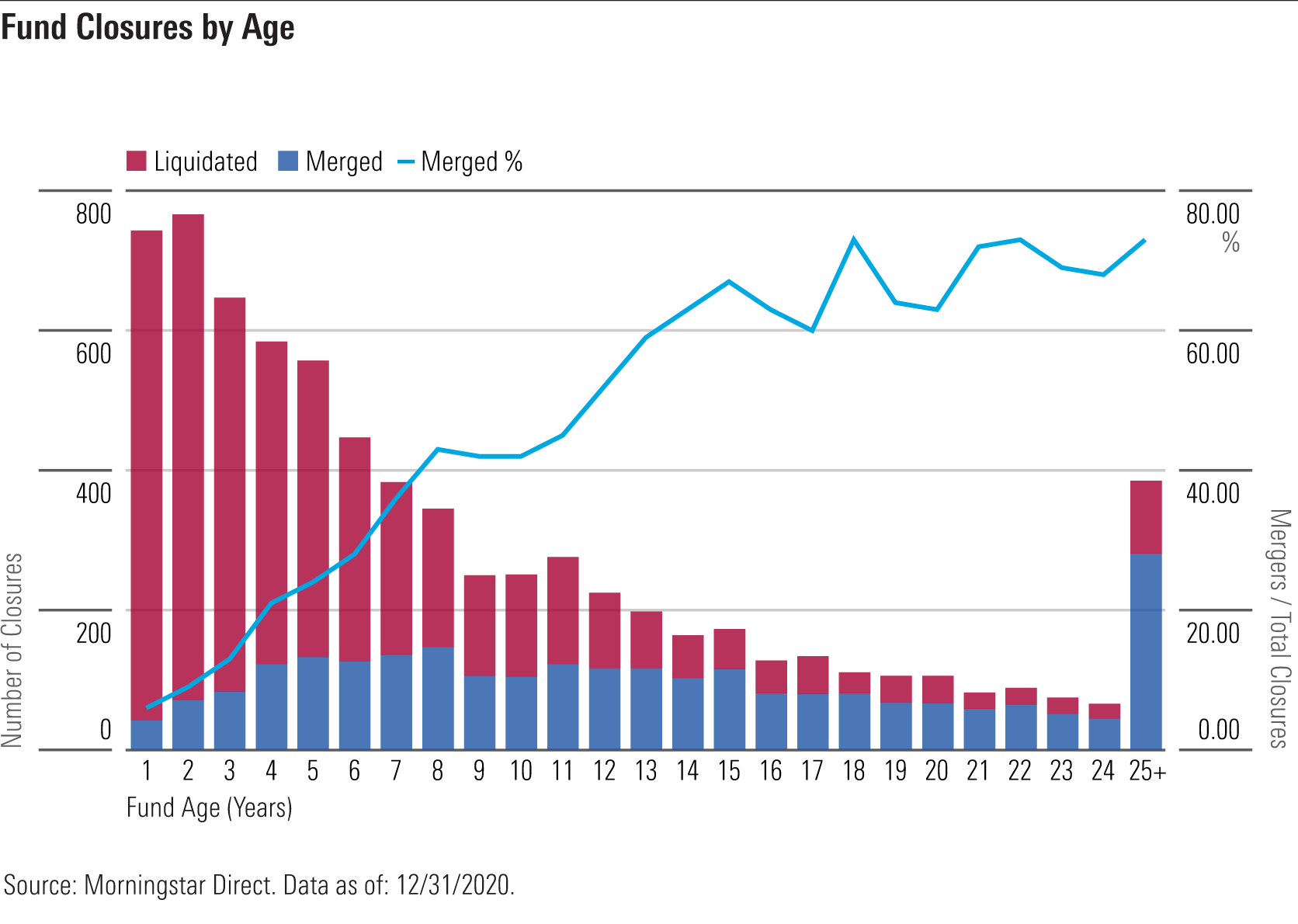

Fund age is one factor that might help to explain fund closures. The chart below plots the ages of all funds in Morningstar's database that closed between 2005 and 2020. As you can see, most were laid to rest early in their lives--and about 44% of those in this sample didn't even make it to their fifth birthday.

When older funds closed, they tended to be merged into other funds, while those with shorter lives were mostly liquidated. That trend may be partially explained by fund size, which appears to be related to age: On average, older funds have more assets than their younger counterparts.

From an investor's perspective, both kinds of fund closures can yield undesirable outcomes. Financial incentives may explain the tendency to merge older, larger funds into other funds. Mergers allow fund providers to retain the assets and the associated revenue from management fees. Conversely, younger and smaller funds were more likely to be liquidated, returning a fund's assets to its investors.

Fund Fees

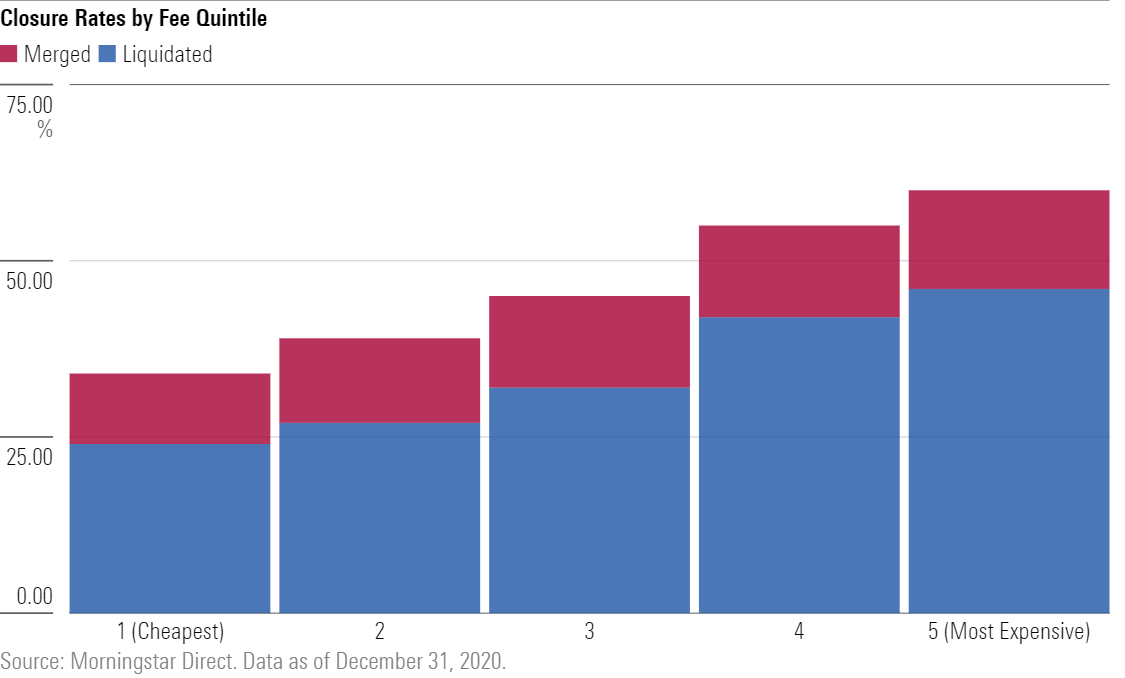

Fees are intertwined with performance: They directly drag down returns. As fees rise, so does the likelihood that a share class will shutter.

Fund fees have steadily declined for decades. The equal-weighted average U.S. fund fee clocked in at 0.98% in 2020--nearly a 20% decrease from 1990, when it was 1.22%. As investors flocked to the cheaper entrants, closure rates in more-expensive funds and share classes have ballooned.

The chart below illustrates our sample of share classes by fee quintile. It shows that those that ranked in the priciest quintile closed at a clip of more than 60% over the past 15 years--nearly double the rate of those in the least expensive quintile.

Fund Size

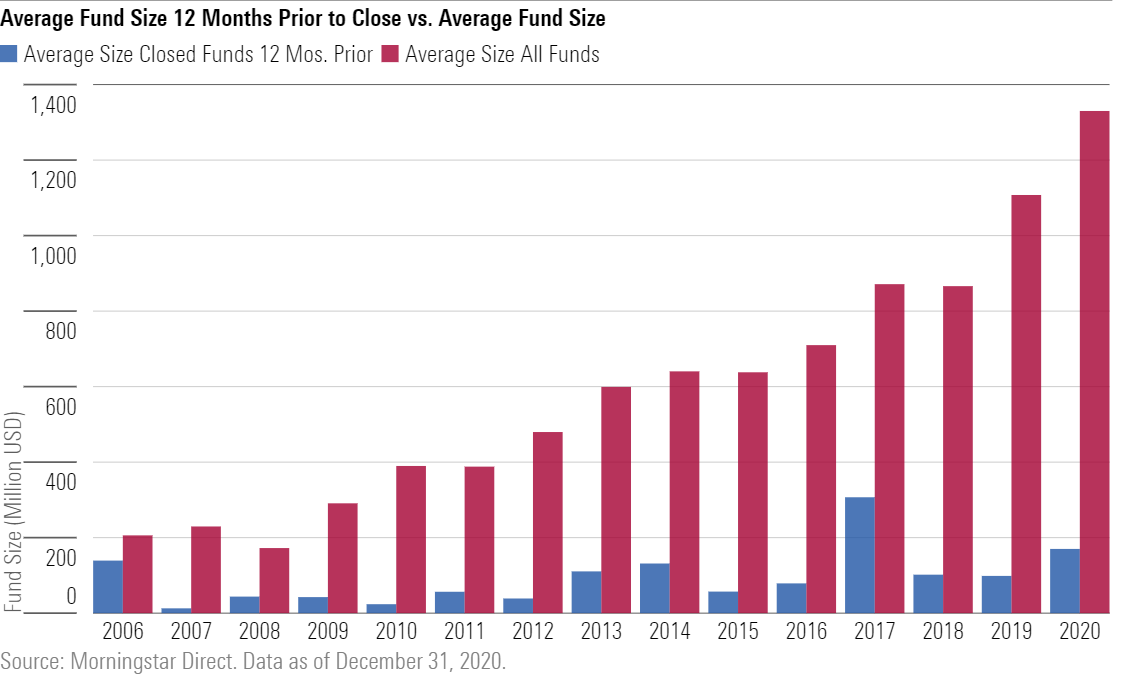

Fund size is a product of flows and performance. Many funds that don't accumulate significant assets either fail to drum up sufficient investor interest, perform poorly, or endure some combination of both.

That said, smaller funds have closed at a greater rate than their larger counterparts, likely for economic reasons. The fee revenue generated through the management of smaller funds may not cover the costs of running the portfolio.

The chart below illustrates this relationship. The chart compares closed funds' average assets 12 months before they closed with the average assets of all other funds on the market that year. Fund size is measured in advance of the closure date to control for any outflows that might occur between fund closure announcements and liquidation or merger dates. The increase in average fund size--among closed and open funds alike--reflects broad market appreciation over the past 15 years.

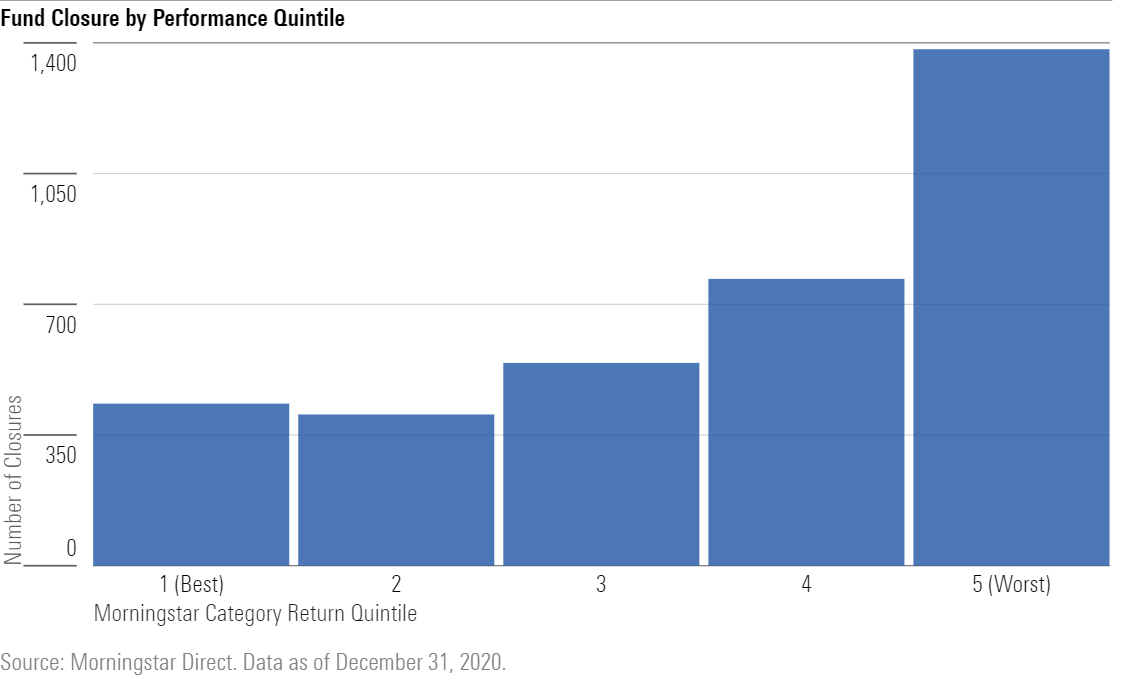

Fund Performance

The universe of funds under examination spans a wide range of asset classes and styles. As such, looking at Morningstar Category-relative total returns can help control for differences in asset class and style exposure when assessing performance as a factor that might influence fund closures.

The chart below sorts shuttered funds into quintile by how well they performed over their lives relative to their category peers; the best performers land in the first quintile of their respective category and the worst in the fifth.

A clear relationship emerged between category-relative performance and fund closures. About 12% of all closed funds landed in the best-performing quintile of their respective category, while 39% came from the worst-performing quintile.

Further analysis revealed a similar relationship between funds that close and their category-relative performance over their final 12 months. This relationship may prove more useful for spotting funds that are not long for this world. Trailing performance over the prior 12 months could be combined with the other characteristics examined here in assessing how likely it is that a fund will shut down.

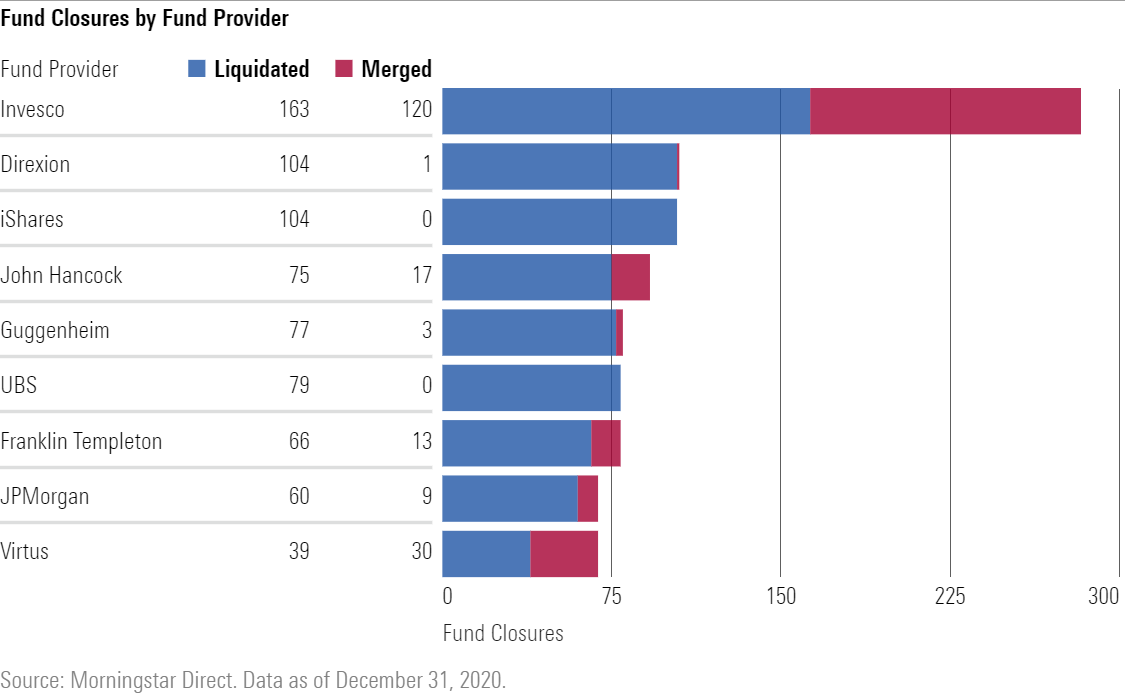

Fund Provider

Funds' proclivity to close may also be influenced by their parent. Different approaches to product development may be one reason. Firms may not exercise a high degree of discipline when developing new strategies. They might offer a wide variety of funds, see what sticks, and close those that fail to gather assets in a timely fashion.

The chart below shows the top-10 firms as ranked by the number of funds they shuttered between 2005 and 2020.

Invesco's liquidations and mergers are far in the lead, with a majority of closures occurring between 2018 and 2020. This coincided with the acquisitions of two of its smaller competitors: Guggenheim's ETF business in 2018 and OppenheimerFunds in 2019. So, the bevy of fund mergers in these years were part of an effort to consolidate funds from those acquired lineups with similar strategies already managed by Invesco.

Fund providers like Capital Group and Dodge & Cox are at the other end of the spectrum, with very few closures over this period. These firms are more cautious in launching new funds and are likely loath to close existing ones. From 2005 through 2020, Capital Group liquidated just one fund (Capital Group Emerging Markets Total Opportunities), while Dodge & Cox didn't shutter any.

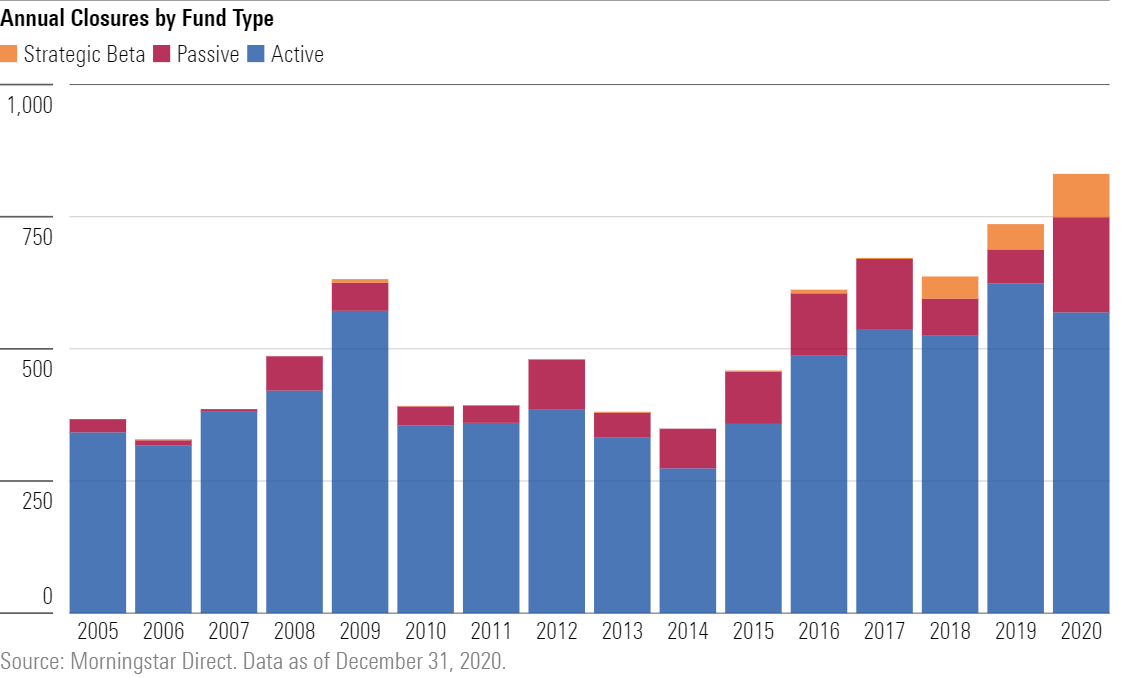

Fund Closings by Fund Type

The growth of index investing and, particularly, the rise of strategic-beta funds were major trends during the 2005-20 period. However, these index funds only accounted for a small portion of the funds that were closed or merged away during this span.

Rather, the chart below shows that actively managed funds accounted for most fund mergers and closings. The composition of the fund universe partly explains this, since actively managed funds still represented most of the funds in the sample. So, actively managed funds primarily drove the steady increase in closed funds over this period.

How Investors Can Anticipate a Fund Closing

All the characteristics that we examined appeared to have some linkage to fund closures, with a few caveats.

Overall, closed funds tend to shut down within their first few years. They typically have small assets under management, relatively higher fees, and poor recent performance within their respective categories. Additionally, some caution should be used when selecting a fund provider. The provider's historical closures may be a useful consideration if they are linked to a firm's product development process. However, this may not be the case if a fund provider is changing in that process or pursuing acquisitions that may temporarily increase closures.

By identifying the common traits of shuttered funds, investors can more effectively identify--and avoid--those that are likely to close.

Editor's Note: This article was updated to correct the information about Invesco in the Fund Closures by Fund Provider exhibit.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)