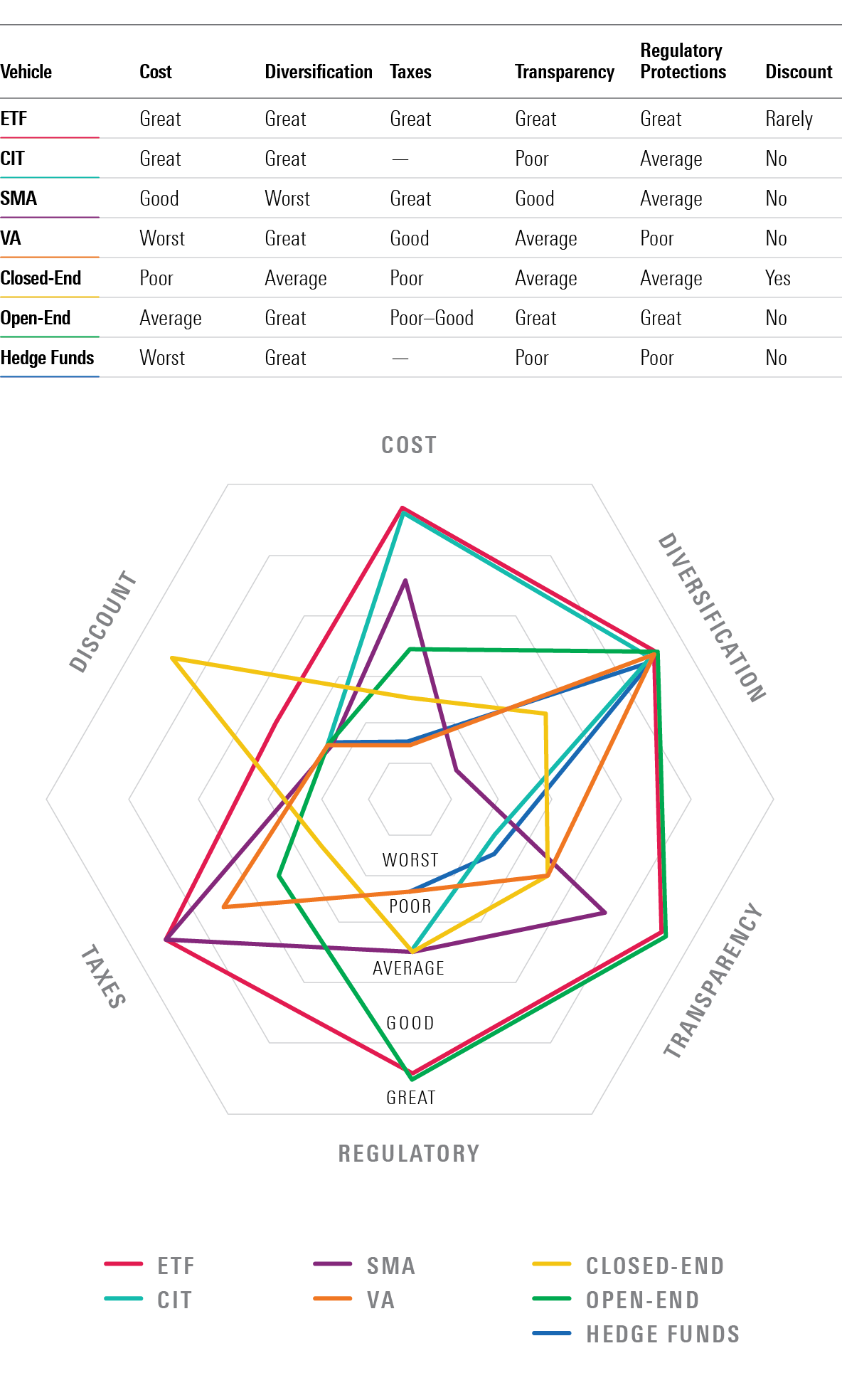

A Quick Survey of Investment Vehicles

From ETFs to CITs, investors have an array of choices. How do they stack up with mutual funds?

/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)

A version of this article first appeared in the December 2020 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting the website.

Mutual funds are largely the creation of the Investment Company Act of 1940, a well-crafted piece of legislation that set the groundwork for the massive growth in mutual funds. It helped to establish principles of transparency, fiduciary duty, and independent oversight that enabled trust to grow as fund companies grew up, too.

Some of the key things that helped funds to grow are daily net asset value, custodian holding securities, boards of directors, clear disclosure of holdings and fees, and SEC oversight.

But other investment vehicles are growing, too, so I thought I'd take a moment to explain what they are and how they stack up with mutual funds. I've also included a graphic showing the relative appeal of each versus mutual funds.

Source: Morningstar.

Exchange-Traded Funds ETFs are taking share from traditional open-end funds thanks to a couple of key attributes. ETFs trade throughout the day, and although ETFs are actually mutual funds governed by the '40 Act, they do some things differently. While individual investors buy and sell an ETF much like a stock, institutional investors can make arbitrage in-kind trades of the baskets of stocks if there is a price discrepency. This serves to keep the ETF's prices largely in line with net asset value, and it means the fund isn't realizing taxable gains every time someone redeems shares.

Thus, they trade on exchanges, but you get a price close to NAV in normal market conditions. For institutional traders, ETFs often take the place of futures for their short-term trading needs. Thus, you have a significant advantage for taxable investors versus an actively managed open-end fund, which will likely pay out capital gains in an up year. You still have to pay taxes if you sell at a profit, but it is unlikely you will along the way. The difference with open-end index funds from big companies isn't great, however, as they tend to realize losses in a way that spares shareholders capital gains payouts. There are exceptions where zombie index funds have spit out big bills.

That brings me to a misunderstood aspect of ETFs. People sometimes frame the open-end/ETF debate as active versus passive. But of course, there are many open-end index funds and about one fifth of ETFs are actively managed. So, when it is suggested that ETFs are cheaper than open-end funds, what is really being said is that passive is cheaper than active. But ETFs are generally also cheaper for having marketing costs stripped out. Some open-end passive funds are cheaper than their ETF counterparts.

Tellingly, Vanguard has both open-end and ETF versions of many of its index funds, and in general the ETF is 1 basis point cheaper. That cost edge is spurring flows from Vanguard's open-end share classes to its ETFs. ETFs have the advantage of not having to pay brokers a service fee. Yes, Vanguard provides services at cost, but the rest of the industry wants a profit.

As for active ETFs, one challenge is that the normal ETF structure requires a level of portfolio transparency that may enable front-runners for big equity strategies. New, less-transparent ETFs have come up to address this issue, but there isn't much gain to show for it.

Collective Investment Trusts CITs act very much like mutual funds only with different disclosure and regulation. They are pooled investments, but they don't have SEC filing requirements or boards of directors. As a result, they are usually cheaper than their mutual fund counterparts. On the downside, you lose transparency, but these are often very similar to a mutual fund. CITs are regulated by the Office of the Comptroller of the Currency and have to go through fiduciaries.

Typically, these are found in 401(k) plans and are run in very similar fashion to a mutual fund. So, you may want to use that mutual fund as a proxy in your portfolio-monitoring so that you can include it in top-down portfolio analysis and have some idea of how your CIT is performing.

Separately Managed Accounts These are another close cousin to mutual funds. They are sold in part based on exclusivity. Rather than pool your money with "commoners," you can have an SMA, which is managed for you--provided you have a million dollars to invest in the strategy. Minimums for SMA platforms and strategies vary by brokerage. Salespeople sometimes oversell this as a portfolio manager customizing a strategy for you, but this is mostly phony. For the most part, SMAs use the same cookie cutter, although you can ask to have something taken out such as tobacco or companies whose names start with the letter W.

SMAs do have a couple of real advantages, however. One is taxes. When you buy a mutual fund, you are buying into a strategy that may already have built up gains. When mutual funds distribute those gains, they go to everyone regardless of whether they have made a profit. So, you have to pay taxes if you hold that fund in a taxable account.

On the other hand, with the SMA, you start with a clean slate on taxes, and the securities are held in your account. You only have to pay taxes when the SMA manager sells your holdings at a profit. Given the currently elevated stock levels, that's a real benefit. No, it isn't tax-free. You'll still pay when SMAs realize profits and when you sell the SMA if it is at a profit, but at least you won't start out paying taxes. SMAs also tend to be cheaper because they are less regulated and have large account sizes. SMA fees are not set, so you will need to take a close look at the fee being offered and compare that with some mutual funds in the same strategy.

The one thing SMAs don't do well is bonds. That's because bonds trade in large amounts that can't easily be sliced up the way stocks can. As a result, bond SMAs tend to have focused portfolios of just 20-30 securities versus a portfolio of hundreds like the typical bond fund. Most people want their bond fund to provide income and a smooth ride, so having greater issue risk isn't a welcome trait. That goes double in high yield and other areas with real risk of default.

Closed-End Funds Closed-end funds are not so different from open-end mutual funds and ETFs except that the price you get will rarely be at net asset value. The funds can trade at discounts or premiums and thus add a rather unwelcome element of uncertainty. In general, closed-end funds trade at a discount to their NAV, which is a real bummer if you bought at the IPO.

Closed-end funds have a set asset base that the managers then run as they see fit. This means the fund isn't vulnerable to the impact of flows; this could help when it invests in less-liquid securities.

But there are disadvantages. There's less disclosure. Closed-end funds might change managers and then take their time in telling you. In addition, they cost more than most open-end funds because they have a fairly small asset base. But maybe the biggest disadvantage is that it's hard to fire the manager. Some closed-end funds appear to serve the function of providing the managers with a secure income stream as they don't run any other vehicles, nor do they have much incentive to do a good job as you can't actually withdraw money.

Finally, it's worth noting that closed-end funds can and do use more leverage than most mutual funds. If you see a big yield on a closed-end fund, it's because it is using leverage and is probably trading at a discount to NAV. There are some good firms, such as Pimco, running closed-end funds, so I'm not saying I would completely avoid them, but I would not want a closed-end fund to be a big part of my portfolio, and I would be sure it was run by a firm I really trusted.

Hedge Funds Hedge funds are a less regulated vehicle for very wealthy individuals and institutional investors. Although the name implies that they hedge away equity exposure, there are a wide variety of alternative and traditional strategies.

Some of the smartest minds in investing are at hedge funds. In particular, many of the best quantitative investors are in hedge-land because running a successful hedge fund can be insanely lucrative. The funds typically charge 2% of assets and 20% of profits. You can't do that in mutual funds because any performance fees have to swing both ways equally--and hedge fund managers don't want to subtract 20% of losses.

The bad news for individual investors is that the best strategies are either closed to new investors or just limited to big institutions. Generally, the stuff for investors with less than $100 million is the weaker stuff, and when you are paying fees like that, you need incredibly good stuff just to get anywhere close to what you'd get in a plain-old 60/40 low-cost allocation mutual fund.

Variable Annuities I've saved the worst for last. The most important thing to know about variable annuities is that they charge you a BIG commission. When advisors recommend a VA to you, they will mention the tax advantages, but what they are really thinking about is that BIG commission.

VAs come in a variable annuity policy with subaccount insurance fees inside. They are tax-advantaged structures that hold a portfolio of mutual funds. Unlike annuities, the value varies based on the underlying holdings. Some advisors have been critical of the use of VAs in 403(b) accounts, though the value to investors varies widely based on their needs and the quality of the VA.

Conclusion Regardless of the vehicle, it pays to keep tabs on costs and the quality of management. Most of the time, ETFs and open-end funds are the best options, but it's good to understand your choices and be open to better opportunities as they arise.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)