How the Analyst Ratings Could Change Under the New Approach to Assessing Funds

Downgrades would outnumber upgrades with costlier share classes likelier to take a hit.

/s3.amazonaws.com/arc-authors/morningstar/550ce300-3ec1-4055-a24a-ba3a0b7abbdf.png)

Executive Summary We recently announced our plans to update the methodology we follow in assigning Morningstar Analyst Ratings to mutual funds, exchange-traded funds, and other managed investments we cover. Here we examine the aggregate impact the methodology change would have if it were applied pro forma to U.S.-domiciled funds that have been assigned an Analyst Rating.

Study Approach To analyze the potential impact of the ratings enhancement, we applied the updated methodology pro forma to funds and ETFs that have been assigned an Analyst Rating. We did so by taking the funds' current People, Process, and Parent Pillar ratings and running them through the updated methodology. (For more information on the updated methodology is available here .)

After running the pillar ratings through the updated methodology, we compared those pro forma ratings against the existing Analyst Ratings and tallied up the results in the following impact analysis. It is worth noting that this pro forma analysis is subject to change, as analysts review their assumptions--including the pillar ratings they’ve assigned--in the normal course.

Key Takeaways

- Roughly 43% of funds and ETFs would see a rating change; many rating changes stem from tailoring ratings to each share class by taking fee differences into account.

- Downgrades would outnumber upgrades by a roughly 2-to-1 margin.

- The percentage of active funds rated Gold, Silver, or Bronze would fall; share classes that embed advice and sales fees also would see more downgrades than upgrades.

- The percentage of index funds earning Gold, Silver, or Bronze ratings would rise; in general, "unbundled" share classes would be likeliest to be named Morningstar Medalists.

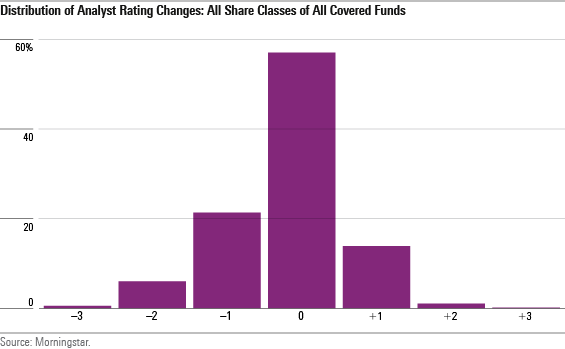

- Most ratings changes would be one rung and involve funds currently rated Bronze (45% of all changes), Silver (27%), and Neutral (17%).

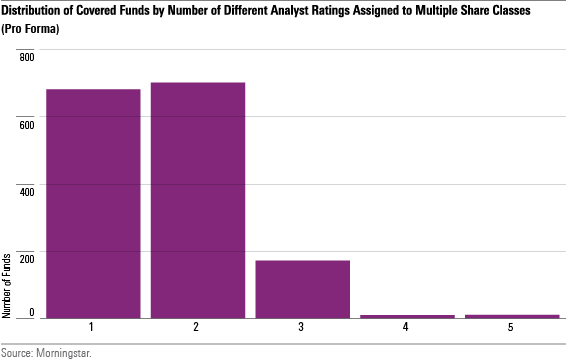

- Around half of funds with multiple share classes would see multiple ratings across the classes.

- Only about 26% of funds with above-average or high fees would receive Gold, Silver, or Bronze ratings, compared with around 50% today.

- Once implemented, we do not expect the updated methodology to result in more-frequent ratings changes than now.

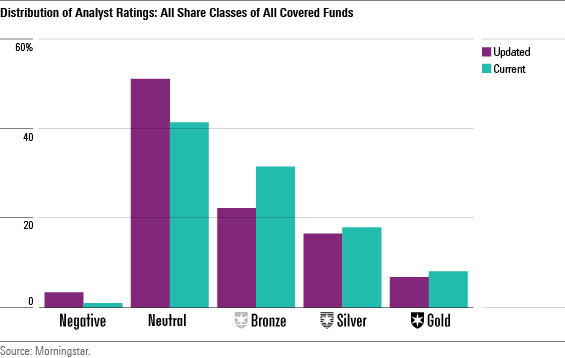

Impact Analysis: Big Picture Pro forma, the distribution of Analyst Ratings would shift away from Gold, Silver, and Bronze ratings, toward Neutral and Negative ratings under the updated methodology. Around 1,000 more share classes would receive Neutral and Negative ratings compared with today, with downgrades outnumbering upgrades by a margin of around 2 to 1. All told, roughly 43% of funds and ETFs would see a rating change.

This shift would stem at least partly from assigning Analyst Ratings to individual share classes. To this point, we have assigned the same rating to each of a fund’s share classes irrespective of fee differences. Going forward, we would vary the ratings we assign to share classes by taking these fee differences into account. All things being equal, more-expensive share classes of funds would receive lower ratings and vice versa for cheaper share classes.

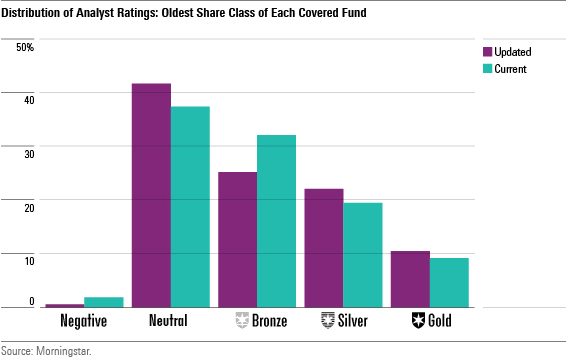

The effect of assigning ratings to individual share classes in this fashion becomes apparent when we remove multiple fund share classes from the analysis. When we limit to one share class per fund (that is, the share class tagged “oldest share class”), the distribution would shift toward Neutral and Negative but not quite to the same degree, with around 42% of funds receiving such ratings (versus 55% of all share classes).

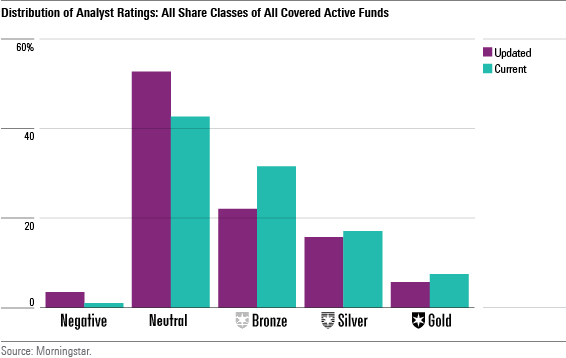

The distribution of Analyst Ratings assigned to active funds would shift in a way that mirrors the overall rated universe. This is explained by the fact that active funds dominate our coverage universe, accounting for roughly 96% of the share classes to which we have assigned Analyst Ratings.

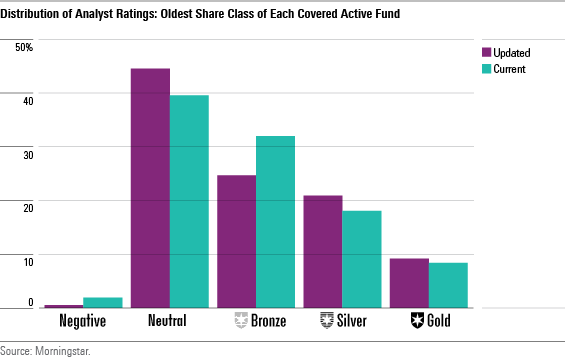

However, this shift would be less pronounced if we limit the analysis to one share class per active fund.

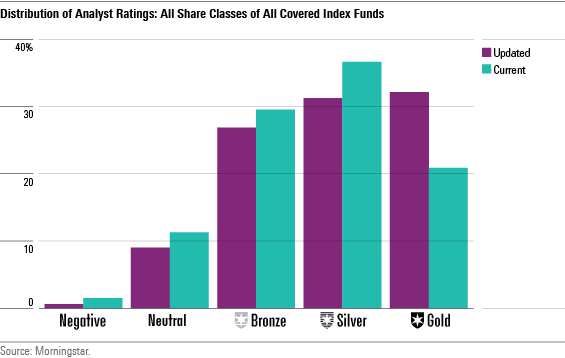

Unlike active funds, index funds would see more upgrades than downgrades under the updated methodology. The main reason for this is that the updated methodology further emphasizes low cost, which is a trait the index funds we cover often boast.

Impact Analysis: Detail We can drill down further to examine the potential impact of applying the updated methodology to rated funds.

By Rating

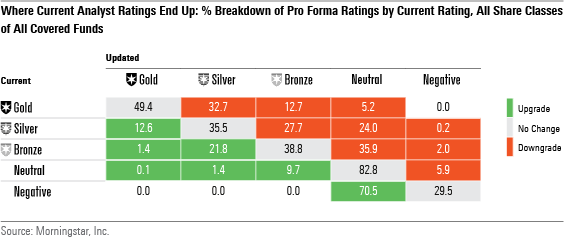

Though many fund share classes would retain the same Analyst Rating under the updated methodology, a significant number would see a rating change. Roughly speaking, 30% to 50% of funds rated Gold, Silver, Bronze, and Negative would keep the same rating. By contrast, more than 80% of share classes rated Neutral would retain that rating.

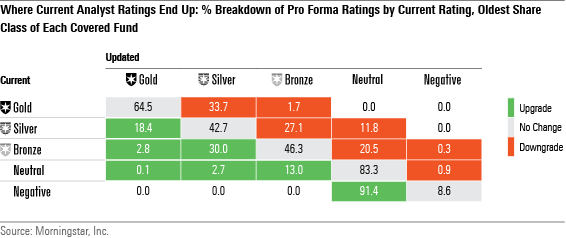

Many of the ratings changes would stem from assigning the Analyst Rating to individual share classes. (Today we assign the same Analyst Rating to all fund share classes, irrespective of fee differences.) This is evident when we remove multiple share classes, narrowing the analysis to one share class per fund.

More than 80% of share classes experiencing a ratings change would see a one-rung move, with changes from Gold to Silver, Silver to Bronze, Bronze to Neutral, and Negative to Neutral most commonplace.

- source: Morningstar Analysts

While the impact analysis did not assess the frequency of ratings changes under the updated methodology, we do not expect it to rise substantially. This is because ratings would change only when an analyst conducts a formal review, which typically happens on an annual basis. The updated methodology would not cause Analyst Ratings to change between formal analyst reviews.

By Fund

Formerly, we assigned the same Analyst Rating to all fund share classes irrespective of fee differences. Going forward, we’ll tailor ratings to each share class by taking those fee differences into account. This means that Analyst Ratings might vary across the share classes of a single fund.

We recently were assigning Analyst Ratings to 1,567 funds with multiple share classes. Under the updated methodology, we expect that 683 of those funds, or 44%, would receive the same Analyst Rating across the share classes. (In these situations, the fee differences between share classes aren’t so large as to pull costlier share classes into lower rating rungs.) 703 funds would receive two different Analyst Ratings across their share classes, and 181 funds would receive three or more different ratings.

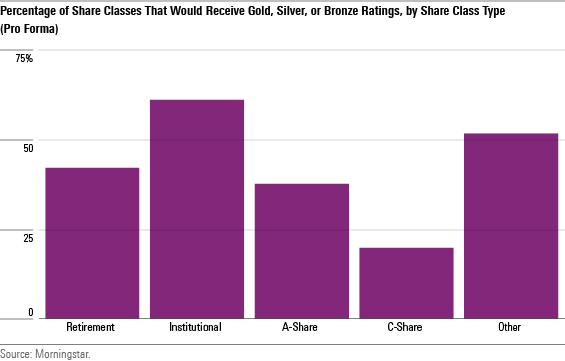

The chart below compares the percentage of share classes that would receive Gold, Silver, or Bronze ratings under the updated methodology, by major share class type. Institutional share class funds would be much more likely to receive a Medalist rating than other share types that embed various types of advice and sales fees.

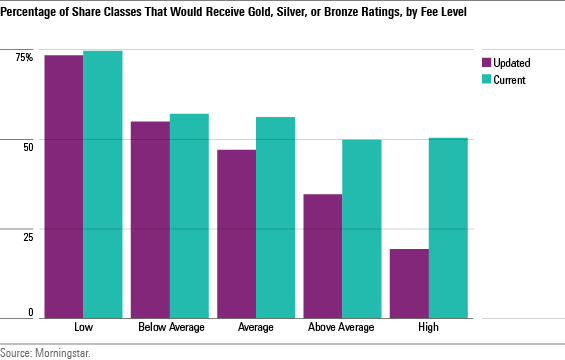

By Fee Level

The Morningstar Fee Level data point indicates how the cost of a fund share class ranks within the context of its broad peer group. It takes the form of Low (cheapest 20% of share classes), Below Average (next 20%), Average (middle 20%), Above Average (next 20%), and High (priciest 20%).

While fee level rank isn’t a direct input into the updated methodology, the impact analysis makes it evident that the more expensive a fund, the less often it would receive a Gold, Silver, or Bronze rating. Only around 26% of share classes with an Above Average or High rank would receive Medalist ratings, compared with about 50% today.

Conclusion This analysis is pro forma, as it takes the People, Process, and Parent Pillar ratings analysts have assigned to U.S. funds and runs them through the updated methodology. It goes without saying that this is subject to change, as analysts will be reassessing those pillar ratings in the normal course of reevaluating funds.

In the event analysts elect to lower their pillar ratings (subject to a ratings committee’s oversight and consent), then the distribution of Analyst Ratings could shift even more decidedly to Neutral and Negative. On the other hand, if analysts upgrade their assessments, then the distribution could shift in the other direction.

This process will unfold gradually, with a subset of the Analyst Ratings universe slated to be rerated under the updated methodology on Oct. 31, 2019, and the remainder over the 11 to 12 months that follow.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/550ce300-3ec1-4055-a24a-ba3a0b7abbdf.png)