Three ETFs Offering Exposure to Higher-Quality Corporate Bonds

These funds take different approaches to dialing down the credit risk inherent in this corner of the bond market.

/s3.amazonaws.com/arc-authors/morningstar/30aa6d58-cc92-46c5-8789-50161dc392a9.jpg)

Editor’s note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

The investment-grade corporate bond market has traditionally been a safe place for investors. Investment-grade credits have typically posed little credit risk and provided steady income streams. But a raft of new issues from lesser-quality credits have ratcheted up credit risk in this space.

There are several exchange-traded funds which seek to dial down credit risk relative to those tracking broad investment-grade credit market indexes. These funds present interesting choices for investors worried about deteriorating credit quality in this segment.

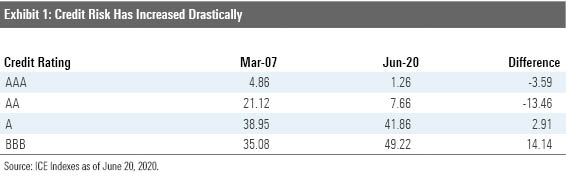

The State of the Investment-Grade Corporate Bond Market As of June 2020, the U.S.-dollar-denominated investment-grade corporate bond market (proxied by the ICE Bank of America US Corporate Bond Index) has a total market value of nearly $8 trillion. Nearly half that debt was issued by companies receiving a BBB credit rating--the lowest possible investment-grade credit rating. Exhibit 1 shows the credit quality makeup of the ICE Bank of America US Corporate Bond Index as of March 2007 and June 2020. The index's exposure to BBB-rated bonds increased 15 percentage points over the past 13-plus years. The investment-grade credit market of June 2020 is clearly characterized by a pronounced skew toward lower-quality bonds.

While there is the potential for this greater level of credit risk to manifest in incrementally higher returns, it isn’t a sure thing. What is certain is that it will translate into greater volatility and larger drawdowns. For example, during the coronavirus sell-off in the first quarter of 2020, the ICE Bank of America US Corporate Bond Index was crushed. It fell 7.47% in March 2020, marking its worst monthly performance ever dating back to January 1973.

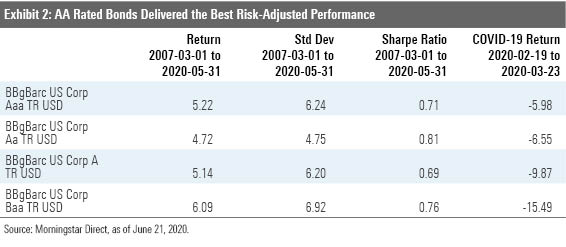

During the trailing 13 years through May 2020, the performance of each strata of the investment-grade space followed expectations (outside of the performance of AAA corporate bonds, which are few and far between). The lowest-rated bonds delivered the highest returns and the most volatility. But as seen below in Exhibit 2, AA rated bonds delivered the best risk-adjusted performance, as the pickup in volatility incurred by A and BBB rated bonds overshadowed their incrementally higher returns. The drawdown experienced by A and BBB rated bonds during the COVID-19 sell-off was also more severe than the drawdown of AA rated bonds.

Three Options for Less Credit Risk The simplest method to cut back on credit risk is to cut it out. That is what iShares Aaa - A Rated Corporate Bond ETF QLTA does. It tracks the Bloomberg Barclays U.S. Corporate Aaa - A Capped Index, which includes U.S.-dollar-denominated corporate bonds that are rated higher than BBB. The portfolio is market-value weighted.

Removing the lowest-rated issues leaves QLTA’s portfolio looking materially different than the broader investment-grade corporate bond market. As bonds representing half the value of the investment-grade credit market are rated BBB, QLTA isolates the most creditworthy half. There are clear benefits to this approach. It should help reduce volatility, shore up downside protection, and limit correlation to stocks. However, it also introduces greater sector concentration risk as it tilts heavily toward issuers from the financial sector, and limits upside potential.

There are other ways to lean toward higher-quality issues The ProShares S&P 500 Bond ETF SPXB takes an indirect approach. It tracks the S&P 500/MarketAxess Investment Grade Corporate Bond Index, which includes investment-grade U.S.-dollar-denominated bonds from publicly traded firms that are included in the S&P 500. Firms in the S&P 500 are typically large and have more resources to meet their obligations. Thus SPXB indirectly courts quality.

But by focusing on issuers within the S&P 500, the index cuts out a significant number of smaller issuers. In fact, as of the end of May 2020, bonds representing nearly 40% of the ICE Bank of America UC Corporate Bond Index were from issuers that are not included in the S&P 500.

While SPXB’s portfolio strategy is market-value weighted, it does not simply select every bond issued by a company in the S&P 500. Rather, it selects the 1,000 most-liquid bonds, as determined by their recent trading volume. Although the focus on liquidity does not address credit risk specifically, it could protect the strategy against large drawdowns during credit risk periods. Liquidity tends to dry up when credit risk spikes, which can cause the price of less-liquid bonds to fall further and faster than relatively more liquid ones.

SPXB has been consistently underweight the lowest-rated issues. As of May 2020, the fund’s exposure to these bonds was about 5 percentage points lower relative to the ICE Bank of America US Corporate Bond Index.

The Goldman Sachs Access Investment Grade Corporate Bond ETF GIGB, which carries a Morningstar Analyst Rating of Neutral, tracks the FTSE Goldman Sachs Investment Grade Corporate Bond Index. The fund presents a more-sophisticated approach to dialing back credit risk. Rather than rely on credit rating agencies, the strategy cuts credit risk via its own fundamental screening process. In selecting bonds, it eliminates bonds issued by the 10% of issuers from each sector with the most unfavorable year-over-year changes in operating margins and leverage (the two measures are averaged).

This is a sensible approach, as bonds’ upside potential is limited relative to their downside. Also, the market is generally faster to respond to new information than credit ratings agencies. Cueing off fundamentals as opposed for waiting for the ratings agencies to act may give it an edge in weeding out weaker credits. But while the strategy should deliver performance that is consistent with the broad investment-grade corporate bond market, its screening approach won’t necessarily lead to better performance over the long run. Market prices should reflect bonds’ risk. It isn’t clear that the market systematically overvalues bonds with deteriorating leverage and operating margins.

Perhaps the best thing GIGB has going for it is that it minimizes the amount of active risk it takes. For example, the strategy is a few percentage points underweight exposure to BBB rated bonds but has otherwise kept its exposure in line with the broader market. This means that it should deliver market-like performance with marginally less risk over the long term.

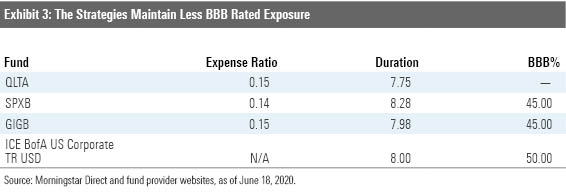

Exhibit 3 presents a peek at each fund’s credit and interest-rate risk exposure. as well as data for the ICE Bank of America U.S. Corporate Bond Index.

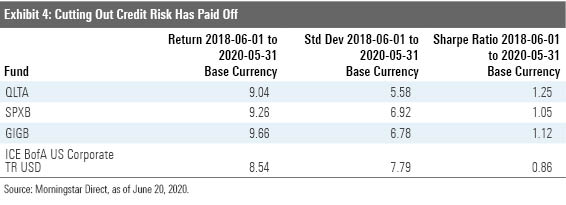

How These Funds Have Fared Each of the funds has performed well dating back to SPXB's May 2018 inception. As seen in Exhibit 4, they each delivered better risk-adjusted performance relative to the ICE Bank of America U.S. Corporate Bond Index over this span.

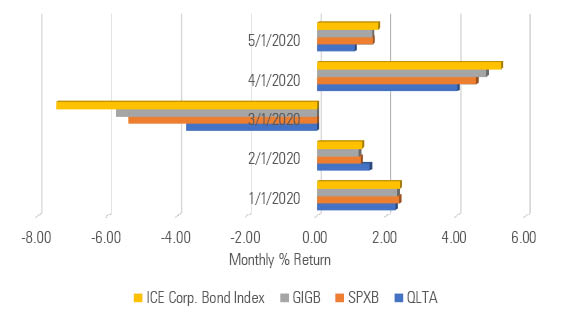

All three funds outperformed the index while exhibiting less volatility. The fact that they demonstrated less volatility is not surprising, nor is their performance relative to the benchmark. Cutting back on credit risk helped these funds to hold up better than their category peers and the category index during the COVID-19 sell-off.

Investors were punished for taking credit risk during the crisis. This explains why QLTA held up the best, as BBB rated bonds performed the worst. SPXB’s focus on the largest issuers also appeared to help. And GIGB’s fundamental screen helped it avoid some of the worst performers, including the fallen angels that were downgraded from BBB to a speculative-grade rating during the crisis.

Exhibit 5 illustrates the monthly returns for each of the strategies, as well as the ICE Bank of America Corporate Bond Index, from January 2020 through May 2020.

Exhibit 5: 2020 Monthly Returns Through June

Source: Morningstar Direct, as of June 22, 2020.

While these funds fared well during the crisis, it wouldn’t be reasonable to expect them to deliver better returns relative to the broader investment-grade bond market over the long term. That said, their relatively higher-quality portfolios should reliably ratchet down risk and might help investors sleep better at night when bond markets are as nightmarish as they were earlier this year.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/30aa6d58-cc92-46c5-8789-50161dc392a9.jpg)