Portfolio Concentration Has Little Sway on Returns

A recent Morningstar study found that high-conviction managers haven't outperformed their better-diversified counterparts.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

Investing with a high-conviction manager may sound prudent. Watering down exposure to a manager’s best ideas seems like it would only lead to mediocre performance, making it harder to recoup active fees. But increasing portfolio concentration also increases the risk of missing out on some of the market’s big winners, which have historically driven a disproportionate share of its returns.

A recent study I published shows that, in practice, these factors appear to offset. There isn't a significant relationship between portfolio concentration and gross returns among U.S. equity mutual funds. Yet, concentrated managers tend to charge more, and the risk of manager selection is greater for these funds because of the wider range of potential returns between winners and losers. Investors in concentrated funds should be mindful of the risks and not give managers much leeway on fees.

Research Design This study measured the potential relationship between portfolio concentration and performance by grouping actively managed funds in each Morningstar Category into quartiles based on the percentage of assets they invested in their top-10 holdings at the end of each year. It then tracked the gross returns (which controls for differences in fees) of each group over the next 12 months before updating the group assignments. This analysis included nonsurviving funds and used the original category assignments as of each sorting date.

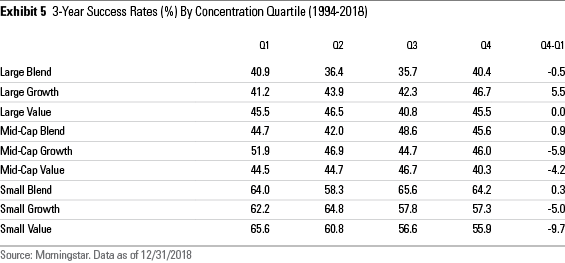

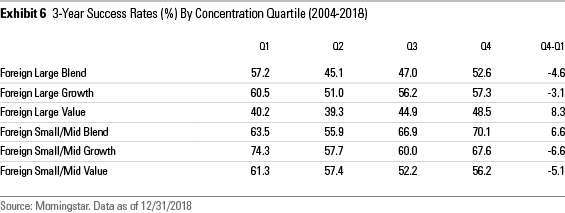

To assess the odds of finding high-performing managers in each group, the study also calculated success rates for the funds in each quartile over a 12-month holding period, and again with a 36-month holding period. This is defined as the number of funds that survived and outperformed the respective benchmark for each category over each holding period, divided by the number of funds on the sorting date, which is the start of the period.

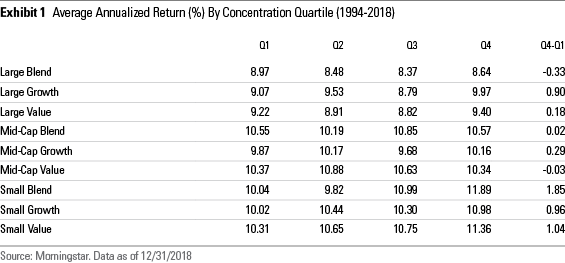

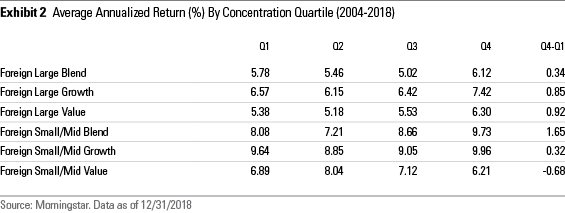

Higher Concentration Doesn't Improve Performance The most-concentrated quartile of funds (labeled Q4) generated higher annualized gross returns than the least-concentrated quartile (Q1) in seven of the nine U.S. equity categories from January 1994 through December 2018. Similarly, the most-concentrated quartiles posted higher returns in five of the six foreign stock categories from 2004 through 2018. However, none of the return differences between the most- and least-concentrated quartiles were statistically significant. This means there isn't clear evidence that these results were due to anything other than chance. In many cases, the results weren't economically significant either. The results are shown in Exhibits 1 and 2.

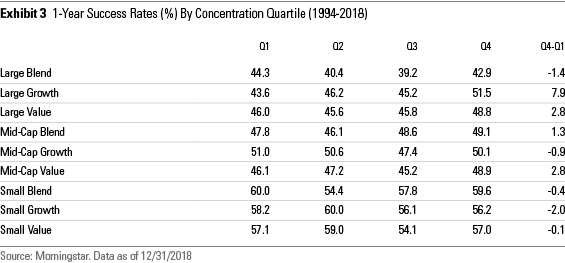

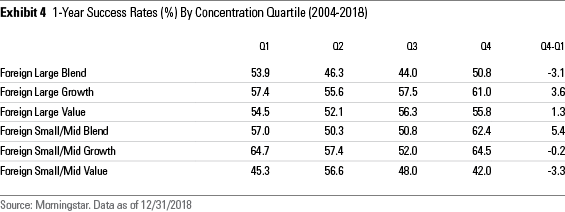

Similarly, the most highly concentrated managers didn’t have significantly better success rates than the least-concentrated, as shown in Exhibits 3-6. It was split roughly in half as to whether the most-concentrated or least-concentrated funds did better. But in all cases, the difference in success rates between these quartiles landed within 10 percentage points, adding further evidence that there isn’t a significant relationship between portfolio concentration and the odds of beating the market.

Risk Even though concentrated managers don't have higher odds of success, the potential opportunity cost of choosing a poor manager increases with portfolio concentration. That's because concentrated portfolios have a wider range of potential returns than their counterparts who are more broadly diversified.

Return volatility is another potential risk that could increase with portfolio concentration, because of the additional exposure to firm-specific risk. However, this study found that in many of the categories, funds in the most-concentrated quartiles only exhibited slightly greater volatility than the least-concentrated. And in three of the foreign stock categories, the most-concentrated funds exhibited lower volatility than the least-concentrated ones. In those categories, the most-concentrated managers were able to partially offset their higher idiosyncratic risk by taking less market risk than their better-diversified counterparts, which they can accomplish by favoring more-defensive investments or carrying larger cash balances.

Firm-specific risk isn’t rewarded on average, so it’s important to ensure that concentrated managers are taking appropriate steps to manage it. Pay attention to portfolio volatility and market beta to assess whether those steps have been effective.

Fees While there was not a significant relationship between concentration and gross returns, the most-concentrated funds tended to charge higher fees than the least-concentrated ones did. This is consistent with the idea that investors are willing to pay up a bit for bolder active bets. However, this study suggests that it may not be worth paying a premium for a concentrated, high-conviction portfolio, since it did not find evidence that higher concentration leads to better performance.

Exercise Caution with Concentrated Portfolios The idea that investing with conviction improves returns is a myth. Increasing portfolio concentration is just as likely to hurt returns as it is to help. Concentrated funds charge more, but don't have significantly better odds of success (before fees) than their better diversified counterparts. Investors in these funds have greater exposure to idiosyncratic risk, which isn't compensated on average. And the cost of selecting the wrong manager is greater here, so proceed with caution.

Click here to read the full paper.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)