Momentum Often Loses Steam in Practice

Momentum may not work as well in practice as on paper, but well-constructed momentum funds still have a good chance to beat the market.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

A version of this article previously appeared in the August issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

Momentum investing is sound in theory but often disappoints in practice. This strategy is based on the tendency for recent performance to persist in the short term. On paper, simple momentum strategies that target stocks with strong returns over the past year seem to work well. But they ignore real-world frictions, like trading costs and taxes, and often look quite different from momentum funds investors can buy.

While momentum has continued to work on paper in recent years, most broad large- and mid-cap U.S. momentum funds have underperformed the Russell 1000 Growth Index. (This is an appropriate benchmark because most momentum funds have a growth tilt). And though few of these funds have been around for a decade, none has managed to beat that benchmark over that horizon.

Momentum investing can succeed in practice, but portfolio construction choices and fees matter--a lot. The best funds balance transaction costs against momentum style purity, effectively capture the momentum effect documented in the academic literature, and consider risk.

A Promising Idea At first blush, momentum investing may seem foolish. It ignores fundamental data, valuations, and warnings that past returns aren't indicative of the future. Most momentum strategies rely entirely on recent performance to select investments, which is antithetical to fundamental value and passive index investing.

Yet momentum has been widely documented in academic literature, showing up in all asset classes and in most markets. The best explanation for this effect is investors are slow to react to new information, causing prices to adjust more slowly than they should.

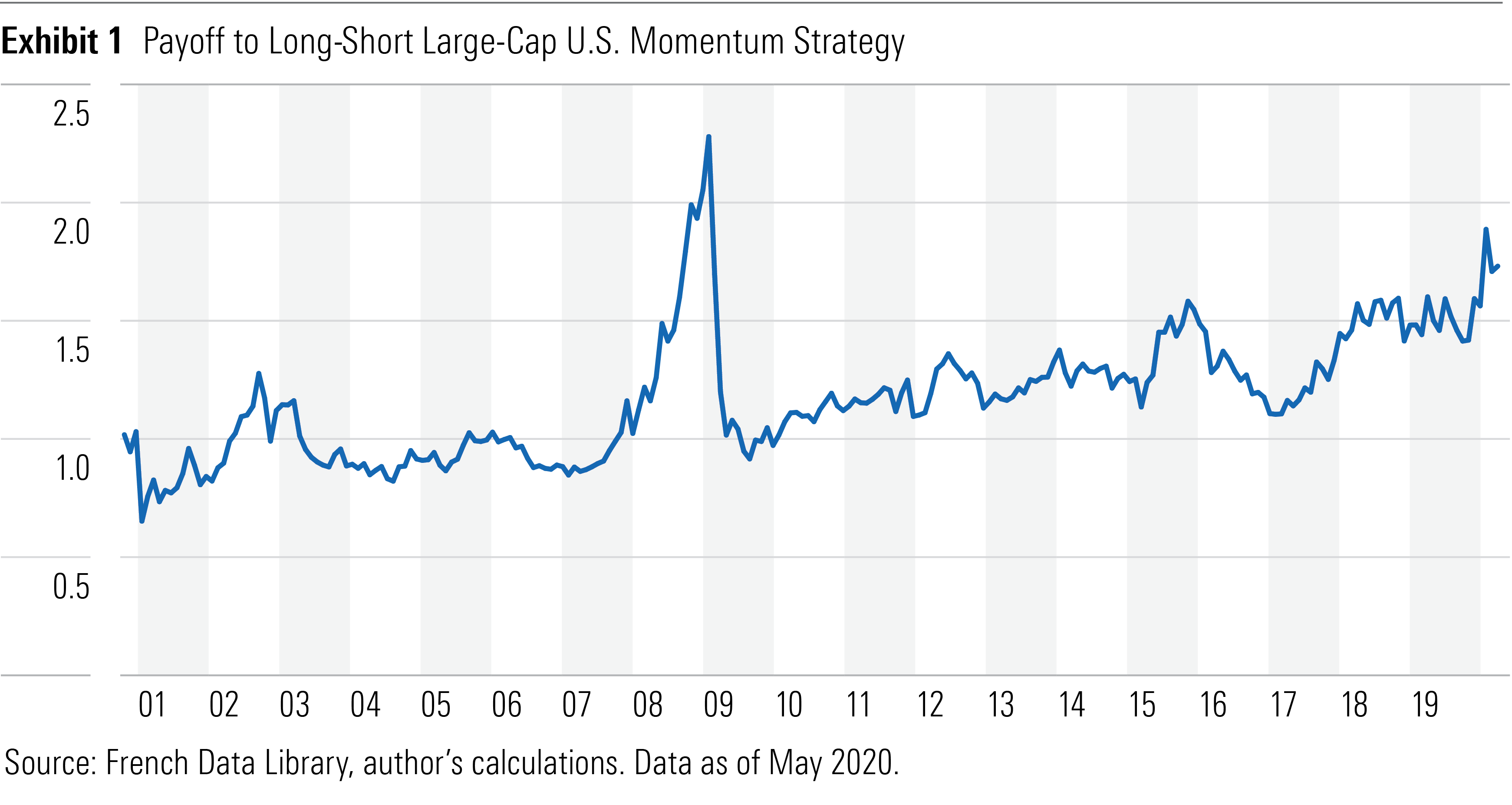

Exhibit 1 illustrates the theoretical payoff to a long-short momentum strategy among the largest quintile of U.S. stocks, similar to the size orientation of the Russell 1000 Index. Each month, it goes long the quintile of stocks from that group with the highest returns over the past 12 months (excluding the most recent one), weighted by market cap, and shorts the quintile with the lowest returns over that period.

This would have been a successful albeit risky strategy. From the end of October 2000 through May 2020, this strategy would have returned 2.79% annually before transaction costs. As this is a long-short strategy, a positive return like this is a success.

That said, this momentum strategy experienced severe losses when the market rebounded in 2009. During that time, stocks with the worst returns over the past year rebounded the most, hurting momentum. Of course, most investors can’t stomach this level of risk, ignore transaction costs, or short stocks. Thus, momentum funds on the market typically look quite different from this theoretical construct.

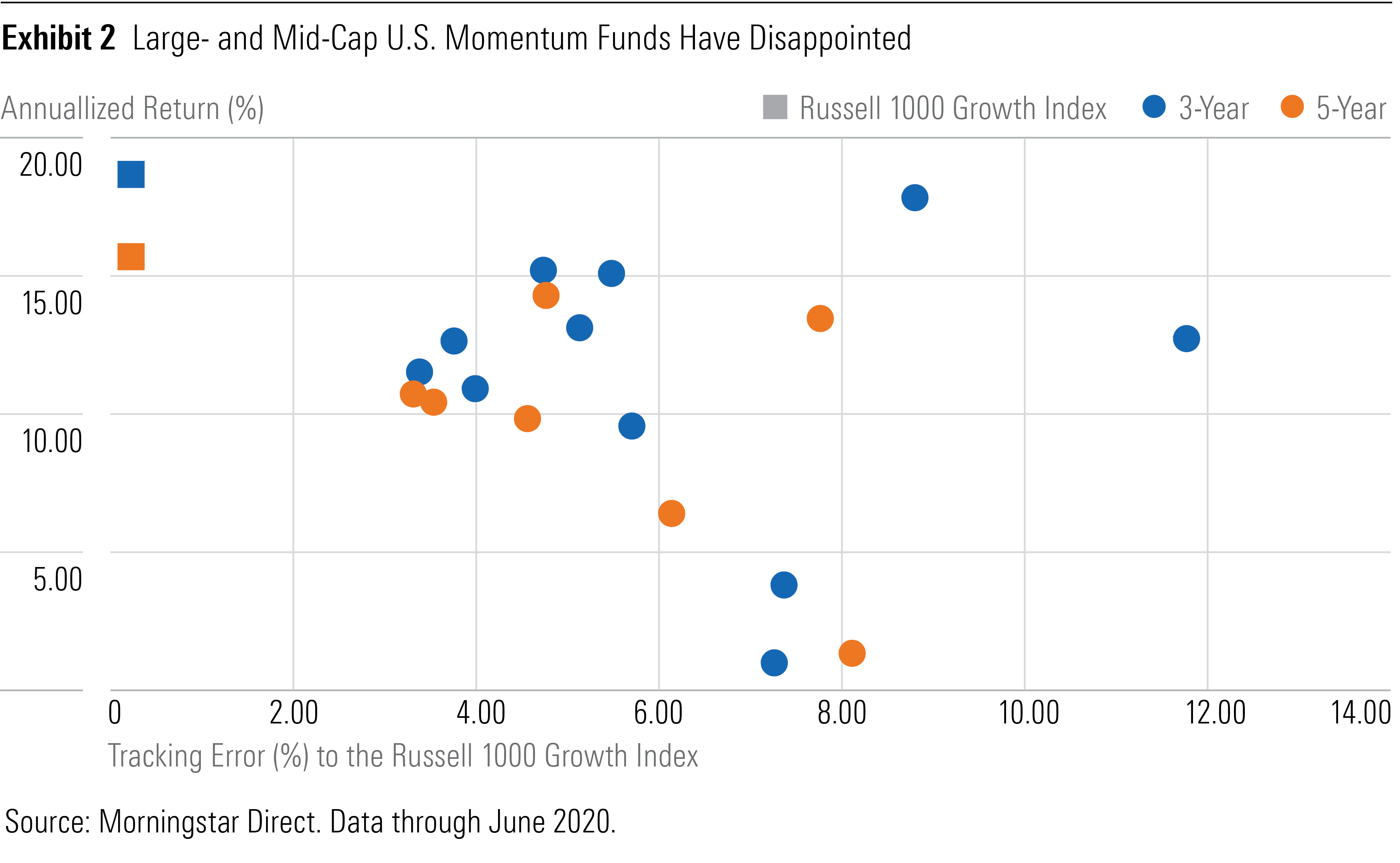

Disappointing Results While this theoretical long-short momentum strategy paid off, most broad, long-only large- and mid-cap U.S. momentum funds have disappointed. While some have beaten the market, most have a growth tilt and have fared less well against the Russell 1000 Growth Index. In fact, they all lagged that benchmark over the trailing three- and five-year periods through June 2020, as shown in Exhibit 2. During that time, the theoretical momentum strategy continued to pay off.

As this exhibit illustrates, there was a wide range in returns and active risk (as measured by tracking error against the Russell 1000 Growth Index) among these funds. That’s because there are important differences in portfolio construction, ranging from how they define momentum to how aggressively they pursue it.

Lost in Translation Clearly, something is getting lost in translation. This isn't entirely because of the practical challenges of implementing momentum, like transaction costs or these funds' long-only portfolios, though those factors play a role. Most of these funds have only modest exposure to the classic academic factor, which helped performance but wasn't enough to overcome other headwinds. These include stylistic differences between these funds and the Russell 1000 Growth Index and fund-specific considerations (alpha).

Most of these funds faced stylistic headwinds. For example, during these periods traditional growth investing paid off handsomely, but most of these funds had less-pronounced growth tilts than the Russell 1000 Growth Index, which hurt performance.

That said, momentum investors shouldn’t sweat underperformance that comes from stylistic differences between a fund and its benchmark, like differences in size and growth orientation or market risk. Those differences are largely unrelated to the efficacy of the momentum strategy.

Stripping out the impact of non-momentum style tilts, only two of seven funds would have outperformed over the trailing five years through May 2020 (Invesco S&P MidCap Momentum ETF XMMO and iShares Edge MSCI USA Momentum Factor ETF MTUM). And only three of 11 would have outperformed over the past three years (Invesco S&P 500 Momentum ETF SPMO, MTUM, and XMMO).

Many of the other funds underperformed considerably after controlling for their style tilts (they had negative alphas). This is partially attributable to fees, transaction costs, and unique portfolio construction choices that didn’t pay off during this time. However, it’s important not to read too much into a fund’s alpha over a short period, as alphas tend to fluctuate considerably over time. Instead, it’s better to focus on each fund’s portfolio construction approach and how well it harnesses the classic momentum effect.

None of the momentum funds in this group follow the same portfolio construction approach as the classic momentum factor, which tends to dilute their exposure to it. For example, many rebalance less frequently than once a month and apply buffers to mitigate transaction costs. Others make risk adjustments in their stock-selection approach.

That’s not necessarily bad. Those adjustments could improve performance and lead to more-practical portfolios that investors can stick with. However, this underscores that it is not appropriate to assume all momentum funds equally benefit from the classic momentum effect. They require further due diligence.

Best Practices The best momentum funds effectively capture the standard momentum effect documented in the literature while taking steps to mitigate transaction costs and risk. SPMO and MTUM, which has a Morningstar Analyst Rating of Silver, do well on these fronts. And both charge low fees.

SPMO achieves strong exposure to the standard momentum factor, despite rebalancing only twice a year and applying buffers to mitigate turnover. It does this by narrowly focusing on the quintile of stocks in the S&P 500 with the strongest risk-adjusted momentum over the past 12 months, excluding the most recent one. It further strengthens this exposure by weighting stocks according to both the strength of their momentum and market capitalization.

This risk adjustment points the fund toward stocks whose momentum is more likely to persist and reduces its exposure to cyclical stocks during market rallies, which tend to get hit harder than most during market downturns. This should improve performance when the market turns, though it isn’t a panacea.

MTUM takes a similar approach to SPMO. Like its peer, MTUM attains strong exposure to momentum by casting a narrow net around momentum leaders and incorporating momentum strength into its stock weightings. MTUM uses a longer three-year lookback period to measure risk than SPMO. It favors stocks with strong returns over the past seven and 13 months (excluding the most recent one), relative to their longer-term risk. This is less about momentum quality than it is about reducing the portfolio’s risk. However, the two funds have exhibited similar risk.

Similar to SPMO, MTUM refreshes just twice a year and applies buffers to mitigate unnecessary turnover. Spikes in market volatility can trigger off-cycle rebalancing, during which the fund focuses only on its shortest-term performance signal. This should help by allowing the fund to use the most recent returns available, which is more likely to persist when market conditions are changing than older data.

Not all momentum funds deliver potent exposure to the classic momentum factor, which limits how much they benefit when that factor pays off. Among these is SPDR Russell 1000 Momentum Focus ETF ONEO. This fund starts with the Russell 1000 Index and adjusts its weightings to favor stocks with strong quality, low valuations, small size, and strong momentum. While the fund places the greatest emphasis on the momentum adjustment, it has very weak exposure to the classic momentum factor. That’s partially because its value and small size tilts tend to favor stocks with poor momentum, which offsets its momentum tilt. Quality stocks may not always have strong momentum.

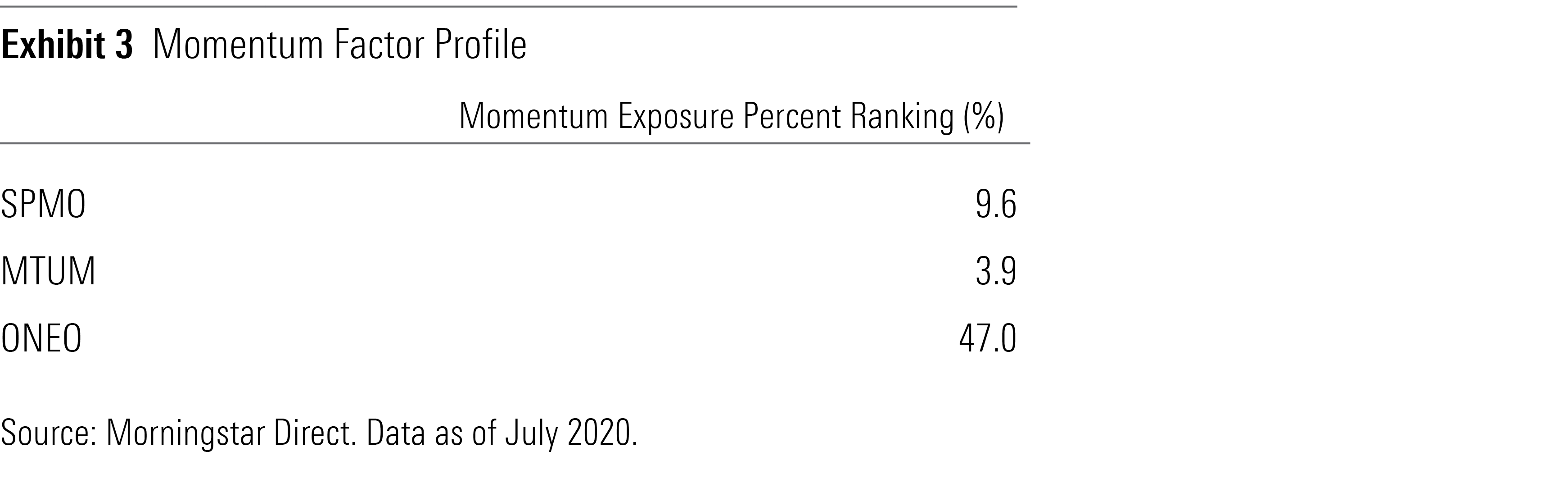

Morningstar’s Factor Profiles (on each fund’s Morningstar.com Portfolio tab) offer an easy way to compare exposures to the classic momentum factor. They show how a stock fund’s factor exposures rank relative to the universe of U.S.-listed funds, based on its current holdings. Exhibit 3 illustrates the momentum exposures for SPMO, MTUM, and ONEO from their factor profiles.

Factor strength alone isn’t the end goal. Potent factor exposures often come with high risk. However, this can be a helpful tool to gauge whether a fund is delivering the exposure it targets. If a fund delivers strong exposure to momentum while mitigating turnover, risk, and fees, it has a good chance to succeed.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)