Why You Should Still Care About Inflation

Inflation hasn't been much of an issue lately, but it's still a long-term threat.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

Editor's note: A version of this article was initially published on May 19, 2020.

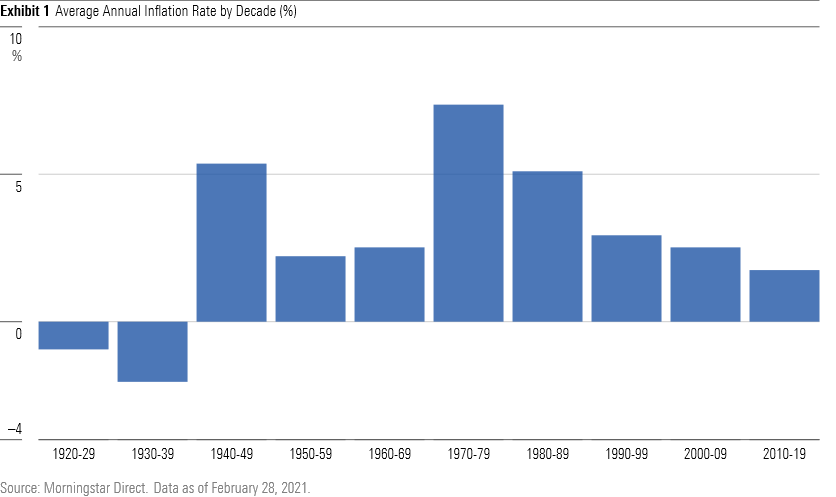

It’s fair to say that inflation has been pretty much a non-issue for a long time. I have vivid memories of hearing dire warnings about rising energy prices during my childhood in the 1970s, but since then, inflation has been in a secular decline. In fact, average inflation rates by decade have gradually stepped down, from 7.4% in the 1970s, to 5.1% in the 1980s, to 2.9% in the 1990s, to 2.5% in the 2000s, and just 1.8% in the 10 years ending in 2019. Inflation rose only 1.4% in 2020.

While inflation has ticked up slightly in recent months, there are reasons to believe it could stay low. For one, the Federal Reserve has an explicit inflation target of 2%, which it officially established in 2012. The Fed uses inflation forecasts relative to this target, along with other economic data, as part of its decision framework for making changes to short-term interest rates. The Fed recently modified its policy to allow for higher inflation rates until the economy gets back to full employment, but it probably won’t let inflation run unchecked for multiyear periods.

Ongoing economic weakness in the wake of the global coronavirus pandemic is another factor that would likely keep inflation in check. Even with a gradual easing of lockdown restrictions, it’s not clear whether consumers will return to previous levels of spending in areas like travel, dining out, and entertainment. In addition, wage growth is a major component of inflation. Even if the economic recovery continues unabated, the historically high unemployment rate may help tamp down inflation over the next few years.

While the overall economic environment probably points to inflation remaining low, there are still pockets of inflation here and there. Prices for oil and gas have increased significantly so far in 2021, and food costs (for both groceries and dining out) were up about 3.6% year over year through the end of February. Prices for durable goods and home improvements have also increased--a trend that may continue as individuals look to spend newfound cash from the “helicopter money” of stimulus payments. More money chasing the same amount of goods and services, by definition, leads to higher inflation.

Learning From History

There are some historical precedents for higher inflation in the wake of fiscal and monetary stimulus. Following Franklin Delano Roosevelt’s election as president in 1932, his New Deal policies vastly increased government spending in an attempt to pull the economy out of a devastating depression. As spending increased, the deflationary trend from 1930 to 1933 was followed by a return to more normal inflation rates from 1934 to 1937. Inflation showed a more dramatic increase after a surge in defense spending caused the federal deficit to balloon during World War II. Annual inflation rates averaged about 10% per year in the three years after the war.

The scale of recent government spending dwarfs that of nearly every other period. The government stimulus package has already totaled more than $5 trillion, and Congress will likely expand that amount in the coming months. At the same time, the Federal Reserve has been aggressively purchasing bonds and reducing interest rates. This increase in money supply is a textbook cause of higher inflation because it decreases currency values.

Granted, many market observers predicted higher inflation rates in the wake of aggressive fiscal and monetary stimulus in 2008, but that didn’t materialize. And while expectations for breakeven inflation rates have increased, the market is currently pricing in five-year inflation rates of 2.5%, which is still pretty benign. However, it’s worth noting that the scale of recent spending is far larger than what the government spent during the global financial crisis. In addition, it’s possible that supply/demand imbalances could lead to higher-than-expected inflation if a resurgence in consumer demand coincides with supply disruptions and depressed levels of production in the wake of wide-scale economic shutdowns.

Portfolio Implications

Because we ultimately don’t know how inflation will shake out, it’s prudent to carve out a portion of your portfolio to guard against different scenarios. In periods of deflation or disinflation, cash and Treasury bonds typically perform well.

On the flip side, Treasury Inflation-Protected Securities are the most straightforward way to protect against a potential increase in inflation. TIPS guard against inflation in two ways. First, their principal value is tied to changes in inflation. Second, their coupon payments are also adjusted based on changes in the principal value. In periods of higher inflation, TIPS pay out more interest and also increase in par value. At maturity, the U.S. government will pay back either the adjusted par value or the original principal, whichever is higher.

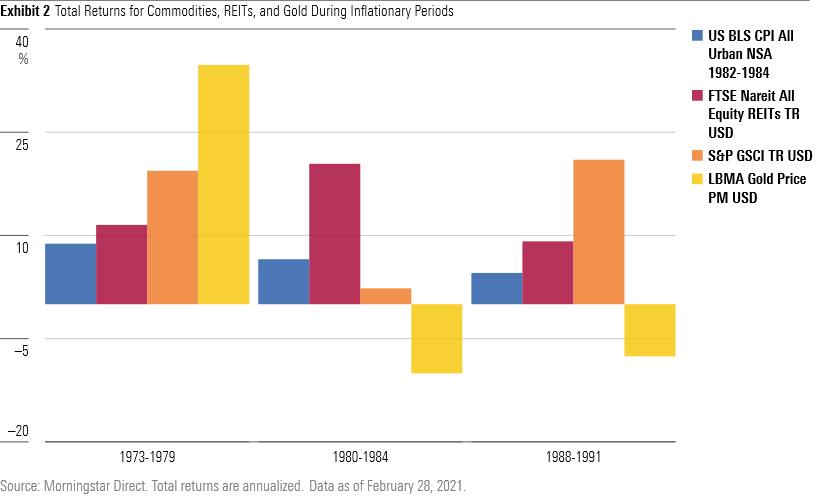

It’s tough to get a handle on other asset classes to use as an inflation hedge simply because we haven’t seen periods of high inflation in recent history. But looking back on some previous inflationary periods helps shed some light on which asset classes have performed best as inflation hedges.

As shown below, commodities have the most consistent record as inflation hedges. This makes sense, because the Consumer Price Index is partly based on commodity prices. Of the three asset classes we looked at, only commodities showed a significantly positive correlation with inflation. All else being equal, that suggests that commodity prices tend to move in the same direction as inflation (although not always to the same degree).

Real estate investment trusts have also fared relatively well. Because property owners have historically been able to pass along most increases in their underlying costs to tenants by raising lease prices, real estate boasts a built-in inflation hedge. It can also benefit from greater demand during periods when surging economic growth leads to higher inflation. (It’s not clear whether this will remain the case going forward if the pandemic prompts companies to adopt more-permanent work-from-home policies, though.)

Gold is often touted as an inflation hedge, but it actually has a pretty low correlation with inflation. Its performance record is decidedly mixed: In some years with higher inflation, it has shot the lights out, but in other years, it’s been a dud.

From a portfolio construction perspective, it’s worth carving out a small portion of a portfolio for assets that can help counter inflation. Of the three asset classes shown above, commodities probably have the strongest case as an inflation hedge. However, commodities have also shown the highest levels of volatility (as measured by standard deviation) among the three and have also been subject to large drawdowns. In fact, previous academic research has found that adding commodities to a diversified portfolio can improve risk-adjusted returns over time, but that pattern has not played out in recent history. Therefore, adding commodities to a portfolio as an inflation hedge requires a bit of a leap of faith as well as a tolerance for risk.

A less-risky way to guard against inflation risk is by increasing a portfolio’s equity exposure. It’s important to note that stocks aren’t really a direct hedge against inflation. In fact, the correlation of broad equity market benchmarks with inflation is close to zero. Instead, stocks can help offset the erosion of purchasing power from inflation simply because they generally offer better long-term returns than other asset classes. Because of this, their real returns (nominal returns minus inflation) should be higher than those of other asset classes over longer periods.

On the fixed-income side, in addition to buying TIPS, investors might also want to tweak their other fixed-income holdings. By staying toward the shorter end of the maturity spectrum, investors can guard against the inflation risk inherent in longer-term bonds, particularly now that interest rates are at a historical low.

Conclusion

When it comes to inflation, it would be easy to get lulled into a sense of complacency by looking at recent history. Taking a longer-term view, though, it’s worth considering the possibility that inflation could eventually return to less-benign levels. If that happens, portfolio diversification should once again prove its merits.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/XF7WENSYN5BFBFLPPFH7BJYUHE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)