Are Bond Investors Making a Mistake by Bailing Out?

The scale of this year’s outflows suggests panic may be prevailing.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

There’s no question that 2022 has been a horrible year for bonds. As the Federal Reserve has hiked interest rates to try to get inflation under control, bonds have suffered some of their worst losses in decades. In the first six months of 2022, for example, the Bloomberg U.S. Aggregate Bond Index dropped 10.35%—its worst showing in more than four decades.

But fixed-income securities still play a critical role in reducing portfolio risk and can also prove surprisingly resilient, even during periods of rising interest rates. In this article, I'll expand on why selling off bond holdings can be particularly detrimental.

Heading for the Exits

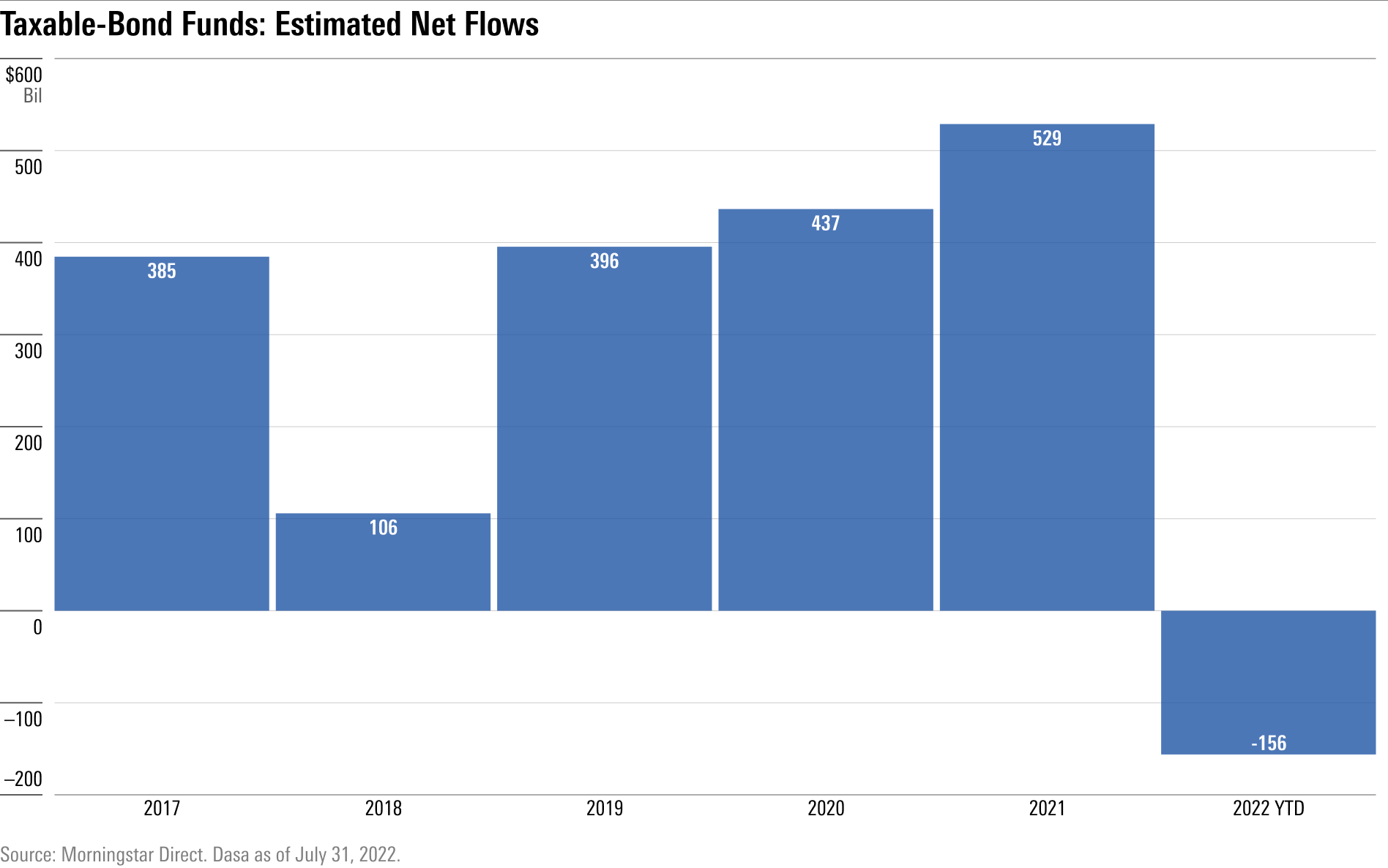

For the year-to-date period through July 31, 2022, net outflows from taxable-bond funds were $156 billion, about 5.4% assets from year-end 2021. That's a dramatic turnaround from the large inflows into taxable-bond funds over the past few years.

Taxable- Bond Funds: Estimated Net Flows

Bond-fund investors have also sold off during some previous bond-market jitters. A series of several interest-rate hikes—along with other events such as the Mexican peso crisis—spooked investors in 1994. Estimated net outflows totaled about $49.3 billion for the year, or about 13% of the previous year-end assets in percentage terms.

Following the bond market's dip in 1999 (driven by rising yields amid robust economic growth and expectations for higher inflation), taxable-bond-fund investors sold an estimated $34.0 billion in 2000, or about 6.6% of assets in percentage terms.

The Problem With Outflows

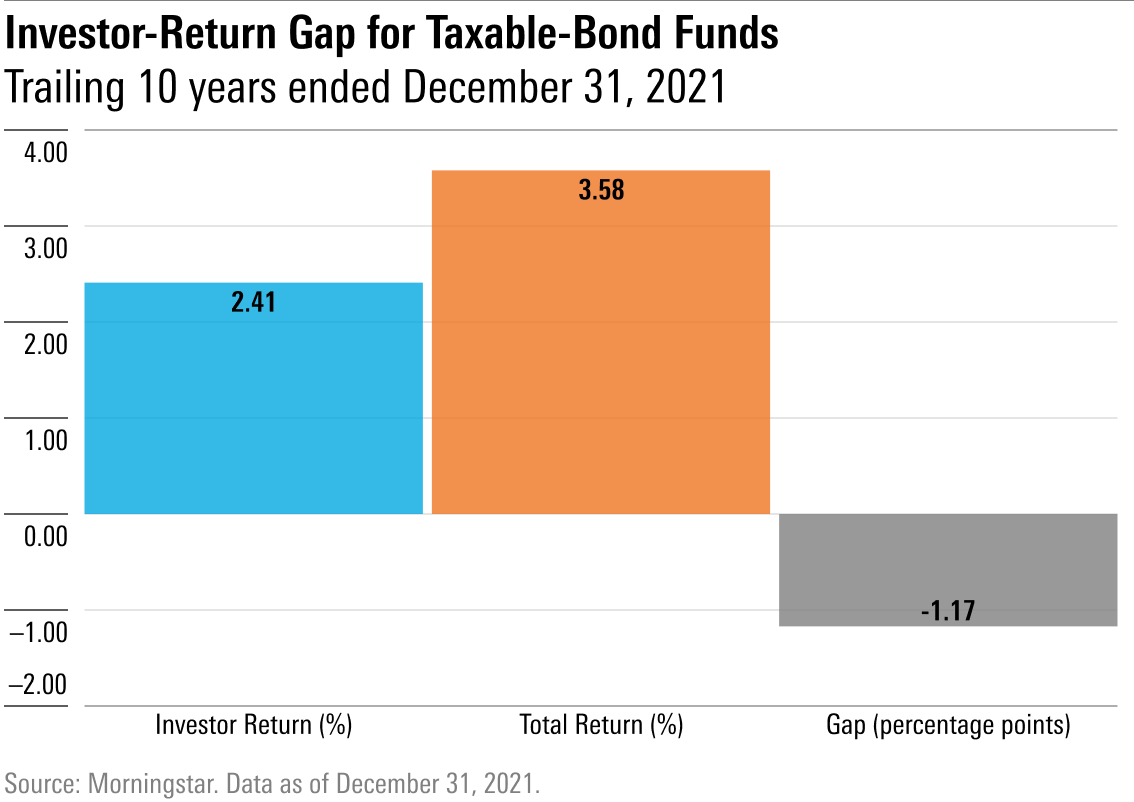

While significant fixed-income outflows aren't all that common, they can still be problematic. In our annual "Mind the Gap" study of investor returns, we look at the impact of cash flow timing on fund investors' actual results. The difference, or gap, between investor returns and reported total returns represents the amount investors gave up because of poorly timed purchases and sales.

For taxable-bond funds, we found that investor returns lagged total returns by 117 basis points, on average, for the 10 years ended Dec. 31, 2021. On the surface, that's actually better than the 1.7-percentage-point return gap across all category groups. But the low level of returns for taxable-bond funds makes this return gap particularly damaging. Over the trailing 10-year period, total returns averaged only about 3.6% per year, and investors missed out on about a third of those returns, earning only 2.4% per year in dollar-weighted terms.

Investor-Return Gap for Taxable-Bond Funds

But what if investors are making the right call by bailing out? After all, the Federal Reserve has said that it plans to continue raising rates at least through September before potentially pausing to assess how well inflation is being controlled. The market is currently anticipating an additional interest-rate increase of 75 basis points in September, followed by smaller hikes in November and December. And there could be more tough times ahead for bonds if the Fed has to make additional rate hikes to tamp down inflation.

Unfortunately, it's impossible to predict exactly what steps the Fed will take and how the bond market might react. As the investor-return gap shown above illustrates, trading activity often leads to weaker returns for bond-fund investors. Institutional investors don't necessarily fare any better, as market interest rates often shift quickly and in directions the market didn't previously anticipate.

Reasons to Stay With Bonds

While shifts in interest rates are unpredictable, the case for including bonds in a portfolio remains intact. As I discussed in a previous article, bonds still play a critical role in reducing risk at the portfolio level, even during periods of rising interest rates. Bonds can also be surprisingly resilient because yield plays such a significant role in determining future returns. Rising interest rates are a negative for bond prices in the short term but can be beneficial as older bonds mature and investors can then purchase newly issued bonds with higher yields.

Bonds can also provide diversification benefits thanks to their generally low correlations with stocks. Even during periods of rising interest rates, bonds usually have a lower correlation with stocks than most other major asset classes, which enhances their ability to reduce risk at the portfolio level. Our analysis of previous stress periods for inflation and interest rates indicates that stock/bond correlations have rarely increased above 0.6, and then only during the most acute periods of rising rates and/or inflation. As a result, bonds can still play an important role in reducing portfolio risk even during periods of weaker fixed-income performance.

Fixed-income holdings also play an increasingly important role as millions of investors transition into retirement. Based on data from the U.S. census bureau, 20.3 million Americans (or 6.2% of the population) are between age 60 and 64 and will reach retirement age within the next several years. An additional 52.4 million individuals (or 16.8% of the U.S. population) were already 65 or older as of mid-2021. For investors in this age range, allocating a portion of assets to fixed-income securities is one of the best ways to control sequence of returns risk—the risk that a series of bad market returns early in retirement will dent the portfolio's value, potentially leading to a permanent reduction in assets available for withdrawals.

From all appearances, fund investors had previously taken the merits of fixed-income investments to heart, as more than $1.8 trillion in net inflows flooded into taxable-bond funds over the five-year period from 2017 through 2021. This year’s outflows, on the other hand, are cause for concern.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/d10o6nnig0wrdw.cloudfront.net/06-11-2024/t_a4a9c8e4b4944a9fab91f0fccfde5dcc_name_MIC_24_Jerome_Schneider_Speaker_1920x1080.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/AGAGH4NDF5FCRKXQANXPYS6TBQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)