Is an Annuity Right for You?

To understand whether these complicated products might suit you, start with the goals you have for your money.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

If there is one investment that sparks both deep confusion and heated debate, it’s annuities.

It starts with the fact that these are insurance products, even when they are combined with mutual funds. They range from low-cost, simple annuities that can deliver on a promise for a guaranteed stream of income and strengthen a retirement plan, to expensive, highly complicated packages offering uncertain results that critics often rightly deride as not much more than a way for an advisor (or insurance salesperson) to earn a commission.

A combination of potential benefits from some features, significant pitfalls from others, wide variations in complexity, opacity of fees, and high commissions and advisor incentives makes it incredibly difficult for consumers to figure out if an annuity is simply right for them in the first place, let alone conduct due diligence on various products. The result is that some investors who could benefit from an annuity miss out, while others end up locking themselves into products that can do real damage to their financial plan.

We've built a special report designed to help educate investors on annuities. We’re going to start with the basic question of “Should I invest in an annuity?” Elsewhere in the guide, we will discuss how to evaluate the different types of annuities--from the most simple fixed annuities to complex equity index annuities--assess strategies for fitting annuities into a portfolio, understand and compare costs, and evaluate issuers, among other topics.

The first step, of course, is understanding whether an annuity makes sense for you.

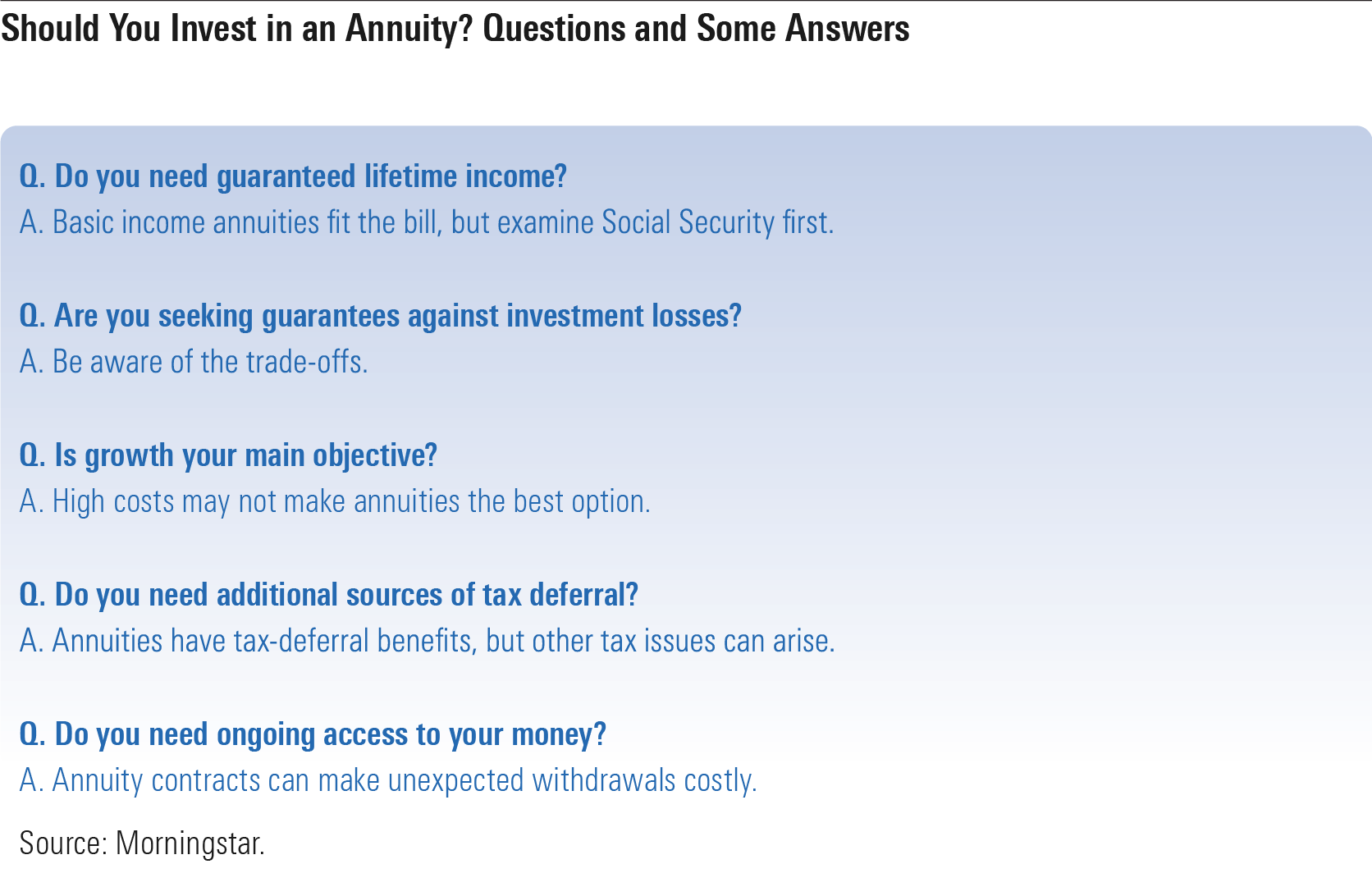

Do you need guaranteed lifetime income? I'd argue that the ability to earn guaranteed lifetime income is the biggest attraction to an annuity. In contrast with your portfolio, which can run out if you overspend or make poor investment decisions, most annuities, once you annuitize, will pay you income for the rest of your life, much like Social Security. It won't necessarily be a high level of income, but "risk pooling" means that you "pool" your risk with other buyers. Some people in the annuity pool will live longer, some will live shorter, with the shorter-lived people effectively plumping the lifetime payments for those who live longer.

That feature means the payout on basic income annuities will tend to be better than you’ll find on pure investment products. For example, a 70-year-old who put $100,000 into a single-premium immediate annuity with no survivor benefits would receive just over $600/month for the rest of his life, or a roughly 7% annual “return.” (I used USAA’s calculator to play around with some options.) That’s not directly analogous to a return you might earn on an investment, in that part of the “return” is your own capital being sent back to you as a stream of income. By contrast, if you put your money into an investment and earn a yield, you’ll usually receive at least some of your money back when you sell. (With safe investments like high-quality bonds or bond funds, you’ll typically receive all of your principal, though yields are, of course, meager today.)

Nonetheless, the combination of lifetime income plus a higher payout means that basic income annuities can be a sensible addition to retirees' tool kits. That's particularly true today, given low yields on safe investments, the ebbing away of pensions, and longer life expectancies, especially for wealthier individuals. (If you're part of a married couple, there's a 1 in 4 chance that you or your partner will live to age 95, and if you're higher-income, the odds are even higher that one of you will make it to 95.) Other annuities, such as equity indexed annuities and variable annuities with guaranteed lifetime withdrawal benefit riders, discussed below, also can deliver income, albeit with additional costs and complexity.

But even as providing a baseline of guaranteed income may be the most compelling reason to consider an annuity, even retirement experts who are bullish on annuities believe that would-be annuity purchasers should explore delayed Social Security filing first. After all, Social Security provides a lifetime income stream, just like an annuity does, and the longer you delay the larger your eventual benefit will be. Moreover, Social Security benefits are adjusted to keep pace with inflation; annuity payments won’t be, unless you purchase an annuity that includes an inflation rider.

Are you seeking guarantees against losses? Protection against outliving your assets--the ability to receive an income stream until you die--is arguably the most compelling selling point for annuities. That's the key reason that so many retirement researchers believe that annuities, especially immediate income annuities or deferred income annuities, are underutilized in retiree portfolios.

Yet annuities are often sold because of other guarantees--namely, protection against big stock market losses. Indeed, a common type of annuity--an equity indexed annuity--has that as its main selling point. These products use options to provide returns that are based on the performance of an equity index but also put a floor underneath losses. From that standpoint, equity-indexed annuities might seem like the best of all worlds, but purchasers should be aware of the trade-offs. For one thing, the contracts curtail how much equity-market performance investors actually enjoy, owing to “caps” and “participation rates” that protect the insurer’s profits but cut into the client’s upside. That means that returns on equity indexed annuities tend to fall between stocks and high-quality bonds. The products can also be incredibly complicated.

Is growth your main objective? Another common selling point of annuities is growth. But how much growth you can expect depends completely on the annuity type. For income annuities--either immediate or deferred--guaranteed income is the main objective, so growth will be modest. To be able to pay out to annuitants what they've been promised, the insurer must invest the assets used to purchase the annuity very conservatively. That suggests that investors buying an income annuity who also want growth would do well to augment it with exposure to the equity market; they're not going to get it from this type of annuity.

Other annuity types offer more growth potential. In the case of variable annuities, for example, the account owner controls the investments, called subaccounts. The funds can be invested in safe investments as well as higher-growth, higher-risk ones such as equity funds and even emerging markets. Equity indexed annuities also offer equity-market participation, as discussed above.

At the same time, other features of these annuities can dilute their growth potential. High costs--which can total nearly 2.5% or even more--can erode the growth of variable annuities. With equity indexed annuities, the guarantees against losses also typically mean that the buyer must accept a cap on gains. Thus, investors seeking growth who don’t also have a need for the additional benefits the annuity confers may be better off investing outside of the confines of the annuity, either in an IRA or brokerage account.

Do you need additional sources of tax deferral? Another of the main selling points for annuities is the potential tax benefit. Annuities are tax-deferred, similar to funds in a traditional IRA or 401(k). That means that as long as your assets stay inside the annuity wrapper, they're not subject to taxation. Because contributions to annuities aren't subject to the same income or contribution limits as IRAs and 401(k)s, the products are often sold as an additional source of tax-deferred funds for retirement.

That's true, but it's also important to understand the tax treatment of the funds on the way out. If the annuity consists of assets that have never been taxed--for example, you purchased the annuity with rollover IRA assets (your assets consist of pretax dollars plus investment gains have never been taxed)--it's considered qualified, and any payments you receive from it are fully taxable at your ordinary income tax rate. If, on the other hand, you steered aftertax funds into the annuity, the tax due upon any payments from it are subject to what's called the exclusion ratio, meaning that any funds you've already paid taxes on aren't subject to taxes, but amounts over and above that level are subject to ordinary income tax. If you outlive your life expectancy, any payments past that point are taxable.

That opportunity for tax deferral means that annuities have some tax benefits relative to saving in a plain-vanilla brokerage account, but they’re not necessarily better. While a brokerage account doesn't supply tax deferral in the same way as an annuity does, the appreciation on assets in a taxable account is taxed at your capital gains rate. That's lower than the ordinary income tax rate that applies to annuity payments (apart from amounts that have already been taxed). And if you buy an annuity with qualified funds, you're effectively doubling up on the tax advantages.

Do you need ongoing access to your money? Finally, your need for liquidity should be a key consideration before venturing too far down the path of an annuities purchase. Annuities are contracts with insurance companies, and while different annuities have different rules about withdrawals, they typically carry charges if you need access to your funds within the first several years of purchase. (Some annuities do give you the option to withdraw a portion of your funds each year.) Taxes also come into play. Similar to the tax treatment of funds in an IRA, you'll owe ordinary income tax on any investment gains (above and beyond the amount you put into the contract), plus an additional 10% penalty if you're not yet 59-1/2. If you put qualified funds into the IRA--for example, you rolled over an IRA consisting exclusively of money that has never been taxed--the withdrawal will be fully taxable.

Thus, if your financial situation is uncertain or if there’s a possibility you’ll need to take a chunk out of your annuity with the first seven to eight years of purchase, an annuity probably isn’t the right vehicle for you in the first place. (Guaranteed lifetime withdrawal benefit riders, discussed above, allow for more flexibility on the withdrawal front, albeit with extra costs.) And liquidity helps explain why people who do decide that an annuity is best for them should hold also nonannuity investments alongside that annuity to further diversify and to meet liquidity needs as they arise.

Could Your Portfolio Use a Makeover?

for a chance to have Christine Benz review your portfolio and provide improvement suggestions based on your needs.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YBH7V3XCWJ3PA4VSXNZPYW2BTY.png)

/d10o6nnig0wrdw.cloudfront.net/04-24-2024/t_a8760b3ac02f4548998bbc4870d54393_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/O26WRUD25T72CBHU6ONJ676P24.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)