What Investor Biases Are the Conscientious Most Prone To?

Contributor Michael Pompian shares the results of his new study of personality traits and investment biases.

This is the seventh article in a series focusing on the Big Five personality traits and how they relate to the behavioral biases of investors. Over the years, I have followed a debate between the effectiveness of the Myers-Briggs test versus another widely used personality test, the Big Five. More recently, the debate has intensified. I decided to conduct a study of the Big Five. Specifically, I studied 121 investors, examining the relationship between the Big Five and investor biases. Why? Because taking the time to understand the underlying personality of the investor leads to better advice and results.

This month’s article examines the second of the Big Five traits: conscientiousness.

Conscientiousness People high in this trait tend to be thoughtful, goal-oriented, good at controlling their impulses, and disciplined. They're also well-organized and pay attention to detail. The conscientious are planners and think about how their behavior affects others. Lastly, they are mindful of deadlines.

The Study I tested 121 investors for the Big Five personality traits and for the following investor biases: loss aversion, status quo, recency, hindsight, confirmation, availability, and overconfidence.

The results of the study show what percentage of the population surveyed is (a) subject to each of the Big Five traits and (b) subject to each of the biases. For those personality traits that have a large percentage of respondents subject to a given bias, we will discuss strategies to work with clients on these behaviors.

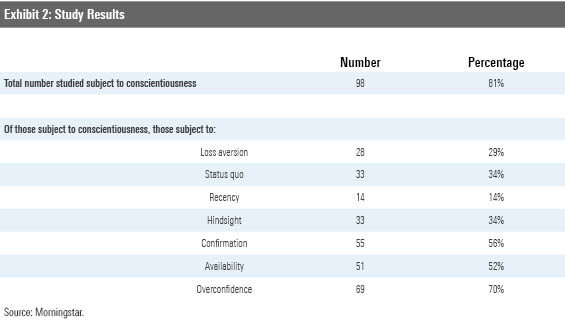

These are the results for conscientiousness.

Analysis of Results Per the table above, 81% of the 121 people surveyed were subject to conscientiousness. Of these 98 people, you can see the percentages that were subject to the various biases. About 70% were subject to overconfidence. The next two most-common biases among the conscientious were confirmation and availability.

Let’s unpack each of those biases below.

Overconfidence In its most basic form, overconfidence bias is unwarranted faith in one's intuitive reasoning, judgments, and cognitive abilities.

The following example of a driver under the influence of alcohol illustrates this. In spite of an enormous body of evidence that drinking impairs a person’s ability to drive safely and react quickly, drunks continue to get behind the wheel. If you suggest they shouldn’t, the typical responses are “I’m OK,” “I can handle it,” or “I am one of those people who aren’t affected by alcohol like other people.” They are overconfident in their abilities to drive under the influence and assume they can beat the safety odds better than everyone else. Similarly, investors exhibiting overconfidence bias overestimate their abilities, sometimes with disastrous consequences. They buy stocks with little or no research, or try to guess the direction of the market without realizing that the market direction from day to day is not able to be predicted.

Advice: I have seen overconfidence in action many times over my practice. To counteract this behavior in my clients, I often recommend they establish a "mad money" account. This involves taking a small portion of one's wealth for "overconfident" trading activities while leaving the remainder of their wealth to be managed in a disciplined way. This approach scratches the itch that many investors have to trade their account, while at the same time keeping the majority of the money intelligently managed.

Confirmation Bias Confirmation bias is a belief perseverance bias and refers to a type of selective perception that emphasizes ideas that confirm our beliefs, while deemphasizing or devaluing information that contradicts our beliefs.

In short, as humans, we believe what we want to believe, and we seek out information that supports our beliefs versus seeking information to the contrary.

Put more simply, confirmation bias refers to our all-too-natural ability to convince ourselves of whatever it is that we want to believe. Because it makes us feel good, we attach undue emphasis to events that corroborate the outcomes we desire, and we downplay evidence to the contrary that arises. In the investment realm, confirmation bias runs rampant. Clients to advisors to even money managers often seek information that supports or confirms their investment decisions while discounting information that contradicts those choices. The investment implications are that less-than-optimal decisions can be made without realizing it, and these decisions can add up over time to reduced overall portfolio performance and possibly not attaining financial goals.

Advice: My advice for overcoming confirmation bias, as with many biases, is to learn to recognize it in action. I can't tell you how many times my team members at work and I say to each other, "Isn't that confirmation bias in action?" My second piece of advice for overcoming confirmation bias is to intentionally put more weight on contradictory information than you typically tend to do. Play devil's advocate with yourself and make a case for how the contradictory information could be right. You might be surprised when you actually change your mind based on the contradictory information. If, however, after this process you can objectively believe that your original view is still valid, then you should proceed with your course of action.

Availability The availability bias, another information-processing bias, is a rule of thumb, or mental shortcut, that causes people to estimate the probability of an outcome based on how prevalent or familiar that outcome appears in their lives. People exhibiting this bias perceive easily recalled possibilities as being more likely than prospects that are harder to imagine or difficult to comprehend.

Investors will often choose investments based on information that is available to them (for example, advertising, suggestions from advisors, friends, and so on) and will not engage in disciplined research or due diligence to verify that the investment selected is indeed suitable for their situation. The result of availability bias is that investors may not choose the best investments for their portfolio and end up with suboptimal returns. A simple example of availability bias is choosing investment funds based on those that do the most advertising. Since the information is available, many investors simply go with the one they’ve heard of most. In reality, there are many high-quality funds that do no advertising but could be found via research services. Because this may present a burdensome endeavor, some investors simply choose the most readily available information for their decision-making.

Advice: Investors will choose investments that resonate with their own personality or that have characteristics they can relate to their own behavior. Taking the opposite view, investors ignore potentially good investments because they can't relate to, or do not come in contact with, characteristics of those investments. For example, thrifty people may not relate well to expensive stocks (high price/earnings multiples) and potentially miss out on the benefits of owning these stocks. Generally speaking, in order to overcome availability bias, investors need to carefully research and contemplate investment decisions before executing them. Focusing on long-term results is the best approach rather than following current investing trends without a plan to overcome availability bias. As an advisor, you should be aware that everyone possesses a human tendency to mentally overemphasize recent, newsworthy events. Refuse to let this tendency compromise you or your advice to your client. The old axiom that "nothing is as good or as bad as it seems" offers a safe, reasonable recourse against the impulses associated with availability bias.

Michael M. Pompian, CFA, CAIA, CFP is an investment advisor to family office clients and is based in St. Louis. His book, Behavioral Finance and Wealth Management, is helping thousands of financial advisors and investors build better portfolios of investments. Contact him at michael@sunpointeinvestments.com.

The author is a freelance contributor to Morningstar.com. The views expressed in this article may or may not reflect the views of Morningstar.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6NPXWNF2RNA7ZGPY5VF7JT4YC4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RYIQ2SKRKNCENPDOV5MK5TH5NY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)