Multitaskers Get Serious About Retirement Funding

With three kids and a single income, it’s time to create a portfolio that can address this young family’s multiple goals.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

Editor’s Note: This portfolio makeover is from 2019. Keep in mind that the current market environment may be different than when this makeover was executed.

Busy with their three kids and living primarily on a single income, Drew, 35, and Emily, 34, feel like they’re playing catch-up on retirement savings. College funding for their three children--ages 5, 6, and 14--is also top of mind. But above all, Drew and Emily would love to buy a house. They’ve been renting but would love to lock in a mortgage while interest rates are still low.

The couple has about $125,000 in total savings--mainly in retirement accounts--and hasn’t yet tackled college. Drew says that Emily’s decision to pursue freelance work rather than working full-time outside the home after their children were born has been absolutely the right one for their family.

“Being self-employed has afforded my wife a lot of flexibility with when and how much she works, and allowed her to be really involved with our kids, minimizing our need for paid childcare,” he wrote.

At the same time, the reduction in household income has had an impact on the family’s finances.

“Our household income took a hit and retirement savings slowed,” Drew acknowledged. “We are not where I would like to be in terms of current savings. However, I think there is hope to get on track.”

Drew earns $128,000 in his current job and this year will be eligible for a bonus equivalent to one third of his salary. He also has been aiming to set aside 12% of his income, and his employer makes a 3% matching contribution 401(k) contribution as well.

At this juncture, Drew and Emily would like a second set of eyes on the totality of their plan, as well as their investment choices.

“I would like to make any recommended changes to current holdings, future allocations, and so on, while time is on our side,” Drew wrote.

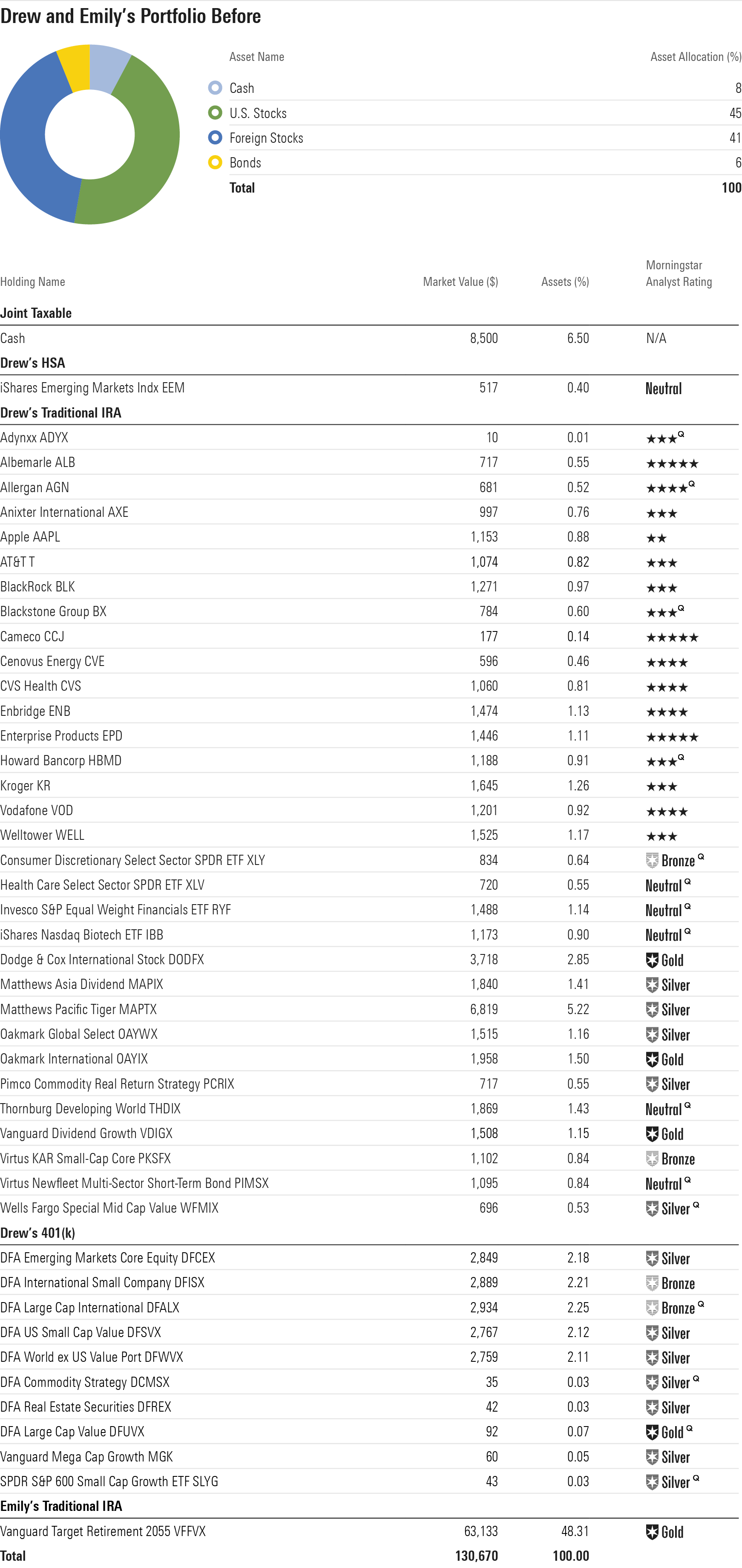

The Before Portfolio Drew and Emily's long-term assets are in three main silos: Emily's Traditional IRA (rolled over from her previous workplace plan), Drew's Traditional IRA (also a rollover), and Drew's current 401(k). They also have a small amount of assets tucked into a health savings account. In addition, they have a cash account that holds $8,500 and is invested in a high-yield savings account earning 1.8% today. Their total portfolio is almost entirely stocks, split almost evenly between U.S. and foreign names; their portfolio also includes small stakes in cash and bonds.

Emily’s IRA is straightforward and is parked in a low-cost target-date fund geared toward retirement in 2055; like most long-dated target-funds, it’s dominated by a globally diversified equity portfolio.

Drew’s IRA and 401(k) accounts are idiosyncratic, though, and even more aggressive.

“I have a high tolerance for risk and prefer a very aggressive investment style,” he wrote. “I’ve gone through periods where I think having three or four low cost Vanguard funds sit on the shelf for 25 years would be the way to go, but that’s not really my style.”

Exhibit A is his IRA, which is almost entirely equities, save for a position in a short-term bond fund. It includes an array of small positions in some topnotch mutual funds, many of them international, including Oakmark International OAYIX, Matthews Pacific Tiger MAPTX, and Dodge & Cox International Stock DODFX. It also includes sector- and market-segment-specific exchange-traded funds and a broad basket of small holdings in individual stocks--17 in all. Many of those individual stock positions are quite tiny; the average star rating for the stock portfolio is 3.6 stars.

Drew’s 401(k), meanwhile, is also equity-heavy, consisting of reasonably priced funds from DFA as well as Vanguard. It’s even more heavily international than his IRA, with more than three fourths of that sleeve of the portfolio in foreign stocks. In aggregate, the equity portfolio heavily emphasizes smaller-cap and value names.

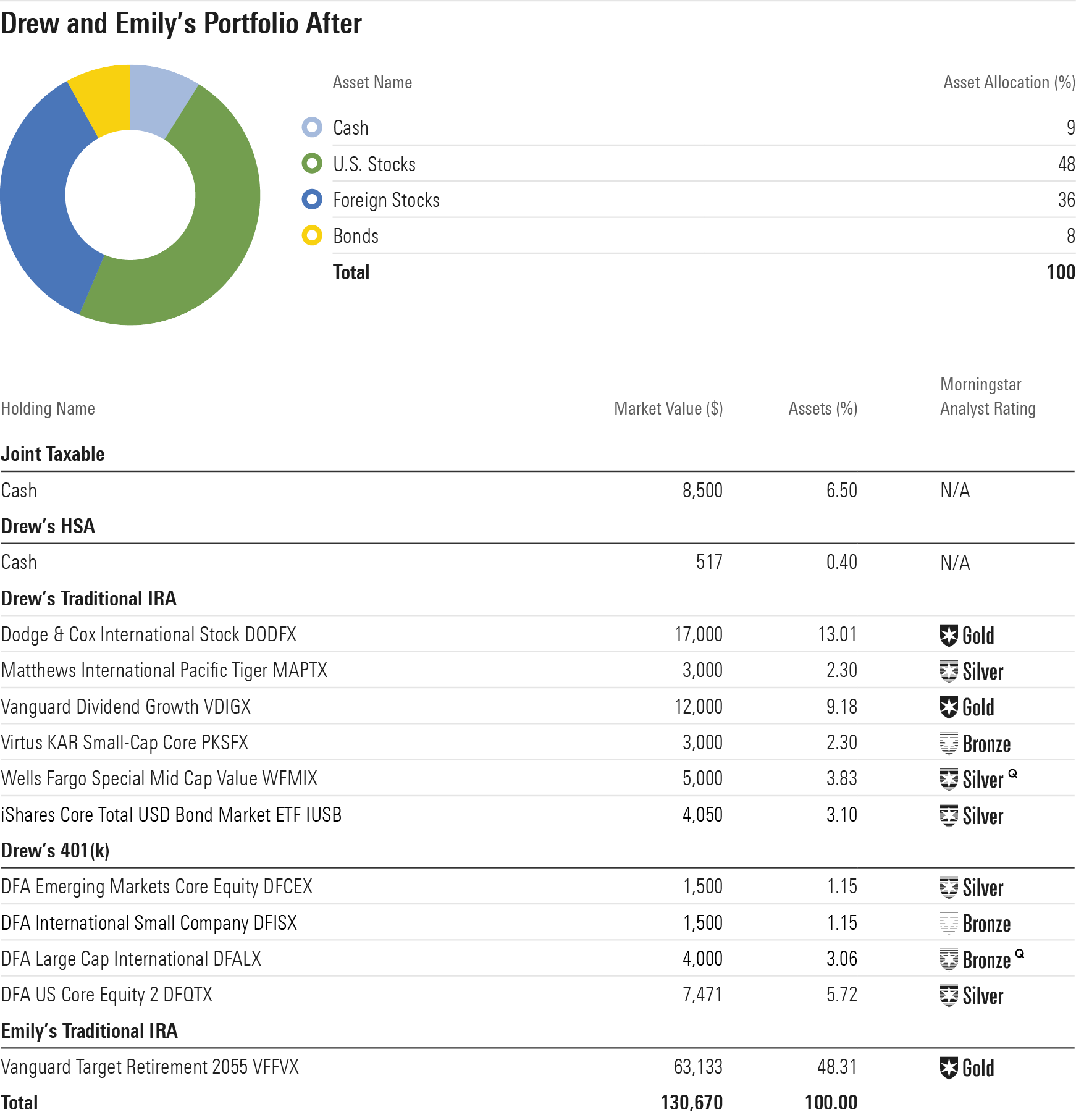

The After Portfolio Drew is correct that it would be ideal if the couple could take advantage of their long runway to retirement to stoke their retirement accounts. But their first order of business should be to bulk up their holdings in boring old cash. In addition to their goal to build up a down payment for their home, they need a larger emergency fund. Given that Drew is the family's primary earner, I would recommend aiming toward the higher end of the usually recommended cash range of three to six months' worth of living expenses.

They can continue to build cash in their high-yield savings account or, alternatively, could begin to steer some assets into a Roth IRA. The beauty of the Roth is that they can harness the tax benefits of the account, but withdrawals of contributions are tax- and penalty-free at any time and for any reason. That would enable them to build security while at the same time saving for their future and/or a home. Drew’s bonus, which he expects early next year, can be steered into a Roth IRA; he can make contributions in his own name as well as Emily’s, and if their budget allows, they can make contributions for both the 2019 and 2020 tax years.

I targeted a high equity allocation for the total portfolio; the "After" portfolio includes 84% of assets in stock funds, and their retirement holdings skew almost entirely toward stock funds. I left Emily’s IRA alone, because it’s sensibly positioned. My major adjustments were to Drew’s IRA and 401(k). In recognition of the fact that Drew is comfortable with equity-related volatility, I left the heavy equity weightings largely intact in both accounts. And while my personal bias is toward more “vanilla” portfolios, I maintained Drew’s emphasis on value, smaller-cap, and foreign-stock names. All three market segments have struggled relative to U.S. large-growth names in recent years, so it isn’t unreasonable to assume some reversion to the mean over the next decade.

At the same time, I cut the individual stock names in Drew’s IRA and reduced other idiosyncratic bets. My thesis is that Drew and Emily need the potential return boost than comes with holding an equity-heavy portfolio, but they don’t need to compound the risks inherent in that position by heavily emphasizing individual stocks and sectors.

Within the IRA, most of the individual equity positions sizes are too small to have a meaningful impact on that portfolio’s bottom line. That’s a positive in that one errant stock pick won’t crater his whole account, but it leads to more complication than is necessary. I also cut the positions in sector-specific ETFs. I retained a number of Drew’s active funds, however. Vanguard Dividend Growth VDIGX is a superb core equity holding, and Drew has chosen fine complementary holdings in Virtus KAR Small-Cap Core PKSFX and Wells Fargo Special Mid Cap Value WFMIX. I streamlined the international holdings, too, opting for Dodge & Cox International and Matthews Pacific Tiger. I also added one of my favorite core bond ETFs, iShares Core Total USD Bond Market IUSB, which provides well-diversified exposure to the total U.S. bond market, including a dash of lower-quality credits.

Within Drew’s 401(k), I retained many of his original picks but undertook some repositioning, again with an eye toward reducing idiosyncratic bets and making the portfolio less complicated overall. Drew’s 401(k) fields a terrific lineup, including DFA US Core Equity 2 DFQTX. That fund is suitable as one-stop U.S. equity exposure, but tilts toward factors that have been associated with long-range outperformance--specifically, companies that are smaller, cheaper, and more profitable than their peers. There’s no one-stop international option on the 401(k) menu, so I cobbled together three DFA holdings that give Drew well-rounded exposure to foreign stocks, including large caps, small caps, and emerging markets.

I would give retirement funding priority over college funding for the time being, especially given that college for their oldest son is just a few years away and that they're a bit behind on retirement savings relative to where they should be at this life stage. (Fidelity and T. Rowe Price have both provided useful benchmarks for thinking about the adequacy of retirement funds at various life stages.) However, I do think it makes sense to set up 529 plans for each of their children, including their 15-year-old, using the age-based options offered by their home state's 529. They can contribute small monthly sums to each account on autopilot, earning a state tax deduction on those contributions, and steer any cash gifts that the children receive into the accounts. As their incomes ramp up, they can increase those contributions, while still steering the lion's share of their savings to their retirement accounts.

Finally, if Drew and Emily will be covered by a high-deductible healthcare plan in the future, I’d invest their current health savings account assets, along with any future contributions, to cash. The HSA vehicle does have unparalleled tax benefits for long-term investors, but Drew and Emily’s current financial plan doesn’t allow them the wiggle room to fund out-of-pocket healthcare expenses with non-HSA assets. If they needed to raid their HSA to pay a big medical bill, they’d risk selling themselves out of the emerging-markets fund at a poor time, locking in those losses. For now, they should use the HSA as a spending vehicle rather than for long-term investments, and keep the money parked in a savings account.

Amy Arnott, Jess Liu, Chris Margelis, and Michael Schramm contributed to this report.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)