Few Good Alternatives

Liquid alternatives can diversify risk, but most do little to improve traditional portfolios.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

A version of this report appeared in the May issue of Morningstar ETFInvestor.

Is it necessary to diversify beyond traditional stocks and bonds? The idea of owning an investment with positive expected returns uncorrelated with the rest of the portfolio is clearly appealing. But many alternative strategies fail to deliver the diversification and performance benefits they promise. Alternative investments aren’t necessary for long-term success or to have a well-diversified portfolio. So, it’s okay to skip them. That said, there are some strategies that might be worth considering—but proceed with caution.

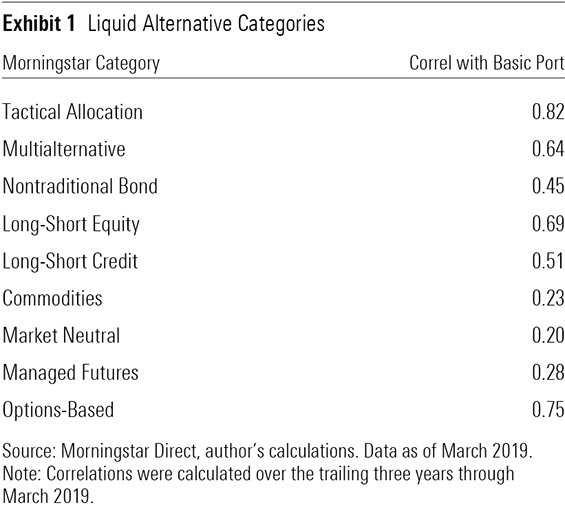

Many Options, Few Asset Classes Alternative investments are diverse. There are many types of strategies out there, as shown in Exhibit 1. Even those within the same Morningstar Category often do very different things. Yet, there are only four distinct asset classes: equity (including real estate), debt, currency, and commodities. Most alternative strategies repackage exposure to one or more of these asset classes, often by taking long and short positions to deliver performance that isn't highly correlated with long-only stock and bond portfolios.

The biggest potential benefit of taking both long and short positions is diversification, but there are others. This approach should also better isolate active bets and limit exposure to unintended sources of risk, such as a sector, market, or style falling out of favor and wiping out the return from a good stock call. And there may be more opportunities to profit from mispricing on the short side. There is a long-only bias in the money management industry, as well as a bias toward buy ratings on stocks. Both factors could make it easier for stocks to become overvalued than undervalued.

Pairing long and short positions should reduce both expected returns and exposure to market risk. But this approach can also increase exposure to firm-specific risk and potential losses from poor active bets. Not all alternative investment strategies take short positions, and many that do still have positive net exposure to the market.

Most alternative investment strategies are riskier than investment-grade bonds but offer lower expected returns than stocks. However, they could still be worth holding if their diversification benefits are strong enough.

Most Alternatives Haven't Delivered A Morningstar study by Jason Kephart and Maciej Kowara found that most liquid alternative investment strategies (available in a mutual fund or exchange-traded fund wrapper) wouldn't have improved performance relative to a traditional 60/40 stock/bond portfolio over the trailing five years through December 2017.[1]

As their study explains, an investment is worth adding to a portfolio if its expected Sharpe ratio (return relative to volatility) is greater than the current portfolio's expected Sharpe ratio times the expected correlation between the two. The lower the correlation between the portfolio and the investment, the lower its required Sharpe ratio.

The study used this simple relationship to determine that most liquid alternatives’ diversification benefits and individual performance wouldn’t have been sufficient to improve the performance of a traditional stock/bond portfolio. That said, the period in scope was generally favorable to stocks. The authors found that liquid alternatives would have done a bit better from October 2007 through March 2012, though most still wouldn’t have improved a traditional stock/bond portfolio over that time.[2]

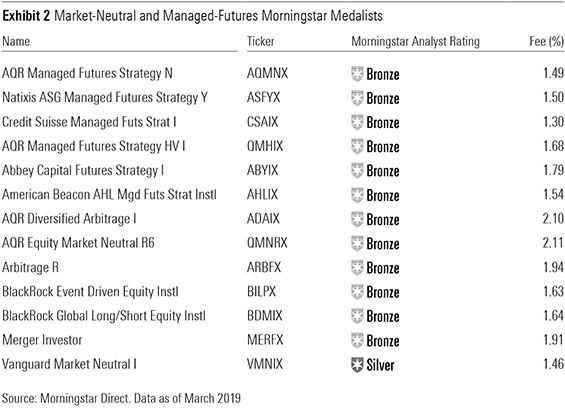

Market-neutral and managed-futures funds did a little better than most because of their low correlations with stocks and bonds, which can make them a good place to start looking for alternative investments.

Market Neutral Market-neutral strategies have similarly sized long and short positions, giving them little net exposure to the market. This allows them to largely strip out the impact of market movements and better isolate intended bets.

These strategies are ideal for factor investing and arbitrage trades. They can achieve stronger factor exposure than long-only portfolios by not only betting on stocks with attractive characteristics, but also betting against those that look unattractive on a given factor. This should also improve diversification, particularly for multifactor strategies, because the payoff to each factor is not highly correlated with the market. And most factors have low—sometimes negative—correlations with each other.

Vanguard Market Neutral VMNFX is an example of a promising market-neutral factor strategy. It targets stocks with attractive value, growth, quality, momentum, and management decisions relative to their industry peers and shorts those with the opposite characteristics, effectively stripping out both market and industry risk. In true Vanguard fashion, this is one of the cheapest funds of its kind.

Arbitrage trades attempt to take advantage of mispricing that is expected to correct soon. These work best when there are two securities whose prices should converge in the future. They typically require a long position in the undervalued asset and a short position in the overvalued asset. Market-neutral strategies are built on this type of trade.

Merger arbitrage offers a good illustration. After an acquisition announcement is made, the price of the stock to be acquired typically rises—but not all the way to the acquisition target, reflecting the risk that the deal may not go through. An arbitrager may take advantage of this risk premium by purchasing stock in the acquisition target and shorting the acquisitor. This trade would pay off if the acquisition goes through.

This is the type of strategy IQ Merger Arbitrage ETF MNA employs. This portfolio invests in acquisition targets listed in both the United States and foreign developed markets. To hedge risk not directly tied to the acquisitions, this strategy shorts sector and regional ETFs of the acquisitor, sizing these positions to match the long position in the acquisition target times the percentage of the deal financed with stock. That means it's not completely market-neutral. That said, its market beta has historically been very low. This is a reasonably priced (0.78% expense ratio) strategy, but it often has a concentrated portfolio with considerable exposure to firm-specific risk.

It’s important to remember that there are virtually no risk-free arbitrage trades. Mispricing can increase, and there’s always a chance that there’s no mispricing at all, but rather a misjudgment of the risks.

Managed Futures Like market-neutral funds, managed-futures strategies take both long and short positions and often have low positive net exposure to the market. But instead of taking positions in individual stocks, they use futures contracts, which are tied to the value of an index. This approach can reduce transaction costs by reducing the number of trades, and it is more efficient for macro bets on commodities, currencies, regions, and sectors of the global stock market, and interest rates. Many of these strategies incorporate momentum or trend-following signals to select their investments.

Exhibit 2 shows the full list of Morningstar Medalists in the market-neutral and managed-futures categories.

Portfolio Impact Well-crafted liquid alternatives, such as those listed in Exhibit 2, can help modestly improve the risk-adjusted performance of a traditional stock/bond portfolio. These holdings should play only a supporting role in a portfolio because market risk embedded in traditional stock and bond holdings will likely pay off over the long term.

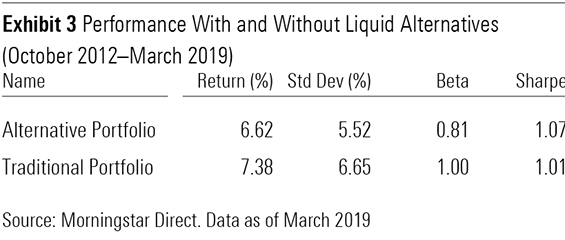

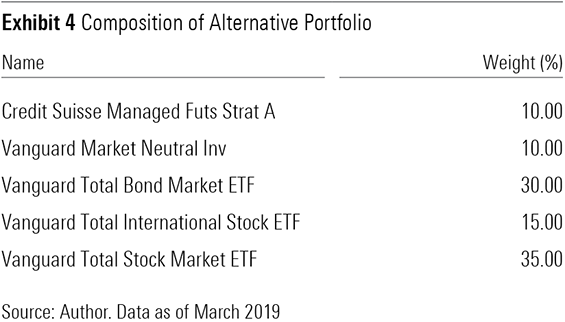

Exhibit 3 illustrates the potential impact of adding small positions in Vanguard Market Neutral and Credit Suisse Managed Futures CSAIX to a traditional stock/bond portfolio. Exhibit 4 shows the target allocations of this modified portfolio.

This adjusted portfolio would have exhibited slightly lower returns and volatility than the Basic Portfolio, from its inception in October 2012 through March 2019. This yielded slightly better risk-adjusted performance. However, the diversification benefits will likely be more significant during market downturns.

Alternatives to Alternatives Adopting a more defensive portfolio with traditional stock and bond investments can yield many of the same benefits as adding alternatives. For example, investment-grade bonds do a fairly good job of diversifying equity risk. Simply tilting toward such bonds and away from stocks can reduce volatility and improve performance during market downturns. Defensive stock portfolios, like iShares Edge MSCI Minimum Volatility USA ETF USMV, can also help achieve those objectives at a lower cost than most liquid alternatives.

[1] Kephart, J., & Kowara, M. 2018. “Liquid Alternatives Have Yet to Prove They Belong in Portfolios.”

[2] Kephart, J., & Kowara, M. 2018. “What If? The Liquid Alternatives Edition.” Morningstar.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)