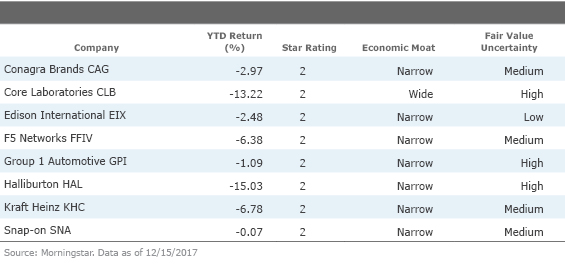

Stocks to Avoid

These stocks are all in the red this year yet continue to trade above our estimates of their fair value.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Two weeks ago in this column, we put the spotlight on stocks that have returned twice as much as the S&P 500 this year, yet still looked undervalued according to Morningstar's estimates of their fair values. These stocks have more room to run, in our opinion.

This week, we’re taking a look stocks through the opposite lens, focusing on those that have underperformed the market in 2017, yet still look overpriced according to Morningstar's estimates of their fair values. In our opinion, these would be stocks to avoid.

Specifically, we screened for stocks that have lost money this year and that are trading in 1- or 2-star range, which suggests they're overvalued. We then narrowed our search further to companies with wide or narrow economic moat ratings. Eight stocks that our analysts cover made the list.

Here's a deeper dive into three of those names.

Conagra Brands

CAG

Having split from its commercial foods business last year, Conagra today focuses on selling products in the meals, additives and snack aisles. Its portfolio includes brands such as Marie Callender's, Banquet, and Hunts. And although the narrow-moat firm has wrapped up several sensible strategic actions over the past two years, Morningstar sector director Erin Lash remains skeptical on the stock.

"Despite management's contention that this will allow for more focused execution, we aren't convinced this strategy will bolster its intangible assets--the source of our narrow moat," writes Lash in her latest Analyst Report.

For starters, says Lash, Conagra's portfolio is stuffed with second- and third-tier brands with little pricing power. And while the company is bringing new products to market and reducing promotions in an effort to improve brand equity, volume degradation during the past few years illustrates how challenging this will be. Lastly, CEO Sean Connolly's focus on brand mix, cutting costs, and fueling brand investments may have worked while he was an Hillshire Brands, but are, in Lash's mind, less likely to work here, given Conagra's weaker competitive positioning relative to its closest peers.

Although Morningstar assigns Conagra a narrow economic moat, that moat is eroding.

"Competitive pressures abound, and we don't believe its mix has mustered much clout, impairing its negotiating leverage with retailers," says Lash.

Core Laboratories

CLB

There's plenty to like about Core Laboratories as a company.

"We have long believed that Core Laboratories is one of the highest-quality oilfield service companies," writes Morningstar analyst Preston Caldwell in his latest report. "For one, with a wide-moat rating, Core Lab possesses the strongest moat across our entire oilfield service coverage. The company's foundational core analysis business in the reservoir description segment, in particular, has been virtually unchallenged over the past three decades."

Yet despite the company's moat being stable, Morningstar recently lowered its fair value estimate on the shares to $80, reflecting diminished long-term growth prospects for the company. Based on that estimate, shares are about 20% overvalued today.

But being overvalued is nothing new for these shares.

"This overvaluation likely stems from a misconception about how Core Lab's moat translates into a valuation premium," Caldwell says. "The market has long rightfully agreed with our view (reflected in our wide-moat rating) that Core Lab will earn high returns on capital for many years to come. Yet, such a view does not necessarily mean that Core Lab should be valued at a high multiple to fully recovered earnings, as is currently the case."

Only high returns on capital combined with sustained earnings growth can justify such a large premium multiple to earnings, he concludes.

F5 Networks

FFIV

"While

Despite its narrow moat rating, Morningstar believes the company's moat trend is negative. The firm's market share had steadily declined, notes Kundozerov, and its core ADC market has already peaked. Moreover, the growth of various cloud-based solutions threatens the company's margins in the long run.

"While the firm expects sequential revenue growth in fiscal 2018, starting from the first quarter, we think that we are going to see gradual gross margin erosion stemming from low-cost, cloud-native application delivery controller offerings," he says.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)