Private Equity: Capital Deployment Remains a Challenge

Despite record amounts of capital overhang and demonstrated interest for the asset class, valuations and heightened competition continue to constrain deal flow.

- Record EV-to-EBITDA multiples continue to challenge capital deployment.

- With a significant portion of PE-backed inventory acquired over the last 3.5 years, we expect exit flow to continue sliding as we are still a couple of years away before many of these assets are ready to be sold.

- With over $1 trillion distributed to LPs since the beginning of 2014, LPs have recycled a significant amount of capital back to the same fund managers who provided such distributions. Although we believe many managers will be able to sustain their relative outperformance over other asset classes, we do expect return profiles in newer vintages to decline given today's heightened valuations and competitive auction processes. Further, fund lives could continue to extend as managers look to maintain quality and price discipline—the result of which could put pressure on time-sensitive IRRs.

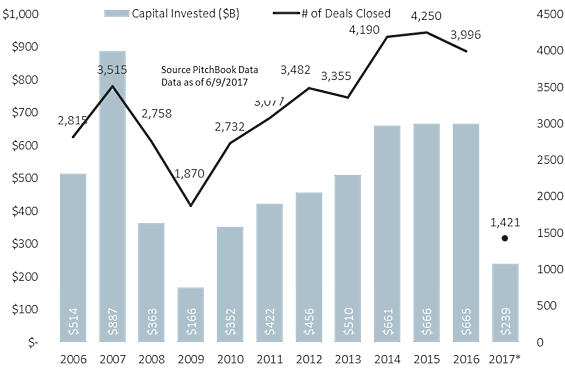

Approaching the end of 2017's first half, we’ve continued to see completed transaction counts inch lower on a quarterly basis, as has been the case since the beginning of 2016: Just $239 billion has been invested across over 1,400 transactions so far this year. At this pace, total U.S. deal value and volume would come in roughly 18% lower than what we experienced in 2016.

As we make our way through the upcoming quarters, we expect to see deal flow continue to move at a consistent, but tepid pace. Capital will continue to cycle back into the industry, as evident by the fundraising data we highlight below and the ability of PE to outperform many other asset classes on a relative basis.

Alongside the decline in deal flow, we also expect newer vintages to experience lower return profiles driven by a combination of persistently high valuations, stiff competition, and a shrinking pool of available targets, given the pace at which existing company inventory has grown.

U.S. Private Equity Activity

Source: PitchBook | Data as of 6/9/2017

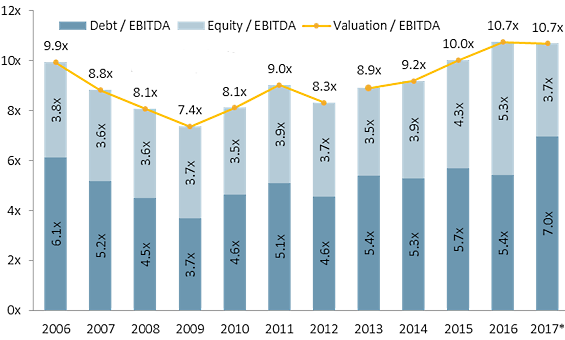

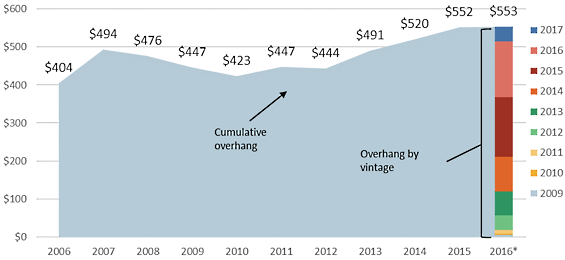

The median price-to-EBITDA multiple thus far into 2017 has stayed flat with what we experienced in 2016 at near 11x EBITDA, the highest figure we’ve seen since at least 2006. Further, despite concerns that have arisen around the sheer amount of capital overhang sitting in PE vehicles, our view is that we won’t see much fluctuation on this front, which doesn’t bode well for transaction multiples.

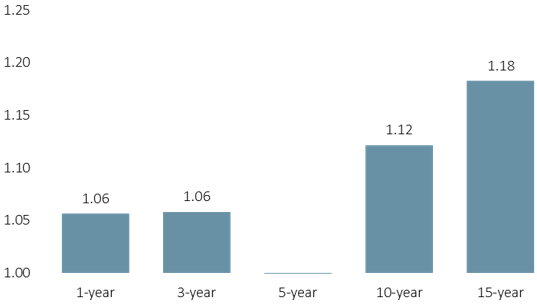

The primary driver of our conclusion stems from the continued interest and trust limited partners have placed in the industry. Over a 15-year horizon, PE has outperformed its public market counterpart by some 18%, and roughly 12% over a 10-year time frame. Even looking at returns over the previous three years, where public markets reached various record highs, the industry has outperformed by some 6%.

U.S. Private Equity EBITDA Multiples

Source: PitchBook | Data as of 6/9/2017

Global Horizon PE KS-PME vs. Russell 3000

Source: PitchBook | Data as of 6/9/2017

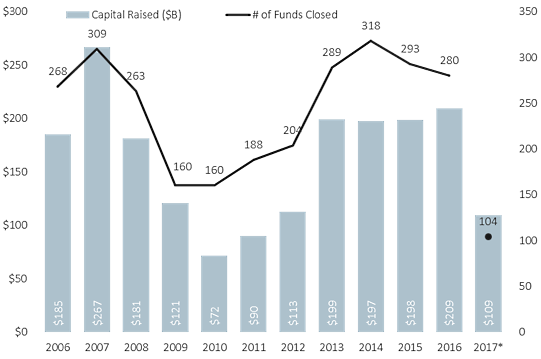

The success of the industry has fueled more than $1 trillion in LP distributions since the beginning of 2014, and as we near the end of 2017's second quarter, more than $109 billion has already been raised this year across 104 vehicles. Notably, first-half fund closings will likely come in near the lowest levels we’ve seen in recent years. Yet as LPs have continued to make larger commitments to a smaller group of managers, we expect that 2017 could very well still be on pace to see another near-record year of capital raised.

U.S. Private Equity Fundraising

Source: PitchBook | Data as of 6/9/2017

U.S. PE Capital Overhang

Source: PitchBook | Data as of 6/9/2017

More Quarter-End Reports

Market Stock Market Outlook: Equity Valuations Look Lofty

Economy Midyear Economic Forecast: Lower Inflation, Slow Growth

Credit Markets Credit Market Insights: Bond Indexes Perform Well in a Quiet Market

Equity Sectors Basic Materials Outlook: Propped Up and Too Expensive

Communication Services: AT&T and Verizon--A Duopoly No More

Consumer Cyclical: Amazon Reshapes Retail in Real Time

Consumer Defensive: Retailer Consolidation Sparks Concerns, but Opportunities Exist

Energy: Despite OPEC Cuts, a Crude Awakening Is Near at Hand

Financial Services: Our Take on U.S. Tax Reform and Bank Deregulation

Healthcare Outlook: ACA Repeal Efforts Unlikely to Yield Major Legislative Changes

Industrials: China Shows Signs of Softening, but the Sector Remains Healthy Overall

REITs: Some Scattered Opportunities in a Fairly Valued Sector

Tech: A Tectonic Shift Toward Enterprise Cloud Computing

Utilities: Tough to Stop This Sector's Powerful Performance

Mutual Funds First Half Winners and Losers for Funds

Second Quarter in U.S. Stock Funds: Growth on Fire

International-Stock Funds Continue to Prosper

Bonds in the Second Quarter: The Flattening

Portfolio Planning With Christine Benz Trends and Takeaways From 2017's First Half

PitchBook Reports Tapping the Brakes on M&A

Venture Capital: Less Is More?

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F2S5UYTO5JG4FOO3S7LPAAIGO4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZZNBDLNQHFDQ7GTK5NKTVHJYWA.jpg)