Most Investors Probably Won't Outperform This Simple Portfolio

A portfolio of low-cost index funds isn't a bad starting point for the average investor.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

A version of this article was published on morningstar.com in March 2014.

Investing can seem like a daunting task. But low-cost index funds make it easy for investors to do better than they would with most professionally managed offerings, after fees.

A broad-market index reflects the collective portfolio of all market participants and their view on the value of its holdings. In order for one investor to beat the market, someone else must underperform. Competition for superior performance creates a reasonably efficient market that is tough to consistently beat without taking on greater risk.

The average actively managed dollar must underperform the average passively managed dollar because it incurs higher fees and, in aggregate, active investors define the market portfolio.[1] But as Warren Buffett wrote in his 2013 annual letter to Berkshire Hathaway shareholders, "Nevertheless, both individuals and institutions will constantly be urged to be active by those who profit from giving advice or effecting transactions. The resulting frictional costs can be huge and, for investors in aggregate, devoid of benefit."

In the same letter, Buffett explained the advice he gave to the trustee for a bequest to his wife in his will: "Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 fund. (I suggest Vanguard's.) I believe the trust's long-term results from this policy will be superior to those attained by most investors--whether pension funds, institutions, or individuals--who employ high-fee managers."

While it may not be appropriate for most investors to tilt so heavily toward U.S. equities, the benefits of index investing persist in a more diversified portfolio, according to a

by Richard Ferri, founder of Portfolio Solutions, and Alex Benke, VP of financial advice and planning at Betterment. Ferri and Benke constructed a portfolio that invested 40% of its capital in the Investor shares of

Vanguard Total Stock Market Index Fund VTSMX, 20% in

Vanguard Total International Stock Index Fund VGTSX, and the remaining 40% in

Vanguard Total Bond Market Index Fund VBMFX. They tracked the pretax performance of this portfolio from 1997 through 2012 and compared it with 5,000 portfolios of actively managed funds. These active funds were randomly drawn from a survivorship-bias-free universe of each of the following categories: U.S. equity, international equity, and U.S. bond funds. The funds in these categories received the same weightings as in the index portfolio. Ferri and Benke excluded sales loads and did not rebalance either the index or the active portfolios. If a fund merged or closed during the period, they replaced it on that date with another randomly selected fund from the category.

In 82.9% of the simulations, the index portfolio outperformed the active portfolio. When the active portfolios outperformed, they offered a median excess return of 0.53%. But when they underperformed, their median shortfall was 1.25%. These results were also consistent after controlling for differences in risk. In other words, the odds of randomly picking a winning fund aren't good, and the cost of selecting a losing fund can more than offset the payoff from a winning fund. That can explain why Ferri and Benke found that the index-fund portfolio had a slightly higher probability of outperforming a portfolio of actively managed funds than the weighted-average probability of selecting winners in each individual fund category. This probability increased when the index-fund portfolio was compared with a portfolio that had multiple active funds within each asset class.

Not surprisingly, Ferri and Benke also found that the portfolio of index funds had a greater chance of outperforming a portfolio composed entirely of actively managed funds the longer it was held. This is because the cost advantage that index funds enjoy compounds over time, creating a bigger hurdle for active funds to overcome. Time also distinguishes luck from skill, which is scarce.

So picking active funds at random is a bad idea, but no one does that. Investors can improve their odds of success by simply selecting active funds with low expense ratios. To address this point, Ferri and Benke filtered out the most-expensive half of the universe of actively managed funds and reran their simulations. In this case, they found that the probability of the index portfolio outperforming fell to 71.5%. The median winning fund beat the index portfolio by 0.53%, while the median losing fund lagged by 0.92%. Those odds still aren't good. However, it may be possible to further improve the likelihood of success of an active approach by sticking to funds with large manager co-investments. Rigorous manager research can also help, but it requires more of the investor.

Even when an investor identifies a skilled manager, taxes can erode the return advantage when the fund is held in a taxable account. Broad market-cap-weighted index funds tend to be more tax-efficient than actively managed funds because they usually have much lower turnover. For instance, neither Vanguard Total Stock Market Index Fund nor Vanguard Total International Stock Index Fund has made a capital gain distribution in the past decade. In their study, Ferri and Benke did not account for this tax advantage.

While it is certainly possible to do better with active managers or style tilts, a portfolio of broad low-cost index funds is not a bad default option for investors who do not have strong conviction about a given active manager or investment strategy. It may be boring, but such a portfolio should do better than most. Investors who find themselves asking friends or tuning in to the media for investment ideas would probably be better off in an index portfolio, which harnesses the collective wisdom of the market.

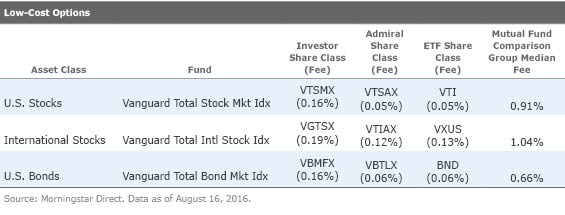

Portfolio Building Blocks There are plenty of good low-cost index mutual funds and exchange-traded funds investors can choose from to build a diversified portfolio. The three Vanguard index funds Ferri and Benke included in their study are among the best. These funds are available in both a traditional mutual fund and ETF format, as illustrated in the table below. The Investor and Admiral share classes require a $3,000 and $10,000 minimum investment, respectively. Vanguard charges a $20 annual account maintenance fee for account balances below $10,000 in these share classes. There is no minimum investment requirement or maintenance fee for the ETF share classes of these funds.

Though the appropriate asset allocation will vary with investors' risk preferences, applying the asset-class weightings from Ferri and Benke's study with the ETFs results in a weighted average expense ratio of 0.068%, or $6.80 for every $10,000 invested. In contrast, the weighted average median expense ratio from the corresponding mutual fund categories is 0.836%. In other words, the typical manager will have to outperform the market by 0.77% each year in order for investors to break even. Some will, but most probably won't.

[1] Sharpe, W. F. 1991. "The Arithmetic of Active Management." The Financial Analysts' Journal, Vol. 47, No. 1, P. 7. http://www.stanford.edu/~wfsharpe/art/active/active.htm

Disclosure: Morningstar, Inc.’s Investment Management division licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click

for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)