Dear Fellow White Women in Finance: Hold That Door Open

Diversity improves our work and work environment.

With a headline like the one on this column, I realize I risk limiting my audience, especially in the male-dominated world of finance and money management.

I’m willing to take that risk. And in any event, the advice portion of this article is relevant to men, too.

To my fellow white woman readers, I’m sure you know what it feels like to be the “only” in the room. The only woman on a team, the only woman in a management meeting, the only woman on a committee, or the only woman at a client dinner.

Of course, not only do you know how hard it is to be the “only,” but you also know how hard it was to get into that room.

Unfortunately, once inside the room, an instinct can arise to keep your head down, be grateful to finally be accepted, and work inside the established structure.

But the status quo isn’t working--not for us, not for people of color, and especially not for women of color. So now that you’re inside, use that leverage to hold the door open and welcome others in.

Who Benefits From Diversity Efforts Thanks to decades of national affirmative action programs and corporate diversity efforts, women have slowly increased in ranks in finance over the past few decades. While those gains are gratifying, we're not yet close to gender parity. And let's be honest: The benefits of corporate and industry diversity efforts have been reaped largely by white women, including me.

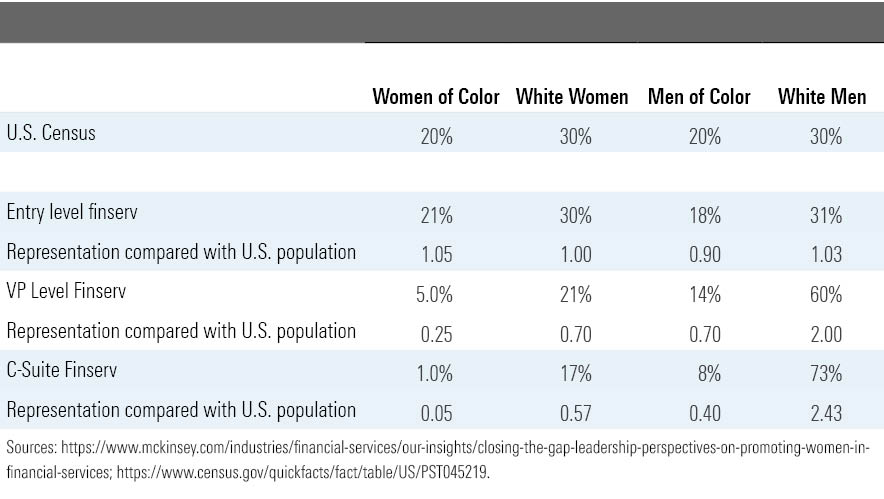

While white women, women of color, white men, and men of color now enter the financial-services workforce at rates approximately proportional to that of their representation in the broader U.S. population, white men make it to the C-suite at two and a half times that rate, while white women and men of color fall behind, and women of color are left with only crumbs. Doors don't just open for white men, they push them up the corporate ladder.

I suspect that if we had the data by race, and not aggregated into a group of “women of color,” that the data about Black women would be even starker, and Indigenous women would likely not be represented at the C-level.

The thing is, in addition to the moral imperative to give everyone an equal opportunity to succeed, working with people who are different from us improves our work and increases both creativity and diligence. For our industry to truly be of service to everyone--including those of us who work in it--we need full representation of Black, Indigenous, Latinx, Asian, Middle Eastern, and other people of color, LGBTQ folks, people with disabilities, and people from other underrepresented groups.

Doing the Work So, how can white women help to get more-proportional representation? Here are some effective tools for change.

- Hiring and retention--Reducing bias in your company's hiring process can lead to direct change. Some common biases in financial advisory firms include:

--Hiring preferences for Ivy League university graduates. Thanks to the lack of diversity among students at many of these schools, this bias removes talent from your candidate pool. It also favors those people who did well on standardized school exams or sports and likely had enough family resources (and potentially connections) to attend an Ivy League school.

--Hiring friends and family. This is a big one for smaller RIAs. While there’s nothing wrong with a family business, it drastically reduces your talent pool. Hiring from your immediate network may lead to finding the right job for the candidate instead of hiring the right candidate for the job.

--Requiring years of experience in the field when on-the-job training is sufficient. At entry level, this requirement can narrow down applicants to those who have the financial or family resources to take unpaid internships. At more-senior levels, where a network and excellent communication skills are crucial, financial advice can be a rewarding and successful second career.

To retain top talent, thoughtful hiring must be paired with fostering an inclusive workplace where all employees feel like they can be themselves and belong.

- Networking--Financial services is a "who you know" business. Look at the makeup of your company, the professional groups you are a part of, and even your LinkedIn connections. Is your network a self-reinforcing bubble? If so, intentionally diversify your network, and make introductions among your white colleagues and people of color, especially women of color. Introductions are powerful, not only in entering the industry but also in changing jobs, meeting new clients, being featured in the media, or securing new referral partners.

- Influence--It should go without saying that you must speak up when you see systemic inequity or individual inappropriate behavior. (I acknowledge that this is not always possible for women for safety and security reasons. Use your judgment.)

But broadly, another way to hold the door open is by influencing other people to speak out. White men still have the overwhelming majority of power in our industry. Some of those men have publicly and privately indicated their understanding of systemic inequity issues and their desire to be allies. Encourage those men to walk their allyship talk. I find that many men want to help but aren’t sure how, so if you have the capacity to give them specific suggestions, do so.

Here’s what that can look like: “John and Monica started at our company at the same time, but I’ve noticed that John is given more opportunities to present at our meetings and mingle with you and our other VPs. Monica’s work is deserving of that same level of reward and opportunity. Can you help me ensure she’s treated equitably here?”

In fact, I recently had the opportunity to use this “influence” technique. I received an invitation to a virtual conference, where all six keynote speakers were white men, including some who I know to be allies. I reached out to the men I knew on the panel and said: “I know all of you are allies, so I'm reaching out to see if you would consider asking [conference organizer] to do better here? ... I'm not indicating you shouldn't have a seat at this table. Instead, I know that we must make more seats at the table, for women, people of color, and women of color especially. I will talk to the folks I know at [conference organizer]. I know it will be more meaningful if the message comes from each of you as well, since messages from men carry more authority (sigh) and because you are involved in the event.”

- Diversity groups--If you are tapped to lead a women's initiative or a broader diversity initiative, be sure that the goals and outcomes of that work are reflective of racial diversity as well as other types of diversity. Financial services has a diversity problem; don't let the answer to that problem continue to be only white women. I recently had one Black woman in the financial-services industry recount to me how she was told not to talk about racism because it derails the conversation about women's equality. If we aren't talking about the additional obstacles women of color face, it's not a women's initiative, it's a white women's initiative.

- Dollars--Budgets indicate an organization's priorities. In the same way you may "shop small" to support local businesses, look at what people and groups benefit from the expense lines of your organization's budget. Unfortunately, the lack of diversity extends to tangential industries; most financial advisor service providers are run by white men. If you don't have the option to support businesses owned and run by people of color, you can still ask potential vendors about diversity in their organizations. Add a question about this to your vendor checklist, and remember that you have the most power before you write the check, so ask and pressure during negotiations. As more prospects and clients request representative companies, that increased demand can drive change.

- Conferences--Events and conferences, by nature of the stage-audience dynamic, give or reinforce credibility for the speakers. As a speaker, I only speak at events with a racially diverse speaker lineup, will not speak on all-white panels, nor will I be moderator for a group of all-male experts. In whatever role you play at conferences, you can influence whom we collectively listen to. As an attendee, you can choose not to attend conferences that only offer homogenous lineups and let the organizers know why. As a sponsor, you can make sure the speaker lineup is diverse before you write that check and ensure compensated speakers are paid at the same level as white men. And of course conference organizers and agenda committees can use their influence directly.

Hold the Door Open So, white women: More of us have made it into the room. While it's not our fault that financial services is overwhelmingly white and male, it is our collective responsibility to use our position in the room to hold the door open and invite in women of color, men of color, and other historically marginalized folks. Let's make space for everyone to have access to this powerful and rewarding profession.

Sonya Dreizler is a speaker, author, and consultant focused on fostering candid conversations about gender and race in financial services. She is also a subject matter expert in ESG and responsible investing and is a former CEO of an independent BD/RIA. When she's not working, you can find her hanging out with her kids, lifting weights, enjoying the beauty of Northern California, and chairing the board at CUESA. The views expressed in this article do not necessarily reflect the views of Morningstar.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/2TT3THVKOJAKBFGHCCRTVPNEQ4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6NPXWNF2RNA7ZGPY5VF7JT4YC4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RYIQ2SKRKNCENPDOV5MK5TH5NY.jpg)