Emerging Markets Look More Attractive

Russia, Brazil, and China stocks are comparatively cheaper than developed-nation stocks today, according to Morningstar’s quantitative valuation data.

Emerging Markets Look More Attractive

Russia, Brazil, and China stocks are comparatively cheaper than developed-nation stocks today, according to Morningstar’s quantitative valuation data.

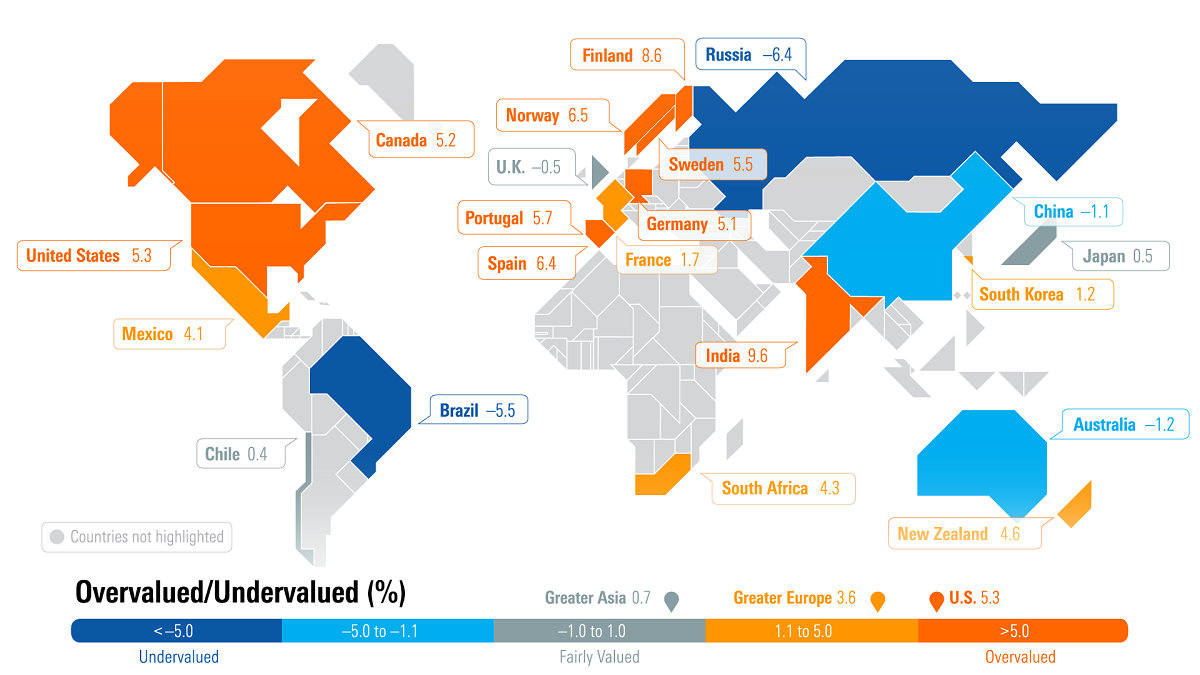

Tim Strauts: In today's chart, we are going to look at Morningstar's quantitative price/fair value [ratio] at the country level. Looking at North America, we see that generally Canada, the United States, and Mexico are all overvalued. But if you look to South America, we see Brazil--an emerging nation--is actually one of the most undervalued countries at negative 5.5%.

Now moving over to Europe, we see that developed countries in Europe are all overvalued--[with the exception of] the U.K. being a slight undervaluation. Then we see Russia, which is undervalued by 6.4%.

Moving over to Asia, we see a region that is generally attractive with China being at negative 1.1%, Australia being at negative 1.2%, and Japan being just slightly overvalued at 0.5%. The only country that looks unattractive right now is India at a 9.6% overvaluation.

In general, we see that developed nations are overvalued and emerging nations are undervalued. The best way to use this chart is to look at the relative valuations between countries and not the absolute over- or undervaluation of any one country. When we do that, we see that the best values right now are Russia, Brazil, and China.

{kind=link}