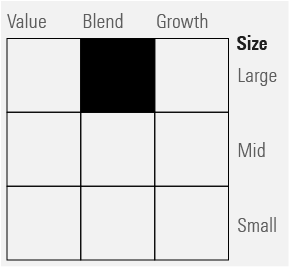

Investors have analyzed managers and portfolios with “style analysis”—particularly holdings-based style analysis, as presented by the Morningstar Style Box TM —for many years. The style box showcases funds on two distinct planes or dimensions of returns—size and value.

Since the style box’s launch in 1992, many other dimensions have been discovered or purported to have been discovered. We count over 160 published anomalies in equity markets, and we suspect this is an underestimate. But not only is the importance of these factors debatable, they may also not survive the test of time and market. We see this in R. David Mclean and Jeffrey Pontiff’s recent study of 97 factors, which found that a factor’s profit declines following its academic publication.

For investors who want to dig deeper

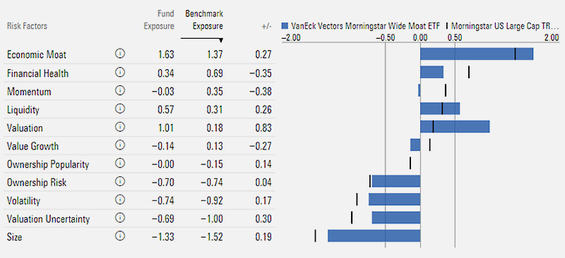

About two years ago, we introduced a 36-factor visualization based on the Morningstar Global Risk Model for those investors who want to dig deeper. BlackRock is apparently following suit with a “Factor Box,” which seems loosely comparable to our risk model visualization. Based on how BlackRock describes the Factor Box, one might think that size and value don’t matter in equity markets anymore. That couldn’t be further from the truth (or the data).

At Morningstar, we don’t see additional factors or sources of return as competition to traditional value/growth and size styles. Rather, we see them as complements that can be very useful secondary sources of information for investors to carefully consider. In the asset-pricing parlance, we see them as orthogonal dimensions of return. Despite the well-documented existence of other factors, we still believe that a style box should seek to give the foundation for a long-term portfolio allocation to investors. That should mean defaulting any style box to the planes of size and value.

Morningstar Style Box

Why do we talk about style? Here are two reasons.

- Nobel Prize-winning Eugene Fama and his co-author Kenneth French brought us the Fama-French model in the early 1990s. This model brought together work showing there is a size effect and a value effect, a tendency for investors to gain additional returns over what would be expected from the market risk alone for small-cap and value stocks. This is usually the second model taught in almost all finance classes today immediately following the capital asset pricing model, or CAPM. One of the first facts we learn is that the size and value factors command significant risk premiums over time that are comparable to the size of market premium, and these two factors significantly improve our ability to explain the cross-sectional stock returns over the CAPM. In Fama and French’s renowned study, the three factors explain more than 90% of the variations in returns for 21 out of the 25 portfolios formed based on size and book/market equity ratio.

- Perhaps more importantly, there’s a similar character to active managers. Some managers are small-cap specialists, while some specialize in large caps. And similarly, there’s a distinct difference in the management styles, turnover, and outlook for value against growth managers. Open any random fund prospectus around the world, and you’ll likely see strategies related to growth, value, or large/mid/small-cap. The commonality with which these strategies are employed underlines the rationale for defaulting to size and value in any style box. It’s probably not a coincidence that these active management strategies parallel the factor strategies which deliver excess returns.

So as a broad guide, the Morningstar Style Box simultaneously tells you something about the fund employing the style, as well as the two biggest explainers of long-term equity returns, size and value.

New factors keep coming

After the development of the Morningstar Style Box, more factors have been established in the academic literature. We capture several of them in our risk model, particularly momentum, volatility, and moat or stock quality. But these measures aren’t as important to understand an active manager’s behavior. We can talk sensibly about a value manager, or a small-cap specialist, or indeed a small-cap growth specialist. Very occasionally, you hear about particular managers as momentum specialists. But no managers call themselves “low volatility specialists” or “liquidity specialists,” let alone a “low-volatility, liquidity specialist.”

There’s an argument to bring in momentum as a dimension, and investors should certainly be live to momentum exposures in their portfolio. But the track record as an investment strategy sometimes experiences spectacular reversals. Historically, it has generated magnificent and consistent returns from 1940 through 2000 in U.S. equity markets, explaining substantial portfolio variation. But since then, performance has been much less consistent, with a massive reversal in the 2007-08 crash.

Can we use factors other than size and value?

We think paying attention to other well-established factors is useful for portfolio monitoring, but we are a little worried about how they will be used. There is something of a cautionary tale in sector rotation and more general tactical asset-allocation strategies. These were popularized in the 1990s. The idea is that macroeconomic cycles tend to make particular sectors boom and bust, and particular sectors are identified to be the ones to “get into” in particular conditions.

For instance, in the “full recession” stage of the economy, technology is meant to be oversold, and therefore a good idea to deliver excess returns. Tactical asset-allocation generalizes this idea, and managers rapidly shift between asset classes based on macro forecasts or trend-following.

Morningstar’s Jeff Ptak notes that tactical funds generally have failed to deliver better risk-adjusted returns, or downside protection, than do traditional balanced index portfolios.

And hence the worry—investors note that momentum strategies did very well in 2017, so load up on momentum. Or low volatility. Or whatever flavor of the month. Or more generally try to dynamically modify their portfolio to generate outperformance. Perhaps this strategy works sometimes, but it is certainly hard to execute well. More factors present investors with more flashing lights, something else to tactically shift over and thus generate trading costs and manager fee revenue, but not investor outperformance. Size and value, on the other hand, have proven to withstand the test of time and popularization.