- Risk tolerance, or a person’s ability to handle investment risk, doesn't change during an economic downturn.

- No two investors are the same. Use a risk tolerance quiz as a jumping-off point for individual conversations.

- Even experienced investors can grow nervous during market volatility. Look for ways to reframe anxiety as excitement.

Risk

Step-by-Step Guide: How to Calculate Risk Tolerance in an Economic Downturn

Key Takeaways

Read Time: 5.5 Minutes

Bear markets put pressure on financial advisors hoping to grow their practices.

Current clients will want to know if the market jeopardizes their retirement plans. Prospective clients will be (understandably) cautious about handling their money. If they get too nervous with the market’s inevitable swings, clients might sell off their equities and lock in their losses.

Don’t let your clients’ emotions interfere with their investing success. As an advisor, you need a way to understand your clients' actual risk tolerance, communicate your long-term plan, and instill confidence during times of stress.

Accurate risk profile assessments can help you maintain trust. Here’s a step-by-step guide to ensure your client relationships survive a market crash, including key talking points.

1. Reach out proactively to shore up relationships.

2. Give clients a proven risk tolerance quiz.

3. Talk through any discrepancies in their risk profile assessment.

4. Explain how their current portfolio lines up with their risk comfort.

5. Keep investors focused on what they can control.

Webinar

Risk & Rewards: Profiling to Meet Today's Needs

How do you know if your current risk profiling system is doing its job? Morningstar experts explain how to standardize your process to save time and money.

Step 1

Reach out proactively to shore up relationships.

Don’t wait until clients call you, anxious about the falling value of their portfolios. Regular check-ins show clients that you’re always thinking about their financial goals. That consistency builds trust in your expertise.

When you do connect, focus on listening instead of explaining. Some behavioral evidence shows that telling people not to panic often has the opposite effect. Take the opportunity to refocus on what matters most to your client.

Step 2

Give clients a proven risk tolerance quiz.

Let’s start by debunking the myth that risk tolerance, or a person’s psychological willingness to take risk in exchange for possible return, changes during an economic downturn.

This might seem counterintuitive. Of course, investors often feel pessimistic about the market when their portfolio loses value and optimistic when investments perform well.

Yet Morningstar data suggests that risk tolerance, when measured accurately, stays stable.

Over two decades, two million investors have taken our risk tolerance quiz. Advisors regularly retested their clients, showing how the same investors responded over time. Risk profiles changed slightly as investors aged, but even in the 2008-09 recession, risk tolerance largely remained a stable trait [PDF].

With the right tool, you can build reliable risk profiles for long-term portfolios. Look for risk profile assessments that explain and verify their methods with empirical testing.

Make a risk profile questionnaire part of your value proposition by showing clients how you think about risk. You can engage clients by helping them know themselves and their investments.

What to say to clients: Short-term volatility is always a part of investing. That’s why we focus on long-term performance. Based on a proven risk profile, we can build a plan for your personal goals and risk comfort, and make smart trade-offs.

Step 3

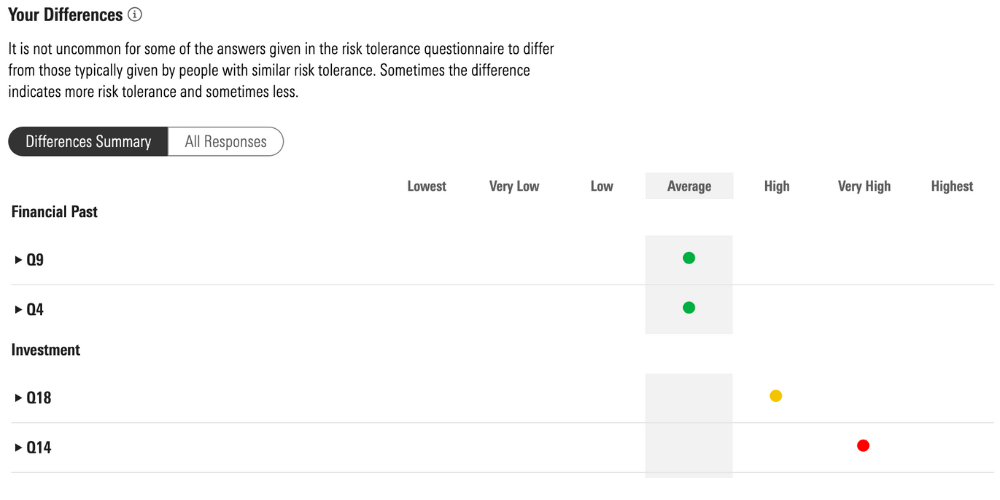

Talk through any discrepancies in their risk profile assessment.

No two investors are the same. Why would they have identical risk profiles?

If they wanted to, your clients could buy investment products on self-trading platforms. Investors turn to you for personal advice on their financial situation.

Use the risk tolerance quiz results as a jumping-off point for individual conversations.

Let’s use Gina as an example. Gina is in her early 30s, saving for her first house and retirement. Based on her risk profile assessment, she can handle an average amount of risk. Some of Gina’s responses, though, show a greater risk appetite:

- Gina said that it was much more important that the value of her investments retains its purchasing power than their current value.

- Gina said that the total value of her investments could fall by 50% before she would begin to feel uncomfortable.

You may use such differences to spur a deeper conversation, and ultimately calibrate a portfolio at the higher or lower end of a client’s Risk Comfort Range (more on this range below) based on a more nuanced understanding of their risk tolerance.

What to say to clients: Conservative investors with a low risk tolerance want to control their losses. Aggressive investors with a high-risk tolerance are willing to risk some money for the return potential.

Your risk tolerance falls within this range here. It’s normal for investors to differ from others in the same group. These differences help me fine-tune your plan for your financial goals.

Step 4

Explain how their current portfolio lines up with their risk tolerance.

If clients sound worried about the markets, it could be a good time to revisit their portfolio.

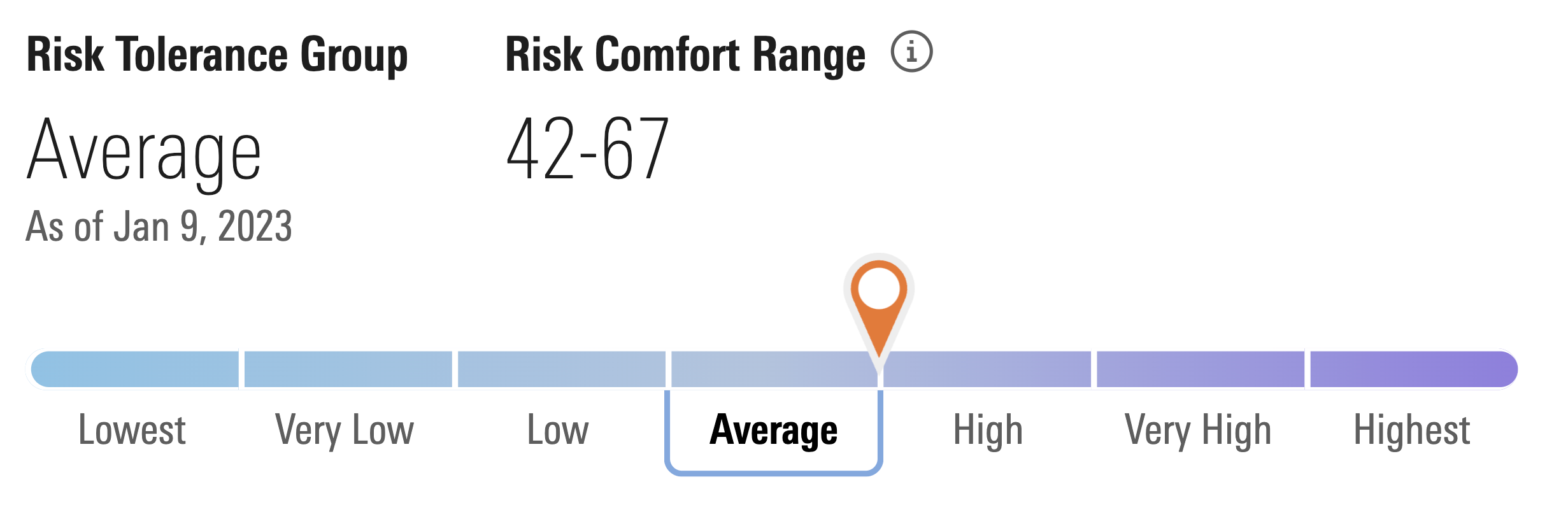

Your clients are more than a number. Every Morningstar risk tolerance test result includes a Risk Comfort Range, a range of portfolio risk that may straddle investment profiles and could support their goals. It gives you flexibility in constructing your advice.

This is how risk comfort would appear for our example client, Gina. Her risk tolerance falls on the upper end of the Average risk tolerance group and aligns with a Risk Comfort Range of 42–67. This range suggests Gina would be comfortable in a balanced portfolio with diversified equity exposure between mid-40% and mid-60%.

The comfort range gives you room for professional judgment. If your client has shown a need or propensity for more growth, you may look to position them at the higher end of the range. However, if they’re new to investing or don’t yet know much about financial markets, the lower end of the range may be more suitable.

The Risk Comfort Range gives you the flexibility to personalize while also reassuring your clients that their portfolios will stay within agreed-to levels of risk.

What to say to clients: On its own, a risk tolerance score isn’t good or bad. It’s a lens to calibrate portfolios to your comfort level. Your portfolio scores similarly to a well-diversified balanced portfolio. Based on your risk profile, you might experience some ups and downs, but should be generally comfortable with that. Let’s explore our options.

Step 5

Keep investors focused on what they can control.

Even experienced investors can grow anxious during market volatility. Broader economic forces can feel unpredictable and out of our control.

Look for ways to reframe anxiety as excitement. In down markets, you could uncover opportunities to be contrarian or opportunistic. Can you identify undervalued stocks or bonds? Have your clients explored tax-loss harvesting?

For some clients, it could be time to rebalance their portfolio to maintain their target asset allocation. Have bonds outperformed stocks? How does the portfolio balance U.S. and international markets?

These conversations can also broaden your advice from pure stock picks to broader financial coaching. Where can your client trim her spending? Can she build up her savings cushion?

What to say to clients: When we made this financial plan, we accounted for your personal goals. Based on your current asset allocation, you’re still on track, even with the market’s current gyrations.

Navigating an Economic Downturn

Done right, a risk tolerance quiz gives you a stable perspective on your client’s mindset.

If clients call you asking about the market correction, you have a way to explain what you’re already doing to help them reach their goals and how your plan aligns to their needs. The right approach to risk could also lead to much higher retention and a better connection with your clients.