After Earnings, Is Walmart Stock a Buy, a Sell, or Fairly Valued?

With the company’s great second quarter and stable business model, here’s what we think of Walmart stock.

Walmart WMT released its second-quarter earnings report on Aug. 17, before the market open. Here’s Morningstar’s take on Walmart’s earnings and stock.

Key Morningstar Metrics for Walmart

- Fair Value Estimate: $145.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

What We Thought of Walmart’s Q2 Earnings

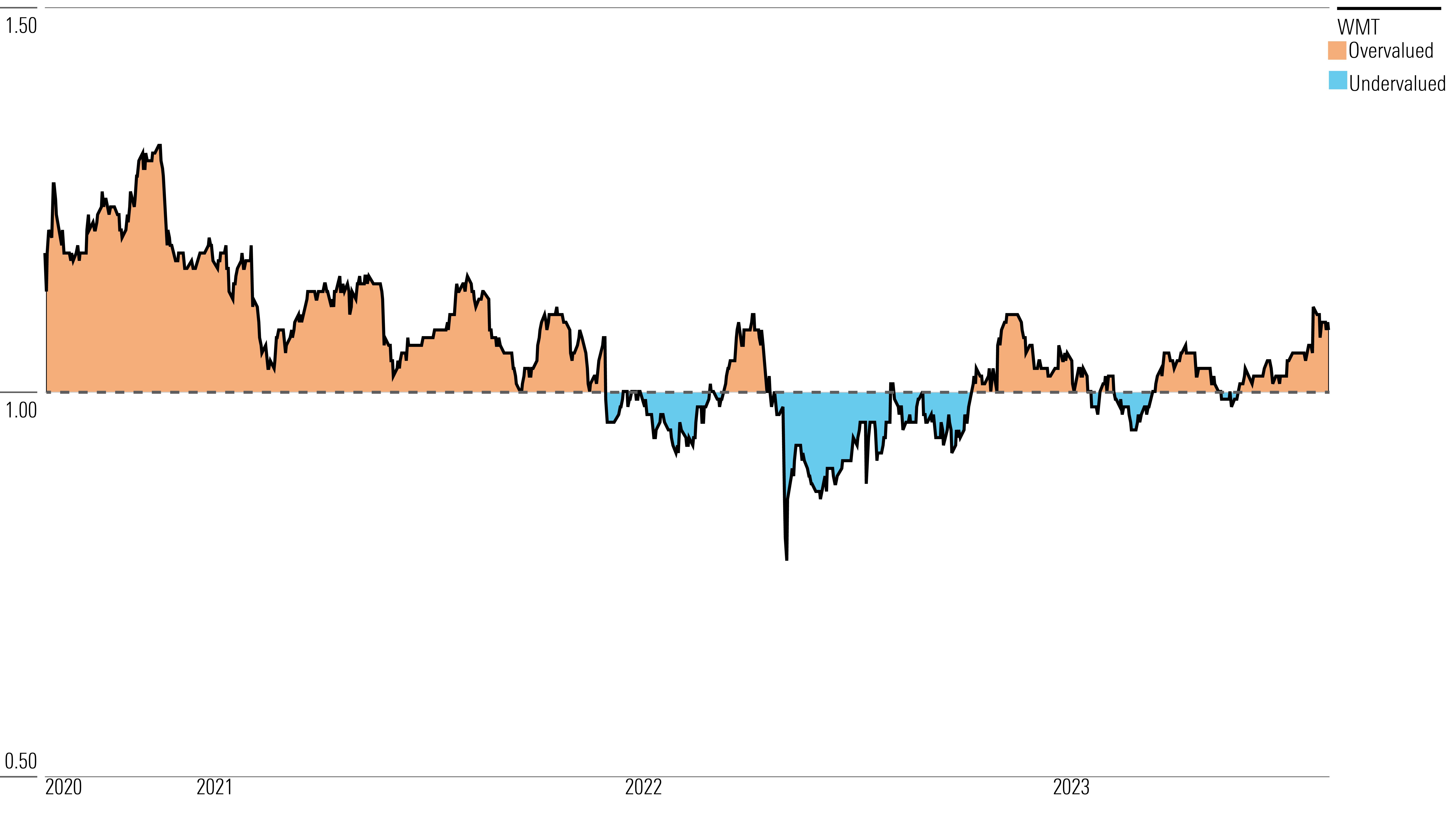

The market was expecting Walmart to deliver robust results, and it did, so the company’s stock price hasn’t moved much since its earnings release. Overall, Walmart looks fully valued from our perspective, as its stock trades at about an 8% premium to our $145 fair value estimate.

Solid second-quarter results: The company beat consensus estimates on the bottom line amid strong comparable sales growth (excluding fuel, comparable sales increased 6.4% in the United States and 5.5% at Sam’s Club) and modestly raised its full-year earnings per share guidance. During precarious economic environments, Walmart’s low-price proposition tends to resonate with consumers, so it was unsurprising to see it post strong top-line growth and a 2.9% increase in transaction volume during the quarter.

Good positioning for a tight economy: Walmart’s results reiterated the stability of its business model. With a value proposition predicated on offering the lowest price, the company is well-positioned to benefit from tighter economic conditions. For investors looking for steady financial results and low beta exposure during an uncertain time in the market, Walmart may fit that mold.

Digital initiatives: Management also commented briefly about its omnichannel and digital initiatives, such as Walmart’s third-party marketplace, fulfillment services, and advertising revenue. Management has invested significantly in these areas over the past several years in an attempt to create a digital ecosystem centered around the consumer, one similar to Amazon.com’s AMZN. While we expect Walmart’s investments in these areas to gradually scale over time, we don’t really view these initiatives as catalysts to drive pronounced top-line growth or margin expansion. Nonetheless, we think Walmart is successfully differentiating itself from smaller brick-and-mortar retailers, so perhaps the firm could gradually take some market share from those peers over time.

Stable valuation: Walmart is currently right on the edge of 2 and 3 stars. We expect the firm to deliver low-to-mid single-digit top-line growth, and forecast margins to modestly expand as its omnichannel initiatives and investments in supply chain automation scale over our 10-year explicit forecast.

Walmart Stock Price

Fair Value Estimate for Walmart

With its 2-star rating, we believe Walmart’s stock is overvalued compared with our long-term fair value estimate. In the wake of the company’s second-quarter results, we maintain our $145 fair value estimate, which implies a forward fiscal 2024 adjusted P/E of 22.7 times and enterprise value/adjusted EBITDA of 11.4 times.

We expect fiscal year 2024 to remain choppy as economic uncertainty and inflation pinch wallets. Nonetheless, we believe Walmart’s low-price value proposition will continue to appeal to consumers, driving share gains in its grocery category. As a result, we expect it to deliver modest growth in transaction volume and low-single-digit price growth due to inflation. However, we expect operating margins to remain pressured as discretionary spending abates and Walmart’s domestic sales mix leans toward the lower-margin grocery category.

Over a longer-term horizon, we expect Walmart U.S. (about 70% of total sales) to deliver low-single-digit top-line growth. We note that Walmart has reached its effective peak in physical store count, and we expect the retailer to instead deliver the bulk of its growth through increases in comparable store sales. Our estimate of 2.5%-3.0% comparable store sales growth is underpinned by modest growth in both volume and price and slightly exceeds the 2.0%-2.5% organic growth rate that Walmart U.S. posted over the past two decades. We believe Walmart is making the requisite investments today to continue attracting consumers to its stores and driving customer loyalty.

We expect e-commerce penetration to approach 18% of domestic sales by the end of our explicit forecast, but we don’t view the firm’s omnichannel investments as a catalyst for pronounced organic growth. Rather, we view the firm’s investments as an opportunity for Walmart to solidify its existing customer base and take some incremental share from smaller brick-and-mortar retailers that fail to adapt to consumer trends.

Read more about Walmart’s fair value estimate.

Walmart Price/Fair Value

Economic Moat Rating

We believe Walmart warrants a wide economic moat rating, underpinned by its ubiquitous brand and cost advantage.

Walmart is the largest retailer in the U.S., with over $420 billion in annual sales and a massive store footprint of over 4,700 domestic namesake locations. Despite the fragmented and competitive landscape inherent to retail, we surmise that Walmart has carved out an enviable position, as it benefits from its close proximity to the vast majority of U.S. consumers, driving repeat foot traffic.

Walmart supercenters (over 3,500 in the U.S.) provide an extensive product assortment at low prices, creating a convenient one-stop-shopping experience for consumers. As such, we view Walmart’s seemingly unwieldy physical footprint as a strategic asset due to its entrenchment in U.S. communities, allowing the firm to serve customers through multiple channels. Furthermore, the company leverages its unmatched scale by spreading its omnichannel and distribution investments over a wider sales and profit base, allowing the firm to adapt to the dynamic retail environment while maintaining robust profitability.

The retailer’s ability to drive recurring foot traffic has enabled Walmart to boast a dominant position in the domestic retail grocery channel with a 25% market share. For comparison, Walmart’s market share in U.S. grocery outpaces the combined 23% market share of the four next largest grocery channel retailers: Kroger KR, Costco COST, Target TGT, and Albertsons ACI. Grocery items made up 59% of Walmart’s U.S. sales in fiscal 2023, and the retailer’s wide assortment of nondiscretionary goods and perishable foods at low prices induces a degree of consistency in foot traffic and top-line resiliency even during times of economic stress.

Read more about Walmart’s moat rating.

Risk and Uncertainty

We assign Walmart a Medium Uncertainty Rating. The rise in e-commerce penetration serves as the most formidable threat to its traditional brick-and-mortar retail model. While the firm’s sales are underpinned by grocery items (59% of domestic sales), which tend to be more insulated from online penetration, we surmise Walmart faces tough online competition for sales of general merchandise such as electronics, apparel, and home decor, which is unlikely to abate anytime soon.

Given the higher margins that merchandise sales typically carry over that of grocery, margin pressure could ensue over time if grocery becomes a larger part of its mix. Furthermore, Amazon has entertained the idea of expanding its physical presence in grocery beyond its existing Whole Foods and Amazon Fresh footprint. While we view the threat to Walmart as low due to Amazon’s lack of physical storefronts, it is still worth monitoring competition for the corporate behemoth.

Walmart currently remains in investment mode as it continues to develop its omnichannel services, drive Walmart+ subscription adoption, and enhance its third-party marketplace. While we commend the company’s efforts, their underlying financial impact remains uncertain, and it will likely take significant scale to leverage the firm’s elevated fixed cost base. We note that Walmart has already made encouraging progress in areas such as online sales penetration and supply chain automation, but these developments are still nascent. The firm has also invested in dedicated e-commerce fulfillment centers, whose financial impact will be contingent upon consumers continuing to shop on Walmart.com, the adoption of Walmart Marketplace, and growth in the firm’s fulfillment service offerings to third-party sellers (which we surmise remain negligible relative to Amazon’s commensurate offerings).

Read more about Walmart’s risk and uncertainty.

WMT Bulls Say

- Margin pressure should abate as Walmart’s recent investments in omnichannel fulfillment and its third-party marketplace continue to scale.

- Walmart’s vast grocery offering insulates it from digital competition, given the perishability of the merchandise.

- Walmart’s recent investments in supply chain automation should drive margin expansion. The firm may also reinvest the cost savings to hold down prices and drive foot traffic to its stores—a benefit relative to many smaller retailers.

WMT Bears Say

- Walmart’s third-party marketplace and third-party fulfillment capacity pale relative to Amazon’s scale. We posit Amazon can underprice Walmart on commissions, listing fees, and fulfillment services related to its marketplace.

- Sam’s Club has woefully underperformed Costco in recent years, and the brand does not provide a compelling value proposition that would allow Sam’s to take share.

- Walmart’s sales mix of higher-margin general merchandise categories stands to decline due to strong digital penetration, prompting long-term margin degradation.

This article was compiled by Saaketh Tirumala.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/d10o6nnig0wrdw.cloudfront.net/05-20-2024/t_dc0763464c0a4191b876af1624b96f43_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IPKX4IWSDBD3VJC2Y34W6STFL4.jpg)