Your 2022 Medicare Fall Enrollment Checklist

How to effectively and efficiently re-evaluate your prescription drug or Medicare Advantage coverage.

Healthcare is one of the most significant expenses in retirement, and making smart choices about your Medicare enrollment can help you manage these costs.

One of the best ways to be smart about Medicare is to pay attention during the annual fall enrollment season, which began on Oct. 15 and runs through Dec. 7. This is the time of year when you can switch between Original Medicare and Advantage, or make changes to your current Part D or Advantage plan coverage to make sure you're getting the best deal financially--and the best match of healthcare providers and drug coverage.

Even if you like your current coverage, it can pay to take a careful look at your options during open enrollment. The design of your prescription drug plan coverage can change annually, and Advantage plans can make changes to their networks of healthcare providers at any time.

If you're enrolled only in original Medicare with a Medigap supplemental plan, there's no need to re-evaluate your Medigap coverage. But if you have original Medicare and a Part D drug plan, it definitely makes sense to review your drug plan annually to see what drugs will be covered and at what cost, and how they will be delivered.

And here's the bad news: Most people just won't do it.

A new report from the Kaiser Family Foundation, or KFF, shows that 71% of Medicare beneficiaries didn't compare their coverage to other options during fall enrollment in 2018, with the inattention about equal between people enrolled in traditional Medicare and Medicare Advantage. The rates of inattention were highest among people of color, beneficiaries age 85 or older, low-income people, and those with less education.

About half of all Medicare beneficiaries have never visited the Medicare website, called the Medicare toll free number (1-800-Medicare) for information, or read the Medicare & You handbook that is published annually by the government.

People either just don't know that they need to pay attention to this--or they find the process daunting. In 2021, the average Medicare beneficiary could choose among 33 Medicare Advantage plans and 30 Part D stand-alone prescription drug plans, according to KFF.

KFF's findings call into question one of the key propositions about Medicare: that privatization would foster improvements. Today's marketplace approach to Medicare began in the 1990s, encouraged by federal policy and legislation. In 1997, the Medicare+Choice program was created--a forerunner to Advantage that gave Medicare beneficiaries the opportunity to choose among a variety of plan options. The marketplace approach accelerated with the introduction of prescription drug coverage (Part D) in 2006 and the rapid growth of Advantage over the past decade.

Proponents of privatization argue that it gives Medicare enrollees plenty of choices; health insurance companies compete for your business, and that keeps prices down and encourages innovation. But that argument depends on the willingness of consumers to participate as educated consumers in Medicare marketplaces--a role most people do not play, as KFF reports.

And while premiums have stayed generally flat in Part D drug plans, that can be deceptive. Among the top plans, premiums can jump around quite a bit from year to year. And since insurance companies understand that buyers are most likely to focus on premiums than other plan features, they often try to keep premiums low while extracting more from enrollees through deductibles. The government places a cap on Part D deductibles--it is $445 in 2021, and roughly two thirds are charging the full amount.

And there is no out-of-pocket cap for enrollees on Part D costs.

Medicare Part D insurance covers most routine prescription drug costs. But seniors who need certain expensive brand-name or specialty drugs often face daunting, uncovered costs.

KFF studied expected annual out-of-pocket costs last year for 30 specialty drugs used to treat four conditions: cancer, hepatitis C, multiple sclerosis, and rheumatoid arthritis. It found that median out-of-pocket costs ranged from $2,622 for one drug used to treat hepatitis C to $16,551 for a leukemia drug.

Protecting yourself against this risk in the Part D insurance plan market is very difficult. Part D plans all charge similar amounts for specialty-tier drugs, ranging from 25% to 33% coinsurance, so picking one plan over the other will not help much with costs. And predicting a need for one of these drugs ahead of time is impossible.

More generally, it is important to consider whether a drug that you use is covered on a plan's list of approved drugs (the "formulary"), how much of the cost the plan will pick up, and whether you need to receive your prescription through a "preferred" pharmacy. This review needs to be done annually, since the terms frequently change.

"People often just look at the premium and make a decision around that," says Frederic Riccardi, president of the Medicare Rights Center. "But we advise against doing that. It's really important that people start to dig into the details of what the plan is going to offer."

Switching: Original and Advantage

It is possible to shift back and forth between Original Medicare and Advantage during the fall enrollment period. But practically speaking, if you select Advantage at the point of initial Medicare Part B enrollment, the decision may be irrevocable because of the rules governing availability of Medigap supplemental insurance.

If you are in Original Medicare, you're going to want supplemental coverage--and the best time to buy a Medigap policy is when you first sign up for Part B. That's because of Medicare's guaranteed issue rules, which forbid Medigap plans from rejecting you or charging a higher premium because of a pre-existing condition. This guaranteed issue opportunity is available to you during your six-month Medigap Open Enrollment Period, which starts on the first day of the month in which you're both 65 or older and enrolled in Medicare Part B.

During your guaranteed issue period, insurers must sell you a Medigap policy at the best available rate, regardless of your health status, and cannot deny you coverage. The premium will vary, depending on factors such as your age, gender, and where you live. A guaranteed issue right also prevents companies from imposing a waiting period for coverage of pre-existing conditions.

After your guaranteed issue period, Medigap plans in most states can reject applications or charge higher premiums due to pre-existing conditions, with the exception of four states that protect Medigap applicants beyond the guaranteed issue period. New York, Connecticut, Maine, and Massachusetts all have some form of guaranteed issue rules for later Medigap enrollment.

You also may have a guaranteed issue right under certain other circumstances later on, for example, if you had employer coverage that is discontinued, or if you're enrolled in a Medigap plan that is discontinued. You also have guaranteed issue rights if you joined an Advantage plan during your first year of Medicare but disenroll from it within 12 months.

If you are enrolled in Advantage and your guaranteed issue rights have expired, that decision becomes permanent, practically speaking.

COVID-19

Original Medicare Part B covers COVID-19 vaccines, regardless of whether you have Original Medicare or a Medicare Advantage Plan. You will owe no cost-sharing (deductibles, copayments, or coinsurance).

During the coronavirus public health emergency, all Medicare Advantage and Part D plans are required to provide up to a 90-day supply of drugs if you have a prescription for that amount (there are exceptions in place to prevent unsafe doses of opioids).

COVID-19 testing is covered under Medicare Part B. You pay nothing for the test if you have Original Medicare and see a participating provider, or if you have a Medicare Advantage Plan and see an in-network provider.

The expanded telehealth benefits created during the pandemic are still in place.

Nonmedical Supplemental Benefits

Medicare Advantage providers have been rolling out supplemental nonmedical services aimed at helping people stay in their homes, including grocery deliveries, caregiver support, and retrofitting homes to support older adults with chronic conditions. They also are permitted to expand transportation services.

A growing number of Advantage plans offer these benefits. Medicare indicated recently that the percentage of plans offering special supplemental benefits for chronically ill individuals will increase from 19% to 25% next year. A review commissioned by the Better Medicare Alliance--a Medicare Advantage research and advocacy organization for Advantage plans--found that 57% of Medicare Advantage plans now offer meal benefits, while 46% provide transportation to appointments.

It is possible to filter for some of these benefits in the plan finder, but they can be difficult to find. Moreover, the online tool won't provide guidance on whether you are in fact eligible to receive these benefits; that's a plan-by-plan decision based on your specific conditions and needs.

But Riccardi cautions against selecting an Advantage plan solely for these benefits: "Don't overlook the really important factors of the providers in the plan network and how much medical services will cost if you need them."

Dental, Vision and Hearing

Congress is considering a proposal to create a standard Medicare benefit for dental, vision, and hearing care as part of its deliberations over the social services legislation proposed by the Biden administration. The need for this care is high, especially dental. Two thirds of all people on Medicare don't have dental coverage, according to KFF. Among Medicare beneficiaries who used dental services, average out-of-pocket spending on dental care was $874 in 2018, and one fifth spent more than $1,000 out of pocket.

Currently, for traditional Medicare to pay for dental care, it must be deemed necessary as part of a covered procedure, for example, tooth extraction needed in preparation for radiation treatment. And the program does not cover hearing aids (which are notoriously expensive, often running into four figures) or exams, or most vision care.

Most Medicare Advantage plans offer some level of dental, vision, and hearing care. Some plans charge additional premiums for these services, but often they come with no additional premium paid by beneficiaries.

But the limits on what those plans cover vary widely. Among people in plans that offered both preventive and more extensive dental benefits, 43% faced annual dollar caps, typically around $1,000, KFF research shows. That means Advantage plans won't cover more-expensive services, such as implants.

If the Biden proposal is approved, increased coverage will not become immediately available, and some experts believe it will take several years to take effect.

How to Enroll

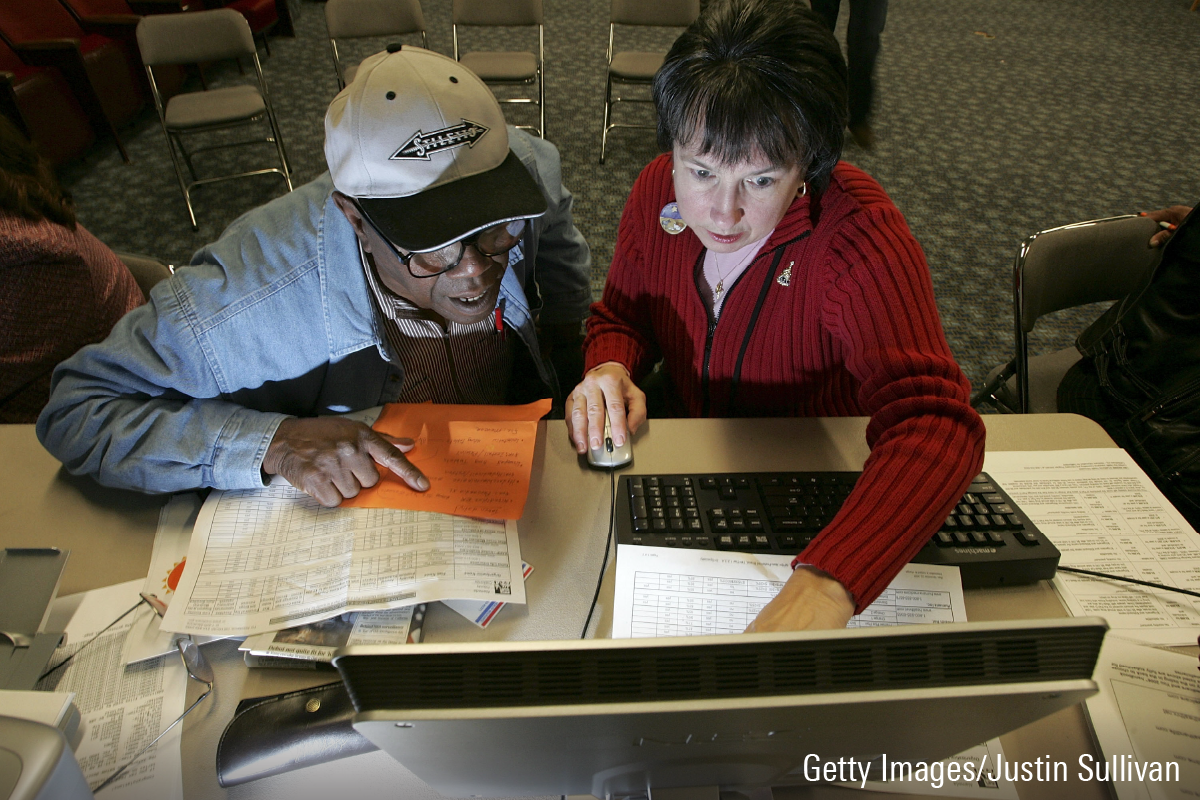

If you're a do-it-yourselfer, the federal government's Medicare Plan Finder is the place to go. But with so many choices--and subtle, complex differences in prescription drug plans--getting some knowledgeable help makes good sense.

The best idea is to use your State Health Insurance Assistance Program, or SHIP. These are free counseling services staffed by knowledgeable volunteers who can help you identify best-match coverage from the entire range of available plans where you live. Find yours here.

What about insurance brokers? Many brokers know the prescription drug, Advantage, and Medigap plan markets very well. But it's important to understand that brokers earn a living through commissions, so they have a built-in bias to sell their own product lines. And that means you will not be selecting plans based on thorough analysis of all the possible coverage choices available to you, and that also means you may not wind up with a best-fit plan.

A recent review of online broker plan selection tools by The Commonwealth Fund found that, on average, each tool included just 43% of available Medicare Advantage plans and 65% of Part D plans. By contrast, SHIPs will survey the entire range of plans available where you live.

"I think of the SHIPs as the gold standard of Medicare counseling," says Riccardi.

Once you've selected your plan, enroll directly through Medicare, either via the toll-free number or online. This is an important step, because it creates a confirmation record of the choices you make with Medicare that can be revisited if any subsequent errors are made in your enrollment.

Mark Miller is a journalist and author who writes about trends in retirement and aging. He is a columnist for Reuters and also contributes to The New York Times and WealthManagement.com. He publishes a weekly newsletter on news and trends in the field at RetirementRevised. The views expressed in this column do not necessarily reflect the views of Morningstar.

Mark Miller is a freelance writer. The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PJQ2TFVCOFACVODYK7FJ2Q3J2U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PVJSLSCNFRF7DGSEJSCWXZHDFQ.jpg)